Using a HELOC for Your Next Down Payment

Equity is often described as a sleeping giant.

Many homeowners in markets like Chicago, Florida, and California sit on a significant amount of wealth that stays locked away in their primary residence.

A Home Equity Line of Credit (HELOC) is one of the most effective tools for waking that giant up and putting it to work for your next real estate transaction.

Whether you are looking to buy a vacation home in Virginia, a rental property in Alabama, or your next primary residence in Michigan, a HELOC provides a flexible way to fund your down payment.

Jump in to explore how this strategy works and how you can leverage your current home to expand your real estate portfolio.

What exactly is a HELOC?

A HELOC is a revolving line of credit that is secured by the equity in your home.

Home Equity: The difference between the current market value of your property and the remaining balance on your mortgage. Practical Application: If your home is worth $500,000 and you owe $300,000, you have $200,000 in equity.

Unlike a standard home equity loan, which provides a lump sum of cash, a HELOC functions much like a credit card.

You are approved for a specific credit limit based on your home’s value and your creditworthiness.

You can draw funds as needed, pay them back, and draw them again throughout the designated "draw period," which typically lasts ten years.

Explore more about fundamental terms on our mortgage basics page.

Using a HELOC for a Down Payment

Using a HELOC for a down payment is a strategy used by savvy homeowners and real estate investors to avoid liquidating their personal savings or selling their current home before they are ready.

Strategy 1: Purchasing an Investment Property

Real estate investors in states like Indiana, Kentucky, and Missouri often use HELOCs to fund the down payment on DSCR rental property loans.

By using the equity in a primary residence to cover the 20% or 25% down payment required for an investment property, the investor can acquire a new asset without touching their cash reserves.

This is particularly useful for BRRRR investors (Buy, Rehab, Rent, Refinance, Repeat) who need quick access to capital to secure a deal.

Strategy 2: Bridging the Gap to a New Primary Residence

If you are looking to move but haven't sold your current house yet, a HELOC can act as a bridge loan.

You can draw the down payment for your new home from your current home’s equity.

Once you sell your original home, you can use the proceeds to pay off the HELOC.

This allows you to make non-contingent offers, which is a significant advantage in competitive markets like Georgia and California.

You can review our home purchase guide for more insights on structuring these deals.

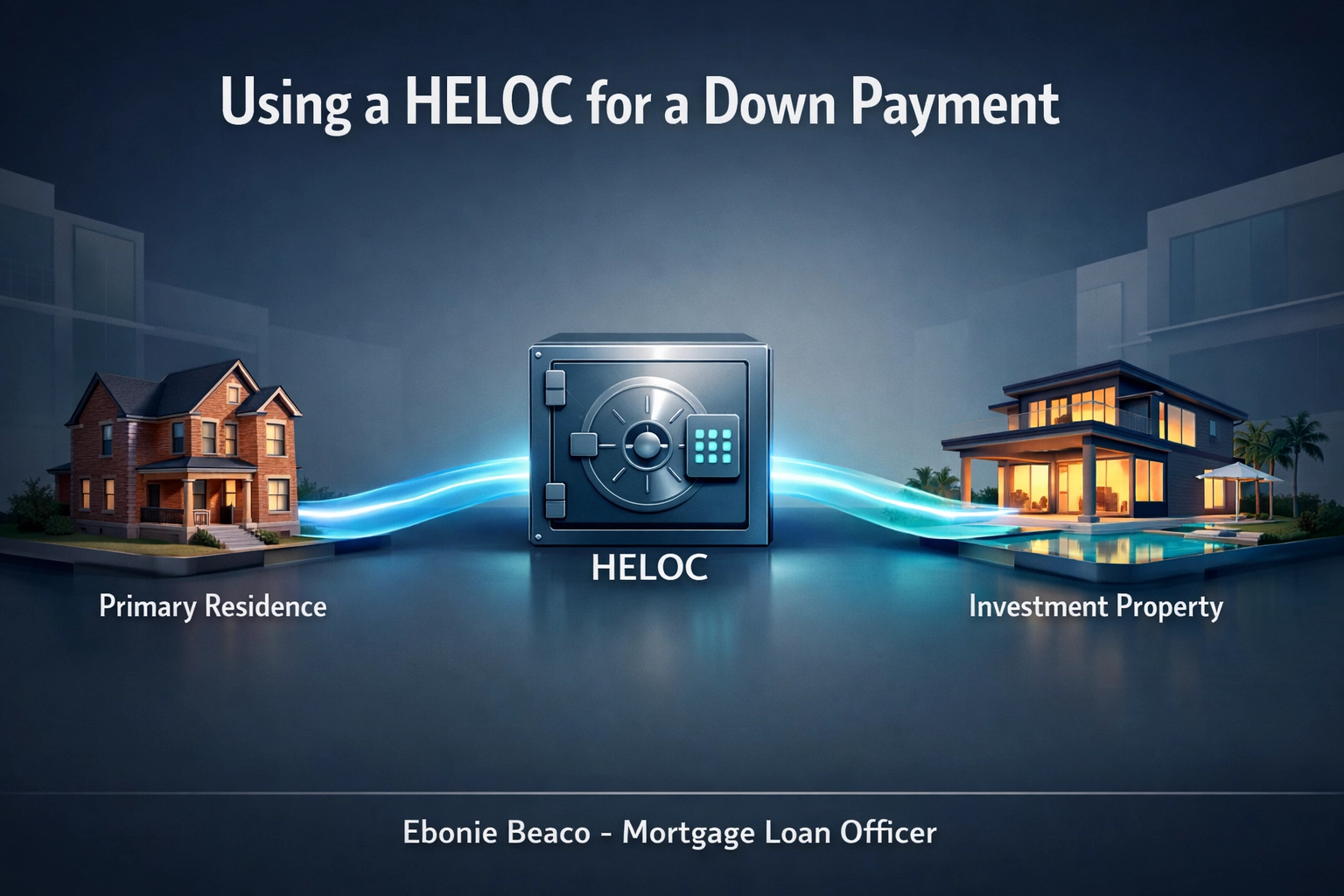

Visual: A flowchart showing equity moving from a primary home into a HELOC account and then being applied as a down payment for a second property titled "Using a HELOC for a Down Payment" with "Ebonie Beaco - Mortgage Loan Officer" at the bottom.

Visual: A flowchart showing equity moving from a primary home into a HELOC account and then being applied as a down payment for a second property titled "Using a HELOC for a Down Payment" with "Ebonie Beaco - Mortgage Loan Officer" at the bottom.

The Financial Advantages

There are several strategic reasons to consider a HELOC over other types of financing.

- Avoid PMI: By using a HELOC to reach a 20% down payment on your next home, you eliminate the need for Private Mortgage Insurance (PMI), which reduces your monthly overhead.

- Flexibility: You only pay interest on the amount you actually draw, not the total credit limit.

- Lower Monthly Payments: A larger down payment funded by a HELOC results in a smaller primary mortgage on the new property.

- Speed: Once the HELOC is in place, you can access the funds instantly via transfer or check, allowing you to move fast on investment opportunities.

- Tax Considerations: In some scenarios, interest on HELOC funds used for home improvements or specific investments may be tax-deductible; always consult with a tax professional.

Compare your options and see how different loan structures affect your bottom line using our mortgage calculators.

Analyzing the Numbers: A Real-World Calculation

To understand how much you can actually access, you need to look at your Loan-to-Value (LTV) ratio.

Most lenders will allow you to borrow up to 80% or 85% of your home’s total value, including your existing first mortgage.

LTV (Loan-to-Value): A ratio that compares the amount of your mortgage or credit line to the appraised value of the property. Practical Application: Lenders use this to determine the risk level of the loan and the maximum amount you can borrow.

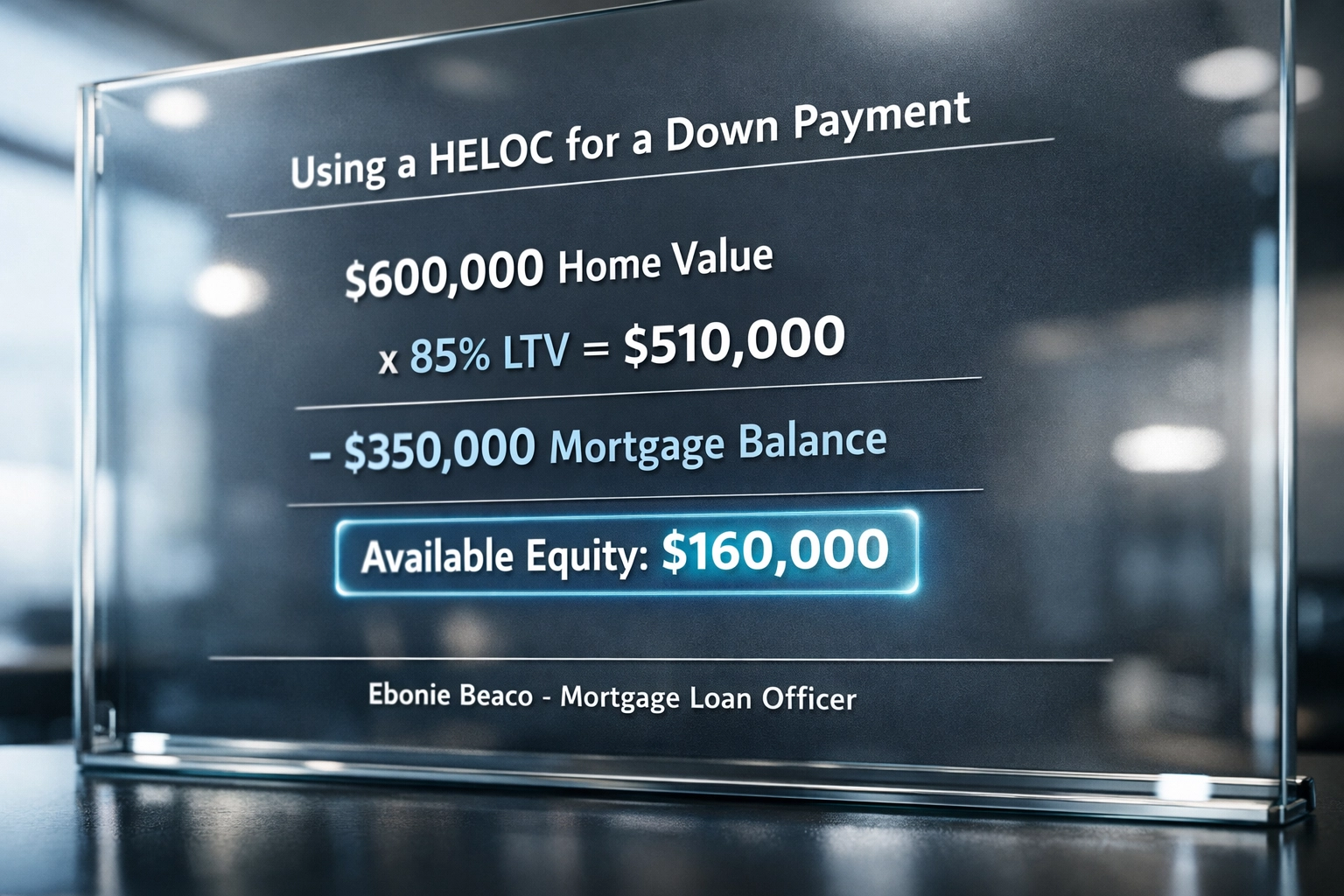

The Calculation Breakdown

Imagine you own a home in Chicago or Virginia with the following profile:

- Current Home Value: $600,000

- Max Combined LTV (85%): $510,000

- Current Mortgage Balance: $350,000

- Available HELOC Capacity: $160,000

In this scenario, you could potentially access $160,000 to use as a down payment for a second home or a rental property.

Visual: A financial breakdown chart titled "Using a HELOC for a Down Payment" displaying the calculation: $600k Value x 85% LTV = $510k, minus $350k Balance = $160k Available Equity. "Ebonie Beaco - Mortgage Loan Officer" at the bottom.

Visual: A financial breakdown chart titled "Using a HELOC for a Down Payment" displaying the calculation: $600k Value x 85% LTV = $510k, minus $350k Balance = $160k Available Equity. "Ebonie Beaco - Mortgage Loan Officer" at the bottom.

Qualification Requirements

Accessing this equity requires meeting specific criteria.

While every lender has different guidelines, the following are standard benchmarks for securing a HELOC:

- Equity: You generally need at least 15% to 20% equity remaining in the home after the HELOC is added.

- Credit Score: A score of 680 is often the minimum, though 720+ often secures the best interest rates.

- Debt-to-Income (DTI) Ratio: Lenders typically look for a DTI of 45% or lower.

- Income Verification: Consistent income is required to ensure you can handle the new monthly payment.

For self-employed borrowers in Florida or Michigan, we often explore bank statement loans if traditional tax returns don't tell the whole story.

Learn more about these specific requirements in our FAQ section.

Geographic Considerations

Real estate is local, and how you use a HELOC may vary depending on where you are buying.

- Florida and California: These markets often have higher property values. A HELOC can be the key to affording a down payment in a high-cost area where 20% can be a substantial six-figure sum.

- Midwest Markets (Illinois, Indiana, Michigan): These areas are prime for Airbnb and short-term rental financing. Using equity from a primary home to fund the down payment on a lakefront rental or a city condo is a common path to building a portfolio.

- Arkansas and Alabama: With lower entry prices, a HELOC from a more expensive market can often cover the entire purchase price or a massive down payment for multiple rental properties.

Potential Risks and Transparency

At Home Loans Network, we believe in full transparency.

Using a HELOC for a down payment is a powerful strategy, but it is not without risk.

Secured Debt: A HELOC is secured by your primary residence. If you fail to make payments, your home could be at risk of foreclosure. Practical Application: Ensure your cash flow from the new property or your personal income can comfortably cover the HELOC interest and the new mortgage payment.

You will also be managing multiple monthly payments: your original mortgage, the HELOC payment, and the new property's mortgage.

Understanding your cash flow is vital before moving forward.

Check out our loan process page to see how we help you evaluate these risks.

Taking the Next Step

Using a HELOC for your next down payment is a sophisticated move that requires careful planning and a clear understanding of your financial profile.

It is one of the most popular ways for homeowners to transition into becoming real estate investors or for current investors to scale their operations in states like Virginia, Georgia, and beyond.

If you have equity in your home, you have options.

Access the tools and guidance you need to make an informed decision about your home's value.

Whether you are looking for a cash-out refinance, a HELOC, or DSCR investor loans, we are here to provide a clear path forward.

Reach out to Ebonie Beaco to leverage your home equity or for mentoring at www.homeloansnetwork.com.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664