Understanding Debt-to-Income (DTI) for Investment Loans

Navigating the world of real estate finance requires a clear understanding of the metrics lenders use to evaluate your files.

One of the most significant indicators of your borrowing health is the Debt-to-Income (DTI) ratio.

For real estate investors across markets like Chicago, Miami, and Atlanta, DTI is often the first gatekeeper you encounter when seeking traditional financing.

Whether you are looking to secure your first rental property in Arkansas or scaling a portfolio in California, mastering this calculation helps you move with more confidence.

Defining Debt-to-Income (DTI)

Debt-to-Income Ratio (DTI) A personal financial metric that compares an individual’s total monthly debt payments to their gross monthly income. Lenders use this percentage to determine how much additional debt a borrower can safely handle.

In the context of mortgage lending, your DTI provides a snapshot of your financial flexibility.

A high DTI suggests that a large portion of your income is already committed to existing obligations, which can signal higher risk to a lender.

Conversely, a lower DTI indicates that you have more disposable income available to cover a new mortgage payment.

How to Calculate Your DTI for Investment Purposes

Calculating your DTI is a straightforward mathematical process, but for investors, the components can get a bit more complex.

The basic formula is your total monthly debt divided by your gross monthly income.

Image Instructions: Title 'Understanding DTI for Investors'. Include 'Ebonie Beaco - Mortgage Loan Officer' at the bottom. No money or cash icons. Formula displayed clearly: 'DTI = Monthly Debt / Gross Monthly Income'.

Image Instructions: Title 'Understanding DTI for Investors'. Include 'Ebonie Beaco - Mortgage Loan Officer' at the bottom. No money or cash icons. Formula displayed clearly: 'DTI = Monthly Debt / Gross Monthly Income'.

To get an accurate number, you must account for all recurring monthly debts, including:

- Monthly mortgage payments (Principal, Interest, Taxes, and Insurance) on your primary residence.

- Existing mortgage payments on other investment properties.

- Auto loan payments.

- Student loan installments.

- Minimum credit card payments.

- Alimony or child support payments.

On the income side, you use your gross monthly income, which is your total earnings before taxes and other deductions are taken out.

For many investors, this calculation also includes projected or actual rental income from the property being purchased or existing units in the portfolio.

The Significance of DTI in Investment Financing

Lenders use DTI to gauge your ability to weather financial storms.

If a tenant in your Michigan duplex leaves unexpectedly, a lower DTI suggests you have enough personal income to cover the mortgage during the vacancy.

Traditional lenders, such as those following Fannie Mae or Freddie Mac guidelines, typically look for a DTI below 43% to 45%.

Some programs allow for a DTI up to 50% if you have compensating factors, such as a high credit score or significant cash reserves.

Explore your current standing by visiting our mortgage basics page to see how these ratios fit into the broader lending picture.

Rental Income and the DTI Calculation

One of the most common questions investors ask is how rental income affects their DTI.

If you are buying a rental property in Virginia or Kentucky, lenders don't just look at your W-2 salary.

They often allow you to use a percentage of the projected rental income from the new property to offset the new mortgage debt.

Typically, lenders apply a 75% vacancy factor.

This means if the property is expected to rent for $2,000 a month, the lender may credit $1,500 toward your income for DTI purposes.

This adjustment accounts for potential periods when the unit might be empty or require repairs.

DTI Limits Across Different Loan Programs

Different loan products have different appetites for debt.

Conventional Investment Loans Standard mortgage products that usually require a DTI under 45%, though 50% is possible with strong credit. These are ideal for investors with stable personal income and high credit scores.

FHA Loans (for Multi-Unit House Hacking) Government-backed loans that allow for DTIs as high as 56.9% in some cases. Many investors use these in cities like Chicago or Indianapolis to buy 2-4 unit properties, living in one and renting the others.

VA Loans Loans for veterans and active-duty members that offer flexible DTI requirements, often focusing more on residual income. This can be a powerful tool for military investors building a portfolio in Virginia or Florida.

Compare these options further on our home purchase section to see which fits your strategy.

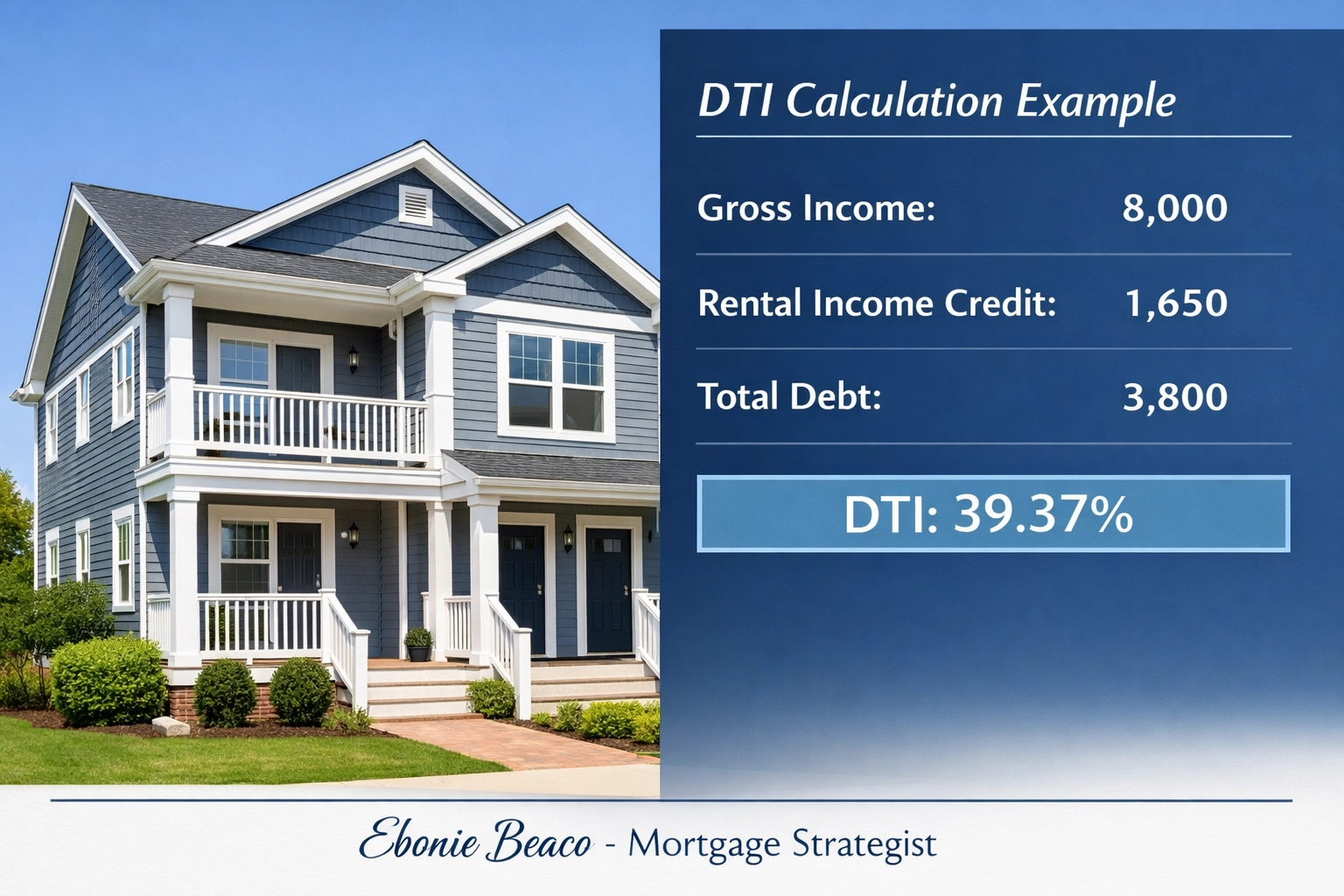

Practical Example: The DTI Calculation in Action

Let’s look at a real-world scenario for an investor looking to buy a rental property in Missouri.

The Investor's Profile:

- Gross Monthly Salary: $8,000

- Primary Mortgage: $1,800

- Car Loan: $400

- Credit Card Minimums: $100

- Total Current Debt: $2,300

The New Investment Property:

- Projected New Mortgage: $1,500

- Projected Monthly Rent: $2,200

The Adjusted Income Calculation: Lender uses 75% of the rent: $2,200 x 0.75 = $1,650. New Total Income: $8,000 (Salary) + $1,650 (Rent) = $9,650.

The New Total Debt Calculation: $2,300 (Current) + $1,500 (New Mortgage) = $3,800.

The Final DTI: $3,800 / $9,650 = 39.37%.

In this scenario, the investor qualifies comfortably under the standard 43-45% threshold.

Image Instructions: Infographic showing the deal breakdown for a Missouri rental property. Labels: Gross Income $8,000, Rental Income Credit $1,650, Total Debt $3,800, Resulting DTI 39.37%. Title: 'DTI Calculation Example'. Ebonie Beaco - Mortgage Loan Officer at the bottom. No money/cash.

Image Instructions: Infographic showing the deal breakdown for a Missouri rental property. Labels: Gross Income $8,000, Rental Income Credit $1,650, Total Debt $3,800, Resulting DTI 39.37%. Title: 'DTI Calculation Example'. Ebonie Beaco - Mortgage Loan Officer at the bottom. No money/cash.

Strategies to Lower Your DTI

If your DTI is currently too high to qualify for the loan you want, there are several ways to improve your profile.

Pay Down Installment Debts Reducing or eliminating a car loan or personal loan can significantly drop your monthly debt obligations. Focus on debts with high monthly payments but low remaining balances.

Increase Your Documentable Income If you have a side hustle or freelance work, ensure you have two years of tax returns showing that income. Lenders need to see consistency before they add that income to your DTI calculation.

Add a Co-Borrower Adding a partner or family member with strong income and low debt can dilute the DTI of the overall application. This is a common tactic for new investors in high-priced markets like California.

Refinance Existing Debt If interest rates have dropped or your credit has improved, a home refinance on your primary residence could lower your monthly payment and improve your DTI.

When DTI Becomes a Barrier: The DSCR Alternative

Sometimes, an investor’s personal DTI is simply too high, regardless of how much income the property generates.

This is common for self-employed individuals in Georgia or business owners in Alabama who take significant tax deductions.

In these cases, we look toward DSCR (Debt Service Coverage Ratio) Loans.

DSCR Loan A mortgage product that qualifies the borrower based on the cash flow of the property rather than personal income or DTI. The lender focuses on whether the rental income covers the mortgage payment (PITIA).

Jump into the details of DSCR investor loans to see how you can bypass DTI limitations entirely.

For many professional landlords, the DSCR loan is the primary vehicle for scaling a portfolio without being hindered by personal debt ratios.

Geographic Considerations for DTI and Investing

Market dynamics in different states can impact how you manage your debt.

In California, high property values mean larger mortgage payments, which can push DTI limits quickly. Investors here often rely on large down payments or interest-only options to keep the monthly debt low.

In Florida, rising insurance premiums and property taxes must be factored into your DTI. Since DTI includes the "T" and "I" of your mortgage (Taxes and Insurance), a spike in these costs can change your qualifying power overnight.

In Chicago, the prevalence of multi-unit buildings allows investors to leverage significant rental income credits, which helps keep the DTI balanced even when purchase prices are higher.

Managing DTI for Long-Term Growth

Successful investing isn't just about getting the next loan; it is about maintaining a profile that allows for continuous growth.

If you max out your DTI on your second property, you may find yourself stuck when property number three comes along.

Access mortgage calculators to run different scenarios before you commit to a new purchase.

Maintaining a healthy buffer in your DTI ensures you can take advantage of opportunities when the market shifts.

Connect for Professional Guidance

Every investor's financial situation is unique.

Whether you are looking to understand your current qualifying power or you want to discuss advanced strategies like the BRRRR method or fix-and-flip financing, professional guidance is key.

Contact Ebonie Beaco to check your qualifying power or for mentoring at www.homeloansnetwork.com.

If you have questions about how your specific debts or income sources will be viewed by a lender, let's look at the numbers together.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664