Understanding Mortgage Rate Volatility: Today’s Market Update for Florida and Illinois Borrowers

Navigating the modern mortgage landscape requires a clear understanding of the forces driving interest rate fluctuations. As of late May 2026, borrowers in Florida, Illinois, and across the nation are witnessing a period of notable volatility. This shift is largely influenced by persistent inflation data and the Federal Reserve's cautious stance on monetary policy. Staying informed allows homeowners and investors to align their financing strategies with the current economic reality.

Explore the latest trends to see how they impact your ability to purchase, refinance, or expand your real estate portfolio. Whether you are looking at a single-family home in the Chicago suburbs or a high-end condo in Miami, the cost of borrowing remains the most significant variable in your transaction. By analyzing today's data, you can move forward with confidence and clarity.

Jump into this comprehensive update to discover how the current rate environment affects borrowers in Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia. We will break down the numbers, define technical terms, and provide practical strategies for navigating these changes.

The Current State of Mortgage Interest Rates

Average 30-year fixed mortgage rates are currently hovering in the mid-6% range, specifically between 6.5% and 6.7%. This represents a slight uptick from earlier in the month, driven primarily by an inflation rate that remains higher than the Federal Reserve's 2% target. For those considering shorter-term financing, 15-year fixed purchase rates are currently sitting between 5.8% and 6.1%.

Jumbo loans and adjustable-rate mortgages (ARMs) are also seeing similar patterns. The 30-year jumbo rate is currently averaging between 6.6% and 6.8%, reflecting the increased risk and capital requirements for larger loan amounts. Meanwhile, the 5/1 ARM remains a popular choice for those planning a shorter holding period, with rates currently near 5.8%.

Access the latest national data from sources like The Mortgage Reports to see real-time updates. This data confirms that while rates have stabilized compared to the highs of previous years, the path toward lower interest levels remains slow and uncertain.

Drivers of Volatility: Why Rates Remain Elevated

The Federal Reserve has maintained its benchmark federal funds rate at its recent meetings, choosing not to implement the cuts that many analysts had anticipated earlier in the year. This decision is a direct response to the Consumer Price Index (CPI), which showed a 3.8% year-over-year increase in April 2026. Because inflation remains sticky, the Fed is unlikely to lower rates until they see a definitive move toward their stability goals.

Geopolitical tensions and fluctuating oil prices also contribute to the current environment. These external factors can lead to sudden shifts in bond yields, which are closely tied to mortgage rate movements. When the 10-year Treasury yield rises, mortgage lenders typically follow suit by raising their offered rates to maintain profitability.

Compare these economic indicators to understand the broader context of your loan application. Knowing that the Fed is prioritizing inflation control helps explain why rates are not falling as quickly as some had hoped. This knowledge is essential for timing your home purchase or refinance effectively.

Florida Market Spotlight: Impact on Sun Belt Borrowers

Florida remains one of the most active real estate markets in the country, but even the Sunshine State is feeling the effects of higher borrowing costs. In metropolitan areas like Miami, Orlando, and Tampa, price appreciation has begun to slow as buyers adjust their budgets. While demand for Florida real estate is still supported by strong migration trends, the pace of sales has tempered.

Investors in Florida are increasingly looking toward DSCR Investor Loans to navigate this environment. These loans focus on the cash flow of the property rather than the borrower’s personal income, making them ideal for scaling portfolios in high-rent areas. As property price growth plateaus, finding the right financing structure becomes even more critical for maintaining positive returns.

Explore opportunities in coastal and inland Florida where inventory is slowly increasing. This shift provides buyers with more negotiating power than they have had in years. Whether you are a first-time homebuyer or an experienced landlord, the Florida market offers diverse entry points if you utilize the correct financing tools.

Illinois Market Spotlight: Stability in the Midwest

The Illinois housing market, particularly around Chicago and its surrounding suburbs, is characterized by its relative stability compared to the more volatile Sun Belt states. Because Illinois did not see the same extreme price surges as other regions during the recent boom, the current correction is generally more moderate. Home prices in many Illinois sub-markets are currently flat or showing only modest year-over-year declines.

Borrowers in Illinois often benefit from a wide range of Non-QM Mortgage Loans and Bank Statement Loans, which are particularly useful for the state's large population of self-employed entrepreneurs. These programs allow for a more flexible underwriting process that accounts for real-world financial situations beyond standard W-2 income.

Compare different neighborhoods in the Chicago metro area to find value where inventory remains tight. For homeowners looking to tap into their accumulated equity, a HELOC (Home Equity Line of Credit) remains a strategic option for home improvements or debt consolidation without disturbing a low-rate first mortgage.

Defining Technical Financing Terms

To help you navigate these updates, here are clear definitions of common industry terms and how they apply to your journey.

DSCR (Debt Service Coverage Ratio)

Definition: A financial metric used to measure a property's ability to cover its own debt obligations through its generated income.

Application: Investors use DSCR loans to qualify for financing based on the property's rental income rather than their personal debt-to-income ratio.

LTV (Loan-to-Value)

Definition: The ratio of a loan to the value of the asset purchased, expressed as a percentage.

Application: A lower LTV often results in better interest rates and may eliminate the need for private mortgage insurance.

Non-QM (Non-Qualified Mortgage)

Definition: A category of loans that do not meet the standard criteria of "qualified mortgages" set by federal agencies.

Application: These loans provide flexible options for self-employed borrowers, ITIN holders, and investors who do not fit the traditional lending box.

Cash-Out Refinance

Definition: A mortgage refinancing option where the new loan is larger than the existing one, allowing the borrower to take the difference in cash.

Application: Homeowners use this strategy to access equity for reinvestment, large purchases, or improving their financial position.

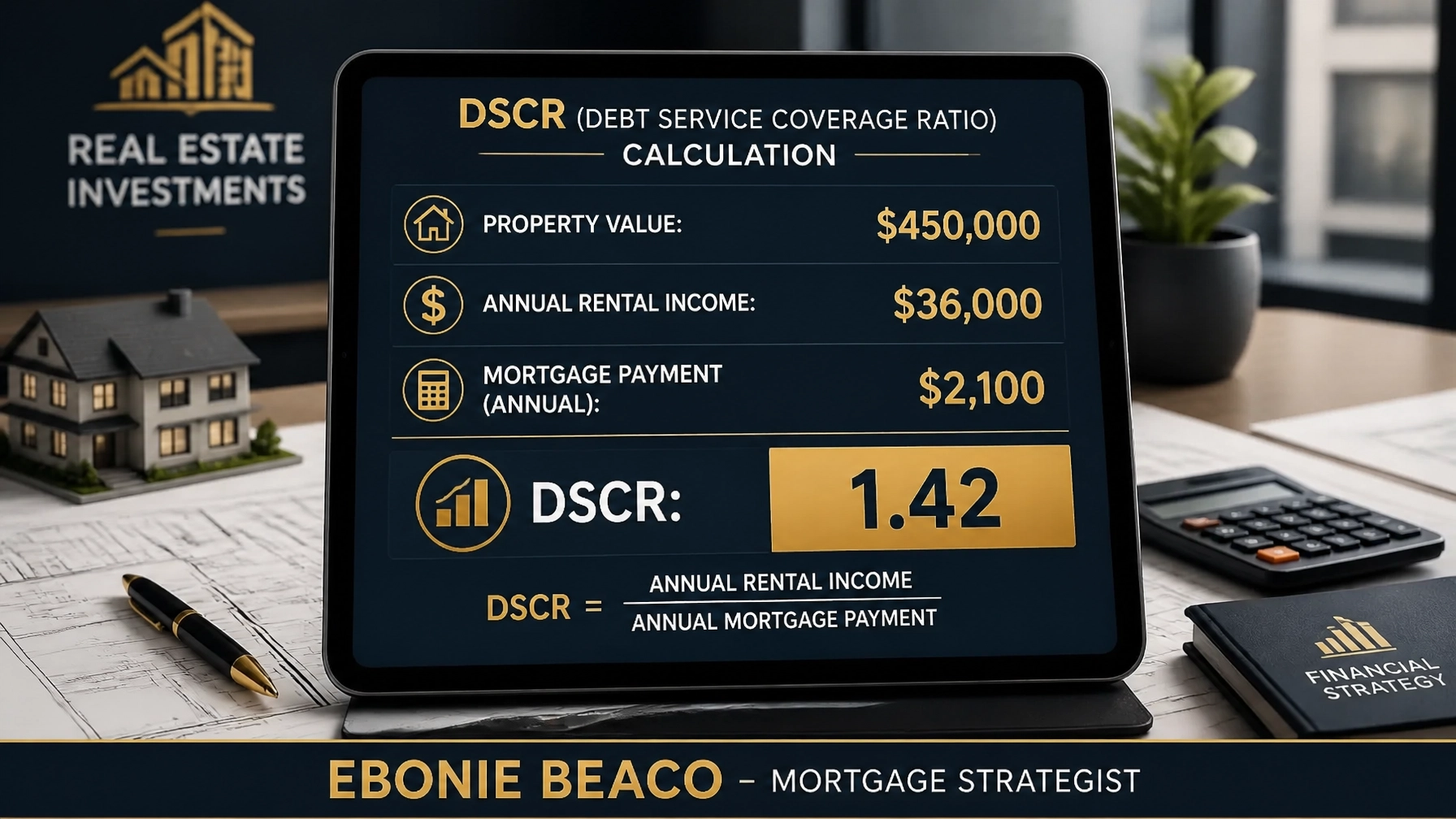

Practical Investment Example: Utilizing DSCR Loans

Consider an investor looking to purchase a rental property in a growing market like Atlanta, Georgia, or Indianapolis, Indiana. The property is valued at $450,000, and the investor plans to put 20% down, resulting in a loan amount of $360,000.

Using a DSCR loan, the lender looks at the projected annual rental income. If the property generates $36,000 per year ($3,000 per month) and the total mortgage payment (including taxes and insurance) is $2,100 per month, the DSCR is calculated as follows:

- Monthly Income: $3,000

- Monthly Debt: $2,100

- DSCR: $3,000 / $2,100 = 1.42

Because the ratio is above 1.0, the property is "covering" its debt. A ratio of 1.2 or higher is typically seen as very strong by lenders. This allows the investor to secure the loan without submitting personal tax returns or proving employment income, facilitating a faster and more efficient acquisition process.

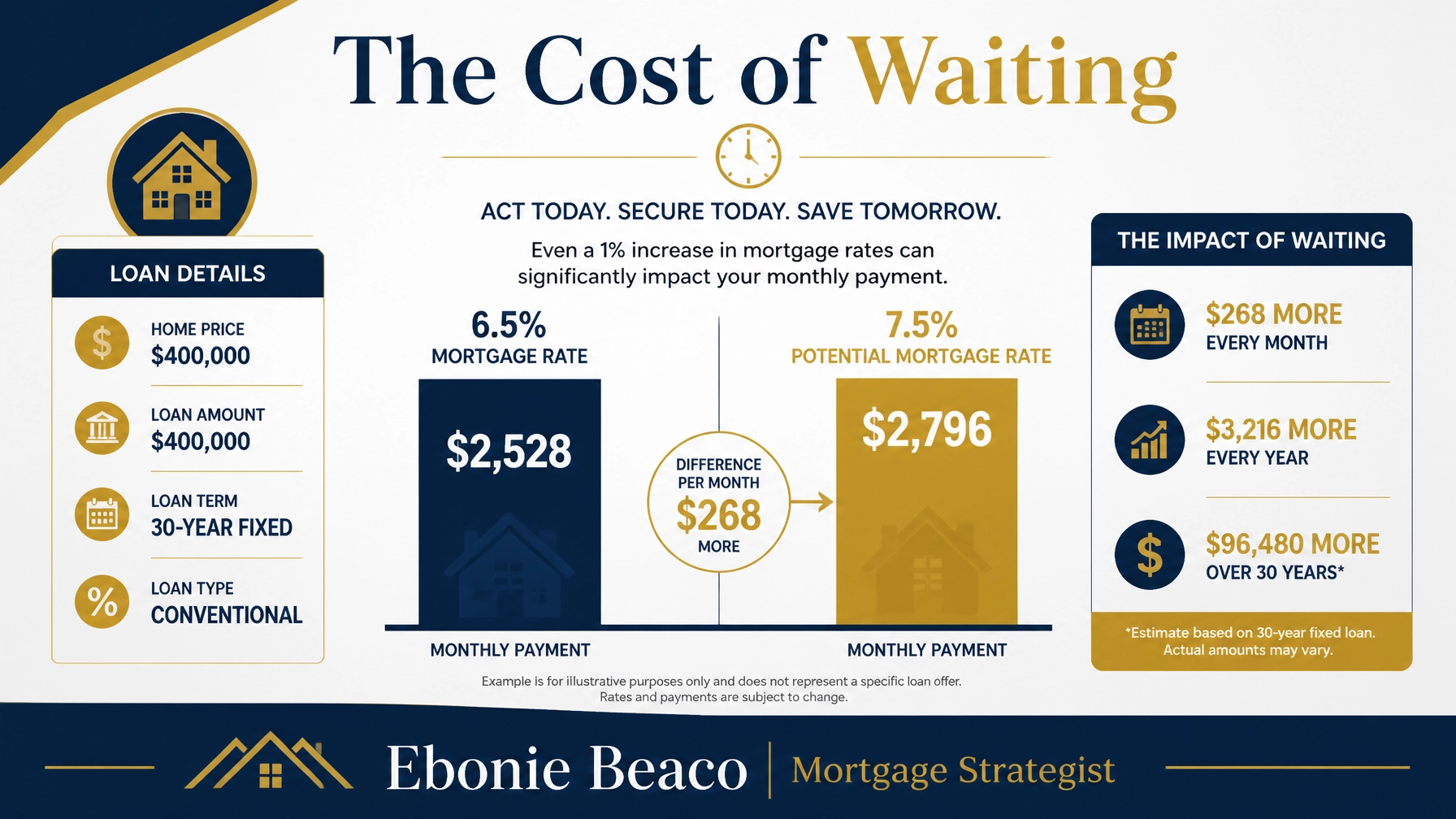

The Financial Impact of Waiting

Many prospective buyers are tempted to wait for rates to drop significantly before making a move. However, this strategy carries its own risks. If rates rise further or home prices begin to appreciate again due to limited inventory, the "cost of waiting" can exceed any potential savings from a marginally lower rate.

Analyze the difference in a monthly payment for a $400,000 loan. At a 6.5% interest rate, the principal and interest payment is approximately $2,528. If the rate were to increase to $7.5%, that same loan would cost $2,796 per month. This represents an additional $268 every month, or over $3,200 per year.

Access a mortgage calculator to run your own scenarios. Understanding these numbers helps you decide whether to lock in a rate now or continue monitoring the market. In many cases, securing a property at today's price and potentially refinancing later is a more effective long-term wealth-building strategy.

Strategic Guidance for Homeowners and Investors

Whether you are located in Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, or Virginia, the current market requires a proactive approach. Homeowners should evaluate their equity and consider if a Cash-Out Refinance or HELOC aligns with their goals. Investors should focus on finding properties where the numbers work in today's rate environment rather than banking on future rate cuts.

Explore different loan programs including Fix and Flip Loans, Bridge Loans, and Construction Financing to find the right fit for your specific project. Every real estate transaction is unique, and having access to over 240 different lenders ensures you can compare the best possible options available in the marketplace.

Jump into the process by reviewing the 7 easy steps of the loan process. Staying educated and prepared is the best way to turn market volatility into an opportunity for growth and financial stability.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664