Virginia HELOC Secrets Revealed: What Your Local Bank Is Hiding About Your Home’s Equity

You probably think your home is just a place where you sleep and store your stuff. If you are living in Virginia, your house is likely a silent goldmine. Over the last few years, property values in the Commonwealth: from the busy streets of Arlington to the quiet corners of Roanoke: have surged. This surge created a massive pool of wealth known as home equity.

Most people walk into their local bank branch, sit in a stiff chair, and ask for a Home Equity Line of Credit (HELOC). They walk out thinking they got a great deal. Often, they did not. Banks are businesses, and they have specific interests that do not always align with your wealth-building goals.

Explore the hidden mechanics of equity and learn how a strategic approach can turn your residence into a powerhouse of financial opportunity.

The Teaser Rate Trap: Why "Low" Isn't Always Better

Jump in and look at the first thing every Virginia bank puts in their window: the teaser rate. You might see an offer for 5.49% or 5.99%. It looks incredible compared to current market averages.

The Hidden Shelf Life

These rates typically last only six to twelve months. Once that introductory period expires, the rate resets to a much higher margin plus the prime rate. If you are not careful, your monthly payment could jump significantly overnight.

The Index and Margin Secret

Banks rarely volunteer the "margin" they add to the prime rate. A wholesale Virginia HELOC lender often provides access to lower margins than a retail bank. While a bank might charge Prime + 1.5%, a strategic broker might find you Prime + 0.5%. Over a ten-year draw period, that 1% difference represents thousands of dollars staying in your pocket instead of the bank's vault.

The Fee Schedule Banks Hope You Never Read

Compare the fine print of a standard bank HELOC with a wholesale product, and you will see a world of difference in the fee structure.

Annual and Inactivity Fees

Many institutions charge you just for having the line open. Even if you do not draw a single dollar, they might hit you with a $100 annual fee. Some even charge "inactivity fees" if you don't use the credit line enough. Accessing your own equity should not come with a subscription fee.

Early Closure Penalties

This is a big one. If you decide to sell your home or refinance your first mortgage within the first three years, many banks will charge you an "early closure fee" to recoup the closing costs they waived at the start. If you are an investor in Michigan or Indiana planning a quick flip or a BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), these fees can eat your profits.

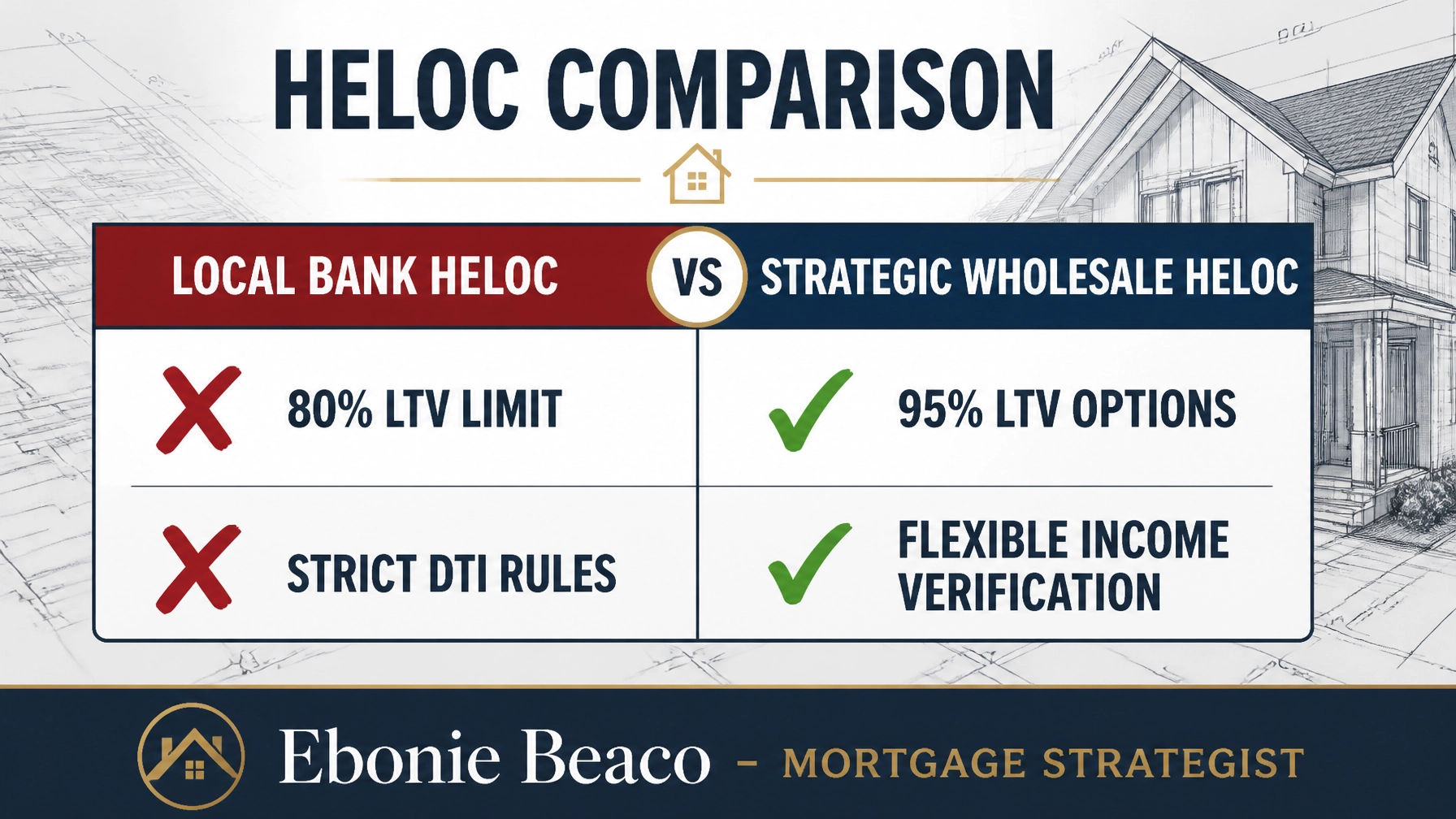

LTV Limits: The 80% Wall vs. The 95% Doorway

Most local banks in Virginia and Alabama have a hard cap on their Loan-to-Value (LTV) ratio. They typically stop at 80%. This means if your home is worth $500,000, they will only let your total debt (first mortgage + HELOC) reach $400,000.

Why Banks Limit You

Banks are risk-averse. They want a massive cushion of equity to protect their investment. While this is good for the bank, it limits your ability to leverage your assets.

The Strategic Alternative

A professional Michigan HELOC lender or a specialized strategist in Florida can often access programs that go up to 85%, 90%, or even 95% CLTV (Combined Loan-to-Value). This extra 10-15% can mean the difference between having the cash for a down payment on a new rental property or being stuck on the sidelines.

The Opportunity Fund: How Virginia Investors Play the Game

Real estate investors do not see a HELOC as debt; they see it as an "Opportunity Fund." Whether you are in Georgia, Illinois, or Kentucky, the strategy remains the same: use your home’s equity to acquire more income-producing assets.

Fast Cash for Fast Deals

In a competitive market like Richmond or Virginia Beach, cash is king. An investor with a standing HELOC can make a cash offer on a distressed property, close in two weeks, and then use a Fix and Flip Loan or a DSCR Investor Loan to stabilize the asset. Once the project is complete, they pay back the HELOC and do it again.

Renovation Power

Using a HELOC for substantial improvements can actually increase your home's value, creating even more equity. It is a self-fulfilling cycle of wealth creation.

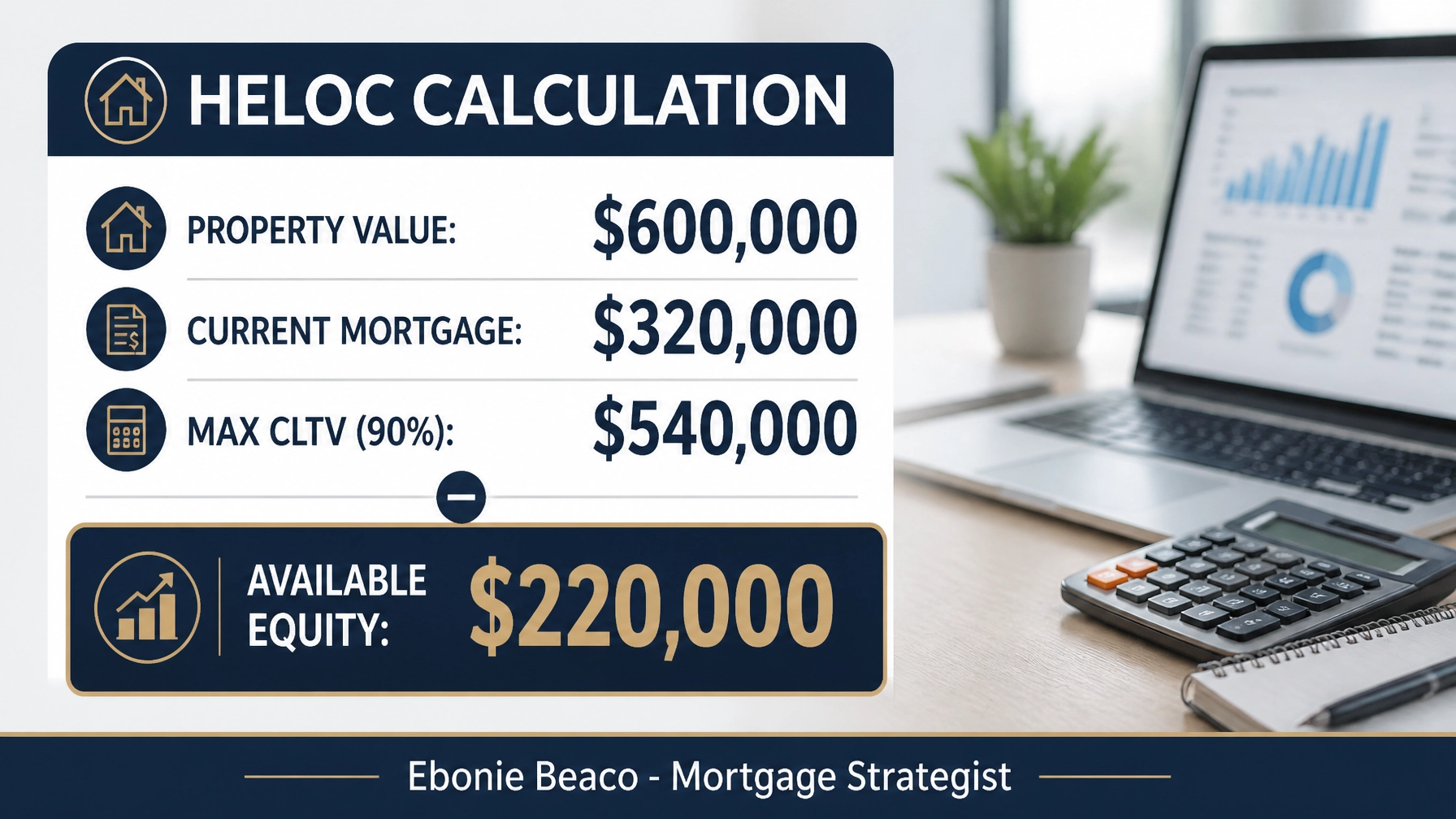

Crunching the Numbers: A Real-World Virginia Example

Let's look at the math. Suppose you own a home in a growing neighborhood in Alexandria or perhaps a suburb in Michigan.

The Profile:

- Estimated Home Value: $600,000

- Current Mortgage Balance: $320,000

- Homeowner Credit Score: 740+

The Bank Approach (80% CLTV):

- Total Allowable Debt: $480,000 ($600,000 x 0.80)

- Available HELOC: $160,000 ($480,000 - $320,000)

The Strategic Approach (90% CLTV):

- Total Allowable Debt: $540,000 ($600,000 x 0.90)

- Available HELOC: $220,000 ($540,000 - $320,000)

By working with a strategist who understands high-LTV products, you just unlocked an extra $60,000. That is enough to cover a down payment and closing costs on a $250,000 rental property in Missouri or Arkansas.

Beyond Virginia: A Multi-State Perspective on Equity

While this guide focuses on the secrets hidden by Virginia banks, these principles apply across the map.

- Michigan: As a Michigan HELOC lender, I see many homeowners in Grand Rapids and Detroit using equity to fund "up-north" vacation rentals.

- Florida and California: High property values in these states mean even a small percentage of equity translates into a massive line of credit.

- Illinois and Indiana: Investors in the Chicago metro area often use HELOCs to bridge the gap between a purchase and a long-term commercial loan.

Regardless of whether you are in Alabama, Arkansas, Georgia, Kentucky, or Missouri, the goal is the same: transparency and leverage.

How to Apply Without the Headache

The traditional loan process can feel like a part-time job. You shouldn't have to chase your banker for updates. A modern approach utilizes technology to streamline everything.

- Initial Strategy Session: We discuss your goals. Are you consolidating debt, renovating, or investing?

- Equity Analysis: We look at your current mortgage balance and property value to see your true potential.

- Multi-Lender Comparison: We check with a network of over 240 lenders to find the highest CLTV and the lowest margins.

- Fast Funding: Many of our wholesale partners can fund a HELOC in as little as two to three weeks.

Access the loan process guide to see exactly how we move from application to "clear to close" with maximum efficiency.

The Verdict: Your Equity, Your Choice

Don't let your local bank dictate the terms of your financial future. They will offer you what is best for their quarterly earnings report. You deserve what is best for your balance sheet.

Whether you need a Virginia HELOC lender to fund a kitchen remodel or a Michigan HELOC lender to help you buy your first duplex, the secret is out: you have more power than the bank wants you to know.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664