Virginia HELOC Secrets Revealed: What Experts Don’t Want You to Know About Accessing Cash in 2026

Home equity in 2026 is sitting at a near-record $34.5 trillion across the United States. For homeowners in the Old Dominion and the Great Lakes State, this represents a massive opportunity to fund renovations, consolidate debt, or scale a real estate portfolio. However, the game has changed.

Lenders have tightened their belts, and the "no-questions-asked" equity lines of the past are long gone. If you want to tap into your home's value without losing your low-rate primary mortgage, you need a strategy that goes beyond just filling out an application.

Whether you are looking for a Virginia HELOC lender to fund a Richmond renovation or a Michigan HELOC lender to bridge the gap on a Detroit rental property, understanding the hidden mechanics of equity is your first step to winning.

The Invisible Gatekeepers of 2026

While national mortgage rates are projected to settle around 6% this year, HELOCs function differently. They are secondary liens, meaning the lender takes on more risk if you default. To offset this, many experts are noticing a shift in how these loans are approved.

Lenders are increasingly requiring larger initial draws. They don't just want you to have the line of credit; they want you to use it immediately. Furthermore, minimum usage requirements are becoming standard. If you open a line and let it sit at zero, you might find yourself hit with inactivity fees that weren't clearly disclosed in the fine print.

Explore our loan programs to see how these requirements vary across different states and products.

The Virginia Equity Explosion

If you own property in the Washington-Arlington-Alexandria corridor or the Hampton Roads area, you likely have significantly more "tappable" equity than the national average. In Northern Virginia alone, owners have seen equity gains nearly $50,000 above the national norm over the last five years.

This surge in value makes Virginia homeowners prime candidates for high-limit lines of credit. However, a common mistake is assuming your local bank will give you the best rate based on your property value alone.

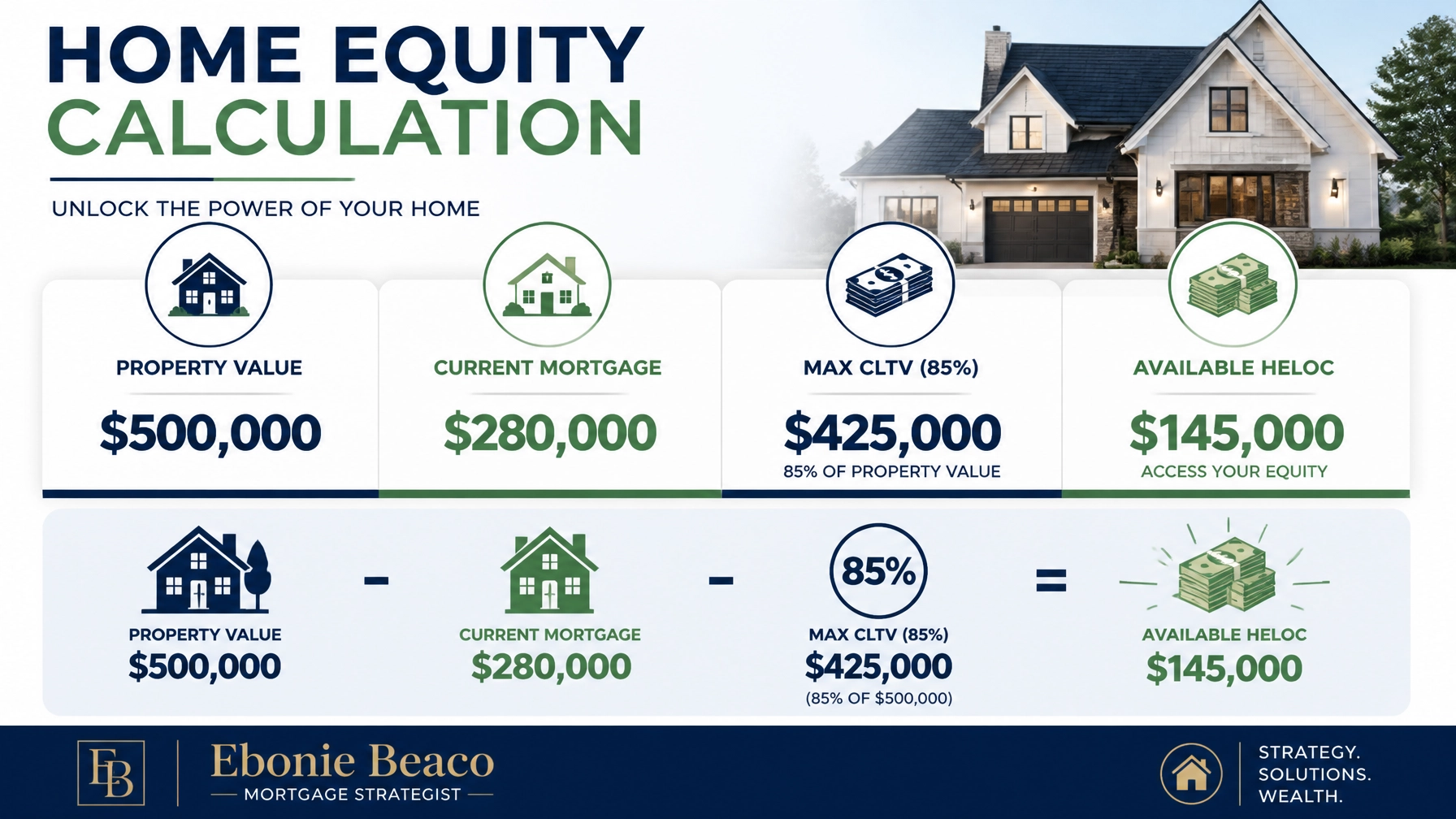

The Math: Cracking the Equity Access Code

To understand how much cash you can actually pull out, you have to look at the Combined Loan-to-Value (CLTV). Most lenders in 2026 cap this at 85%.

Let’s look at a real-world scenario. Imagine your home in Virginia Beach is worth $500,000. You still owe $280,000 on your primary mortgage, which you luckily locked in at 3.5% back in 2021.

- Property Value: $500,000

- Max CLTV (85%): $425,000

- Existing Mortgage: $280,000

- Available HELOC Limit: $145,000

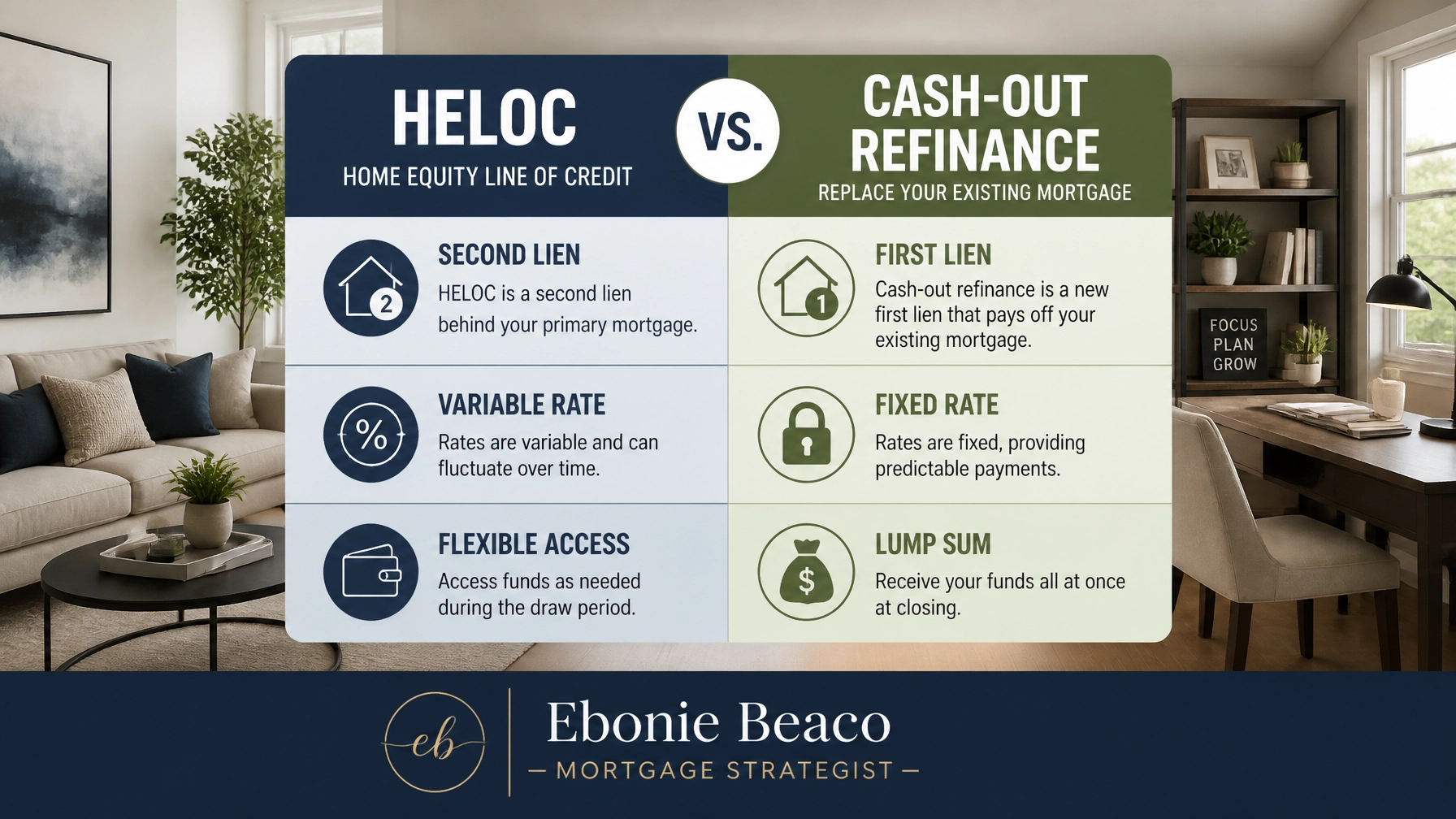

In this case, you can access $145,000 in flexible cash while keeping your 3.5% interest rate on the bulk of your debt. If you tried to do a traditional cash-out refinance, you would have to replace that 3.5% rate with a 2026 rate of roughly 6% to 7% on the entire balance. That move could cost you thousands in extra interest every year.

Why 2026 is Different for Michigan Homeowners

Michigan has a unique lending landscape. While Virginia often leans on large regional banks, Michigan is a stronghold for credit unions. As a Michigan HELOC lender search will show you, local institutions often offer more aggressive pricing on second liens to keep their members from going to national competitors.

For investors in Grand Rapids or Ann Arbor, the "secret" is leveraging these local rates to fund the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat). Using a HELOC as your "earnest money" or "gap funding" allows you to move faster than competitors who are waiting on traditional loan approvals.

Compare the different paths by reviewing our guide on mortgage basics to decide which structure fits your investment goals.

The Shadow Side of Variable Rates

Almost every HELOC in 2026 comes with a variable interest rate. This is the biggest risk for homeowners. When the Prime Rate moves, your payment moves.

One secret experts rarely emphasize is the Fixed-Rate Conversion Option. Many modern HELOCs allow you to "lock in" a portion of your balance at a fixed rate. For example, if you use $50,000 of your line to fix a roof, you can convert that specific $50,000 into a fixed-rate loan while keeping the rest of your line variable. This protects you from future payment shocks.

The Stealth Strategy for Landlords and Investors

If you are a landlord managing properties in Alabama, Florida, or Illinois, the HELOC is your secret weapon for portfolio expansion.

Investors often use a HELOC on their primary residence to pay for the down payment and renovation costs of a new rental property. Once the rental is renovated and occupied, they refinance that rental into a DSCR (Debt Service Coverage Ratio) loan. The proceeds from that refinance are used to pay the HELOC back down to zero.

This creates a revolving "funding machine" that allows you to buy multiple properties using the same pool of equity.

Access our mortgage calculators to run these numbers for your own portfolio.

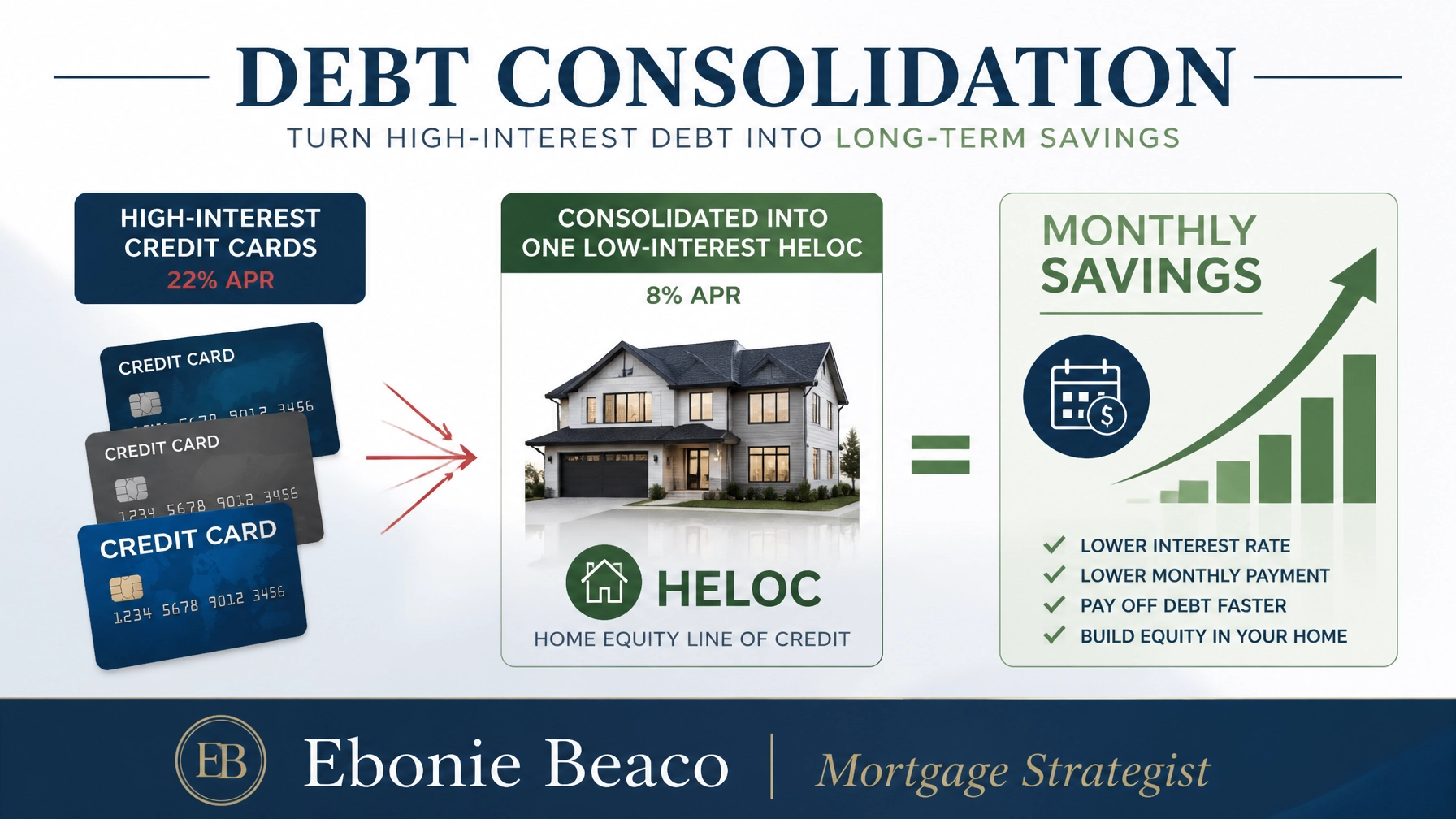

Debt Rescue: The Hidden Consolidation Play

High-interest debt is a wealth killer. In 2026, credit card APRs are still hovering around 22% for many borrowers. If you are carrying $40,000 in revolving debt across multiple cards, your interest payments alone are likely draining your bank account.

By using a HELOC at an 8% interest rate to wipe out those 22% cards, you immediately slash your interest expense.

The Debt Audit Example:

- Total Debt: $40,000

- Current Interest (22%): ~$733 per month

- New HELOC Interest (8%): ~$266 per month

- Monthly Savings: $467

This $467 in monthly savings can then be funneled directly back into the HELOC principal, effectively paying off your debt in record time. Just remember: a HELOC is secured by your home. Only use this strategy if you have the discipline to stop using those credit cards.

Why Lenders Want You to Wait

Lenders often profit more when you take out a full cash-out refinance because they get to re-originate a much larger loan and charge higher fees. They might tell you that a HELOC is "too complicated" or that the "rates are too high."

In reality, for many homeowners in Indiana, Kentucky, or Missouri, keeping a low-rate first mortgage and adding a HELOC is the smarter financial move. It preserves your existing wealth while giving you the liquidity you need for 2026 opportunities.

Your 2026 Equity Action Plan

If you are ready to stop guessing and start strategizing, here is how you should proceed:

- Run a Soft Pull: Check your credit without impacting your score. High-tier rates usually require a 740+ score. You can request this through our soft-pull credit request page.

- Audit Your CLTV: Use your latest property tax assessment or a reliable AVM to estimate your home's current value and subtract your mortgage balance.

- Define Your Exit: Are you using the cash for a one-time renovation or as an ongoing investment fund? This determines if you need a fixed-rate loan or a revolving line.

- Compare State Nuances: Funding speeds and appraisal requirements differ in California versus Arkansas. Understanding the local loan process ensures you aren't caught off guard by delays.

The equity in your home is not just a number on a statement: it is a tool. When used correctly, it can be the foundation of your financial independence.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664