Virginia HELOC Secrets Revealed: What Your Local Bank Doesn’t Want You to Know About Your Equity

Homeowners across the Commonwealth of Virginia are sitting on a gold mine.

As property values in areas like Arlington, Richmond, and Virginia Beach have climbed, equity has reached record highs.

Most people assume their local bank is the best place to access that cash, but that assumption could cost you thousands.

Traditional institutions often play a specific game with your equity that favors their bottom line, not your financial growth.

Explore the reality of how a Virginia HELOC lender operates and how you can use your home to fund your next big move.

Is Your Bank Holding Your Equity Hostage?

Your local bank branch might feel like a safe harbor, but they often have the most restrictive lending guidelines.

Many banks prefer that you keep your equity locked away because it reduces their risk.

When you ask for a Home Equity Line of Credit (HELOC), they may offer terms that include high variable rates and stiff "hidden" requirements.

HELOC (Home Equity Line of Credit): A revolving credit line secured by your home equity that functions similarly to a credit card. Practical Application: You can borrow what you need, pay it back, and borrow again during the draw period without reapplying for a loan.

A dedicated Virginia HELOC lender often provides more flexibility than a big box bank.

They understand that your home is a tool for wealth building, not just a place to sleep.

The Phantom Fees That Drain Your Wallet

Local banks often hide the true cost of borrowing behind a curtain of "standard" fees.

You might see a low introductory rate, but the fine print reveals a different story.

Jump in and look for inactivity fees, which some lenders charge if you do not use your credit line.

They might also include annual maintenance fees ranging from $50 to $250 just for the privilege of having the account open.

Compare this to specialized mortgage strategists who focus on transparency.

Accessing your equity should not feel like death by a thousand paper cuts.

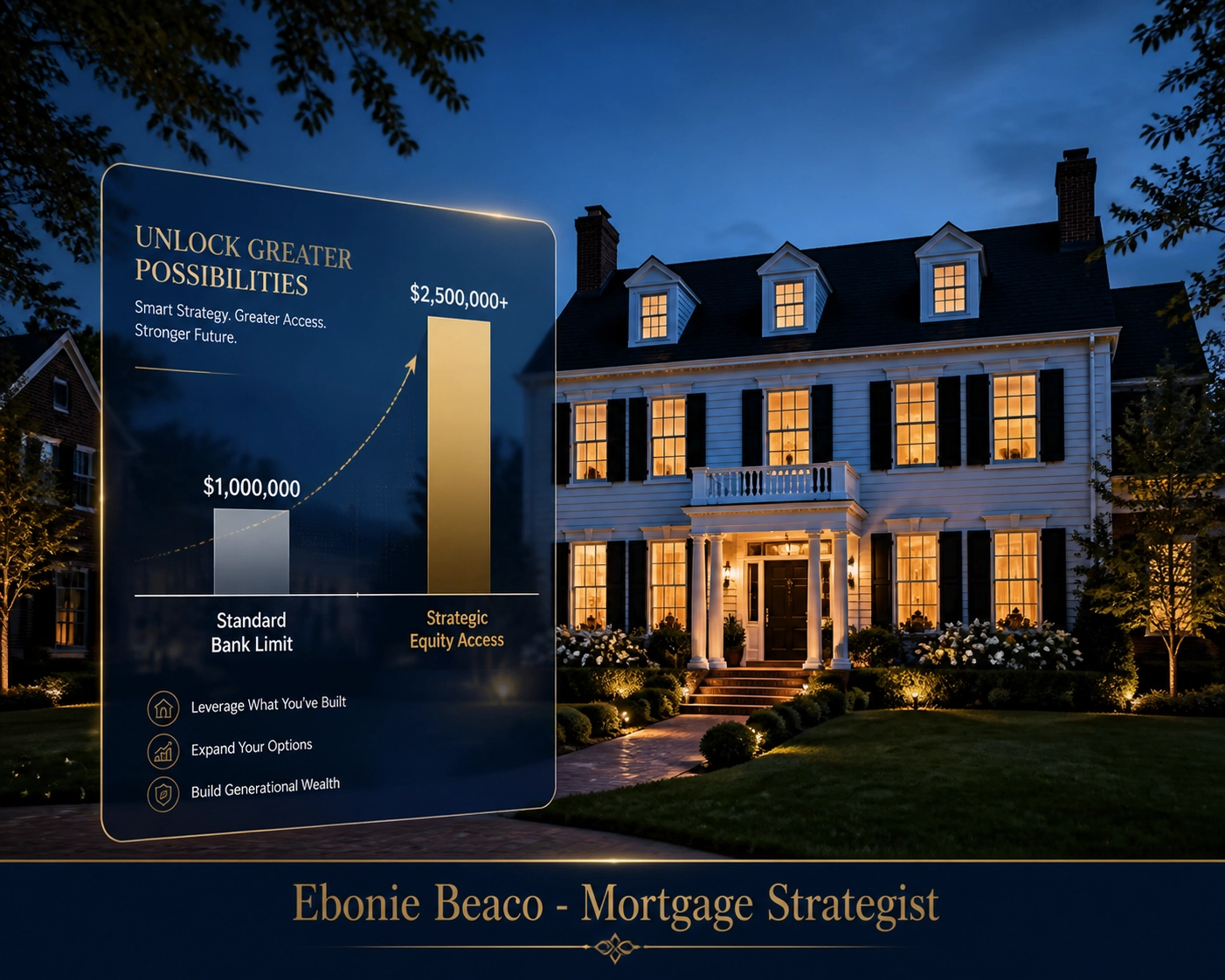

Why Your Loan-to-Value Ratio Is the Golden Ticket

Lenders use a specific formula to decide how much cash you can actually touch.

LTV (Loan-to-Value): The ratio of your current mortgage balance compared to the appraised value of your property. Practical Application: If your home is worth $500,000 and you owe $300,000, your LTV is 60%.

Most banks cap your total borrowing at 75% or 80% LTV.

However, some specialized programs allow you to go up to 85% or even 90% in certain markets.

If you are working with a Michigan HELOC lender or a Virginia HELOC lender, these extra percentage points can mean the difference between a $20,000 line and a $70,000 line.

Let’s Look at the Virginia Numbers

Imagine a homeowner in Alexandria with a property valued at $750,000.

They currently owe $425,000 on their primary mortgage.

A traditional bank might limit them to an 80% total LTV, giving them access to $175,000.

A more aggressive lender might allow an 85% LTV, opening up $212,500.

That $37,500 difference is enough to fund a major kitchen renovation or a down payment on an investment property.

The Draw Period vs. Repayment Period Trap

One secret your local bank might glaze over is the transition from the draw period to the repayment period.

Draw Period: The initial phase, typically 10 years, where you can borrow funds and often make interest-only payments. Practical Application: This keeps your monthly costs low while you are actively using the funds for projects.

Repayment Period: The phase following the draw period, usually 15 to 20 years, where you must pay back the principal and interest. Practical Application: Your monthly payment will jump significantly because you are now paying down the actual debt.

Many homeowners are shocked when their interest-only payment suddenly triples.

An expert strategist will help you plan for this transition or show you how to refinance the line before the repayment phase kicks in.

How Investors Use HELOCs to Scale Portfolios

If you are a landlord or a real estate investor, a HELOC is a tactical weapon.

Investors in Florida, Georgia, and California frequently use equity from their primary residence to fund "fix and flip" projects or "BRRRR" strategies.

BRRRR: Buy, Rehab, Rent, Refinance, Repeat. Practical Application: Use a HELOC for the purchase and rehab of a distressed property, then refinance it into a long term loan to pay back the HELOC.

By using a HELOC, you avoid the high interest rates of hard money loans.

You also keep your primary mortgage at its current low rate rather than doing a full cash-out refinance.

The Hidden Power of the "Standalone" HELOC

Most local banks want to be your only lender.

They might tell you that you need to move your primary mortgage to them to get a HELOC.

This is often a tactic to get you out of a low-interest rate environment and into a higher one.

A true Virginia HELOC lender can offer a "standalone" or "second lien" HELOC.

This allows you to leave your 3% or 4% primary mortgage exactly where it is while tapping into your equity separately.

Whether you are in Alabama, Arkansas, or Illinois, protecting your low primary rate is a priority.

Credit Scores and the HELOC Reality Check

Your credit health dictates your access to these funds.

DTI (Debt-to-Income): Your total monthly debt obligations divided by your gross monthly income. Practical Application: Lenders use this to ensure you have enough cash flow to handle a new credit line.

While a 620 score might get you in the door, the best rates are reserved for those above 720.

If your score is lower, you might find more success with Non-QM Mortgage Loans that look at your overall financial picture rather than just a number.

A Michigan HELOC lender often sees high demand in urban areas like Detroit or Grand Rapids where property values are shifting rapidly.

Having your credit in order before you apply is essential.

Using Equity for Short Term Rental Success

The Airbnb market in Virginia and Florida remains a hotspot for savvy investors.

Many people use a HELOC to fund the furniture and startup costs for a short term rental.

Since the income from these properties can be substantial, you can often pay back the borrowed funds quickly.

Compare this to using a high-interest credit card, and the savings are obvious.

If you are looking to expand into the Airbnb and Short-Term Rental Financing space, your home equity is your cheapest source of capital.

The Appraisal Hurdle

To get a HELOC, you usually need an appraisal.

Local banks sometimes use "drive-by" appraisals that might undervalue your home.

This limits your borrowing power before you even start.

A specialized lender often uses more comprehensive data to ensure you get every dollar of value your home deserves.

This is especially vital in fast-moving markets like Northern Virginia or Atlanta, Georgia.

Why Transparency Beats a "Local" Connection

The "bank down the street" doesn't always have your best interest in mind.

They have sales quotas for specific products that might not align with your wealth goals.

Working with a mortgage strategist gives you access to a broader range of options, including DSCR Investor Loans and bridge financing.

Transparency is the foundation of a good deal.

You deserve to know exactly what your equity can do for you without the corporate gatekeeping.

Access Your Future Today

Your home is more than just a roof; it is a financial engine waiting to be started.

Whether you are consolidating debt, renovating a historic home in Richmond, or buying a duplex in Michigan, your equity is the key.

Stop letting your local bank dictate the terms of your financial freedom.

Compare your options and see how a tailored strategy can change your trajectory.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664