Virginia HELOC Secrets Revealed: What Experts Don't Want You to Know

Homeowners across the Old Dominion are standing on a mountain of wealth that many don't even realize is accessible. Whether you own a classic colonial in Richmond, a high-rise condo in Northern Virginia, or a beach house in Virginia Beach, your home equity represents a potent financial instrument. But here is the catch: most traditional banks and big-box lenders want to keep you on a specific path that serves their interests, not yours.

As a Virginia HELOC lender, I see borrowers every day who think their only options are to sell their home or wait thirty years to pay off the mortgage. The truth is far more flexible. You can tap into your home’s value without losing your low-interest first mortgage. If you are looking for a Michigan HELOC lender or someone to guide you through the equity landscape in states like Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Missouri, and Virginia, you have come to the right place.

Defining the Mechanics of Equity

HELOC (Home Equity Line of Credit): A revolving credit facility secured by your primary or secondary residence that allows you to withdraw funds as needed up to a predetermined limit.

Practical Application: Use it like a credit card for your house: draw funds for a renovation, pay them back, and then use the line again for a down payment on a rental property.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property (first mortgage plus the HELOC limit) compared to the appraised value of the home.

Practical Application: Lenders use this to set your maximum borrowing limit; staying under 85% often yields the best rates.

Draw Period: The initial phase of a HELOC, typically 10 years, during which you can access funds and often make interest-only payments.

Practical Application: This is your window of maximum flexibility for funding short-term investment needs.

The Equity Extraction Hack: Using Your Home as a War Chest

Most financial advisors tell you to "save up" for your next investment. In the world of high-velocity real estate, waiting to save cash is a recipe for missed opportunities. The "secret" that savvy investors in Virginia and Michigan use is treating their home like a private bank.

Instead of letting $200,000 in equity sit idle, these investors open a HELOC to create a "war chest." When an off-market deal surfaces or a distressed property hits the auction block, they don't wait for a bank to approve a new loan. They write a check from their HELOC, buy the property cash, and then refinance it later into a long-term DSCR investor loan.

Explore our variety of loan programs to see how different financing vehicles can move your portfolio forward.

The Appraisal Gap Loophole: Why You Might Skip the Walkthrough

One of the biggest hurdles to accessing your equity is the dreaded appraisal. Traditional banks often require a full interior inspection, which can take weeks and cost hundreds of dollars. However, there is a "wholesale secret" many experts don't mention: the Automated Valuation Model (AVM).

Many modern Virginia HELOC lenders and Michigan HELOC lenders now utilize AVMs or "drive-by" appraisals. If your home is in a neighborhood with plenty of recent sales data, we may be able to determine your value in seconds without a stranger ever walking through your front door. This speeds up the process from weeks to days, allowing you to access capital while the market is still hot.

The Math of Your Available Wealth

To understand how much you can actually pull out, you have to look at the numbers. Let’s look at a typical scenario for a homeowner in a growing market like Arlington, VA or Grand Rapids, MI.

Scenario Analysis:

- Appraised Property Value: $500,000

- Lender Max CLTV (85%): $425,000

- Current First Mortgage Balance: $280,000

- Potential HELOC Limit: $145,000

In this example, the homeowner has unlocked $145,000 in liquid capital. They keep their existing 3% or 4% interest rate on their primary mortgage and only pay interest on the $145,000 if they actually spend it. This is a far more efficient strategy than a cash-out refinance, which would require refinancing the entire $425,000 at today's higher market rates.

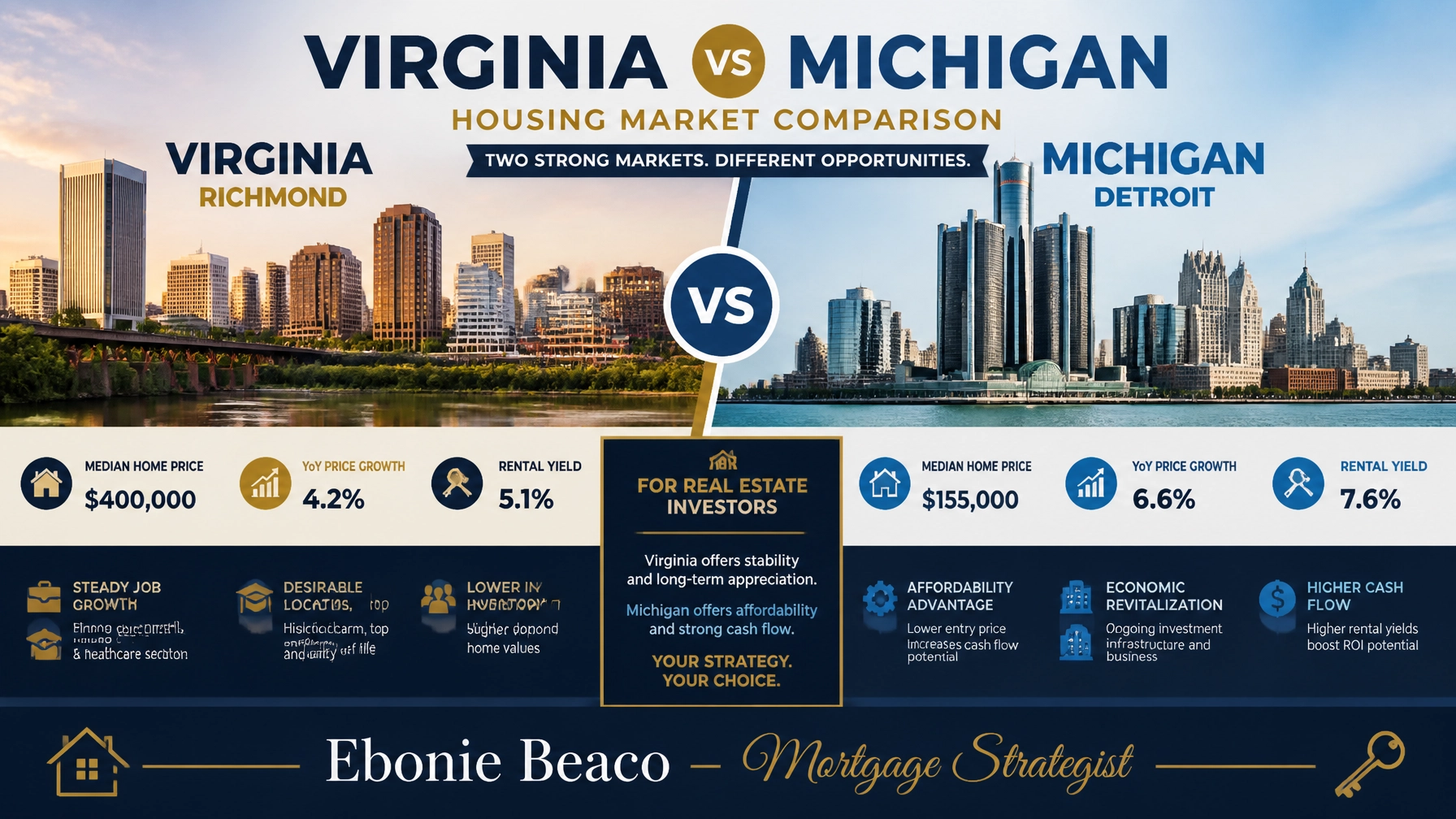

Regional Nuances: Virginia vs. Michigan Lending

While the fundamental rules of mortgage finance are national, the local "vibe" of the market changes how you should use your equity.

In Virginia, particularly Northern Virginia and the Richmond area, property values tend to be higher and appreciation is often driven by government and tech sector stability. Homeowners here often have massive equity "bloat": values that have skyrocketed over the last five years. A HELOC here is often used for large-scale renovations or as a bridge to buy a secondary vacation home in the Outer Banks.

In Michigan, the strategy often shifts toward cash flow. Investors in Detroit or Lansing might use a HELOC on their primary residence to purchase multiple low-cost rental units. Because Michigan's entry price point for real estate can be lower than Northern Virginia's, a single $145,000 HELOC could potentially fund down payments for three or four different investment properties.

Compare your options with our mortgage calculators to see how these numbers play out for your specific zip code.

The 90% CLTV Mystery: How to Push the Limits

Most big banks stop lending at 80% LTV. They want a massive safety net. But what if you need more?

There are specialized programs available through wholesale channels that allow for a 90% CLTV. This means you can keep even less of your equity "trapped" in the walls of your home. This is especially useful for high-net-worth individuals or self-employed borrowers who have significant assets but prefer to keep their cash working in their business rather than sitting in home equity. If you have been told "no" by a local credit union because you have "too much debt" or "not enough equity," it is likely they just don't have access to these aggressive wholesale tiers.

The Repayment Ticking Time Bomb: A Warning

I promised transparency, so we have to discuss the risk. The biggest danger of a HELOC is the transition from the draw period to the repayment period.

During the first 10 years, many HELOCs allow for interest-only payments. This feels great for your monthly cash flow. However, once that 10-year clock hits zero, you must start paying back the principal. Your monthly obligation could double or even triple overnight.

Expert Tip: Never open a HELOC without a clear "exit strategy." If you are using the funds to renovate, your exit might be selling the home. If you are using it for a down payment, your exit should be refinancing the new investment property to pay back the line.

The Ultimate Investor Strategy: HELOC + BRRRR

For those looking to build generational wealth, the HELOC is the ultimate "starter motor." Many of the most successful investors I work with in Illinois, Florida, and Georgia use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) fueled entirely by their home equity.

The Workflow:

- Buy: Use your HELOC funds to buy a distressed property in cash.

- Rehab: Use the remaining HELOC funds to pay for contractors and materials.

- Rent: Place a tenant to generate cash flow.

- Refinance: Use a DSCR loan to refinance the property at its new, higher value.

- Repeat: Use the refinance proceeds to pay back your HELOC, making the line available for your next deal.

Jump in and see how we support investors across all our service areas. Whether you are a first-time homebuyer or a seasoned landlord with a 50-unit portfolio, the strategy remains the same: leverage your existing assets to acquire new ones.

Accessing your home equity is one of the most significant financial moves you will ever make. Don't leave it to a generalist at a retail bank who doesn't understand the nuances of investment strategy. You deserve a mortgage strategist who can align your financing with your long-term goals.

Ready to see how much equity you can unlock?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664