Today’s Treasury Yield: Your 7 AM Guide to Interest Rate Shifts in Florida and Georgia

As the sun rises over the coastal skylines of Florida and the bustling suburbs of Georgia, the financial landscape is already in motion. On this Tuesday, May 19, 2026, mortgage participants are closely watching the 10-Year Treasury yield as it sets the pace for the day's lending environment. Understanding these shifts is essential for homeowners looking to tap into equity and for real estate investors aiming to scale their portfolios with precision. Today's update provides a clear view of where interest rates stand and how they influence your borrowing power in the current market.

The relationship between bond markets and mortgage pricing is a fundamental driver of the real estate economy across the Southeast and beyond. When the yield on government debt climbs, the cost of financing a home or investment property typically follows suit. This morning, we are seeing a continuation of recent trends where cooling inflation data fights against persistent economic resilience. For those navigating the markets in Florida, Georgia, and other key states like Alabama and Michigan, staying informed at the start of the day is the best way to secure a competitive advantage.

Current Mortgage Rate Benchmarks: May 19, 2026

The national averages for mortgage rates today reflect a market that is searching for a new equilibrium. According to data from Bankrate, the 30-year fixed mortgage rate is currently hovering around 6.46%, while FHA options are showing slightly more flexibility at 6.26%. These figures represent a modest increase from the previous week, driven largely by the upward movement in Treasury yields. Investors looking at commercial or multi-unit properties should note that Jumbo rates are currently positioned near 6.62%, reflecting the premium required for larger loan balances.

While these national benchmarks provide a useful starting point, local pricing in Florida and Georgia often fluctuates based on regional demand and lender competition. In high-growth areas like Orlando, Tampa, and the Atlanta metro region, borrowers may find that specialized loan programs offer unique opportunities to circumvent standard rate hikes. Whether you are pursuing a conventional loan for a primary residence or a specialized product for a rental property, knowing these daily shifts allows you to time your rate lock effectively. You can explore a variety of these solutions through our Loan Programs page to find the right fit for your goals.

Defining the 10-Year Treasury Yield and Its Impact

10-Year Treasury Yield: A debt obligation issued by the United States government with a maturity of ten years, serving as a primary benchmark for long-term interest rates. In practice, this yield dictates the "floor" for mortgage rates because investors compare the risk of mortgage-backed securities against the safety of government bonds. When the yield rises, mortgage lenders must increase their rates to remain attractive to global investors who fund the housing market.

Mortgage-Backed Securities (MBS): Investment vehicles composed of bundles of home loans that are traded on the secondary market. The demand for these securities is what ultimately determines the interest rate you receive from a lender. If the 10-Year Treasury yield goes up, the price of MBS usually goes down, leading to higher interest rates for the end consumer. Monitoring this daily interaction helps you understand why your quoted rate might change between your initial inquiry and your final application.

Regional Focus: Florida and Georgia Real Estate Trends

In Florida, the housing market remains resilient despite the pressure from elevated interest rates. Investors in the Sunshine State are increasingly utilizing DSCR Investor Loans to bypass personal income requirements and focus on the cash flow potential of their properties. Cities like Jacksonville and Miami continue to see strong demand for short-term rentals and multi-unit buildings. Because Florida has a high concentration of second-home buyers and vacation rental operators, the daily shifts in Treasury yields have a direct impact on the profitability of these real estate ventures.

Georgia’s market presents a slightly different dynamic, with a focus on suburban expansion and steady appreciation in the Atlanta metropolitan area. Homeowners in Georgia are frequently looking at Cash-Out Refinance strategies to consolidate high-interest debt or fund home improvements. The current rate environment makes it crucial to compare the cost of a new first mortgage against the benefits of a second lien. For many in Georgia, maintaining a low-interest primary mortgage while accessing equity through a HELOC is becoming the preferred method for wealth preservation and growth.

Accessing Equity: The HELOC Strategy

For homeowners who secured low interest rates several years ago, the prospect of a full refinance can be unappealing. This is where a HELOC (Home Equity Line of Credit) serves as a powerful alternative for accessing the wealth stored in your property. A HELOC allows you to borrow against your home's value without disturbing your existing first mortgage. This strategy is particularly effective in states like Virginia and California, where property values have reached historic highs, leaving homeowners with significant "tapped-in" equity.

Consider a practical example of how this works in today's market. If a homeowner in Florida has a property valued at $500,000 and an existing mortgage balance of $280,000, they have $220,000 in total equity. Most lenders allow a combined loan-to-value (CLTV) of up to 85%. This means the homeowner could potentially access a credit line of $145,000 to use for property renovations, investment down payments, or other financial goals. By using a HELOC instead of a cash-out refinance, you keep your original low-interest rate on the $280,000 balance while only paying the current market rate on the funds you actually draw.

Investor Corner: Scaling with DSCR Loans

Real estate investors in markets like Indiana, Illinois, and Missouri are increasingly turning to DSCR (Debt Service Coverage Ratio) Loans. These loans are designed for landlords and portfolio builders who want to qualify for financing based on the property’s income rather than their own tax returns. This is an ideal solution for self-employed individuals or those with complex financial profiles. As Treasury yields shift, the "stress test" for a DSCR loan becomes more important, as the rental income must comfortably cover the new, higher mortgage payment.

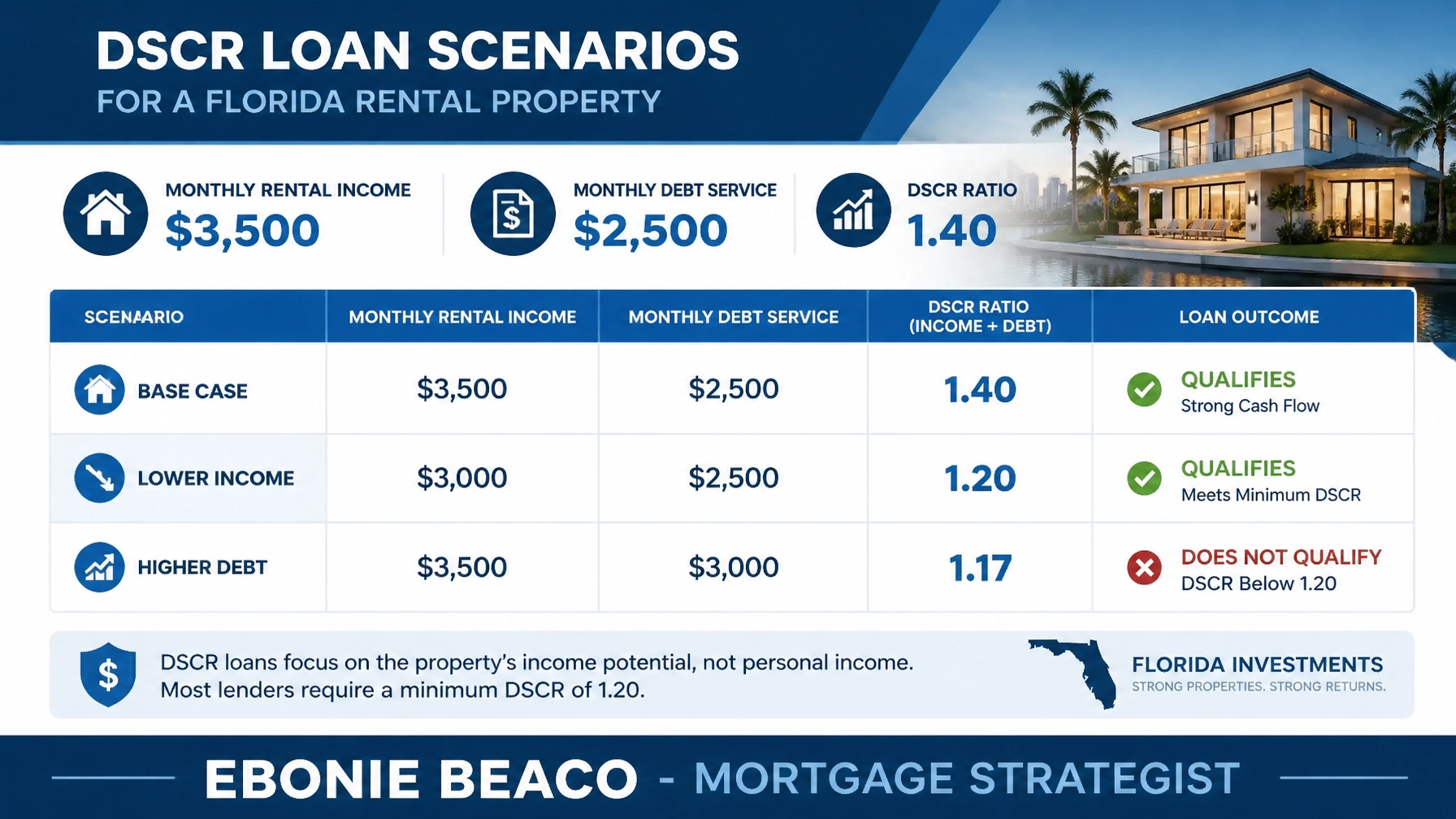

DSCR Calculation: The ratio of a property's annual net operating income to its annual mortgage debt service. To qualify for most competitive programs, investors typically look for a ratio of 1.20 or higher. For example, if a rental property in Atlanta generates $3,500 in monthly rent and the total mortgage payment (including taxes and insurance) is $2,500, the DSCR is 1.40. This healthy ratio demonstrates to the lender that the property is self-sustaining, making it a lower-risk investment even in a fluctuating rate environment.

National Perspectives: AL, AR, CA, IL, IN, KY, MI, MO, VA

While our focus today highlights Florida and Georgia, the shifts in Treasury yields ripple through every state where we provide mortgage solutions. In California, the high cost of entry makes Bridge Loans and Non-QM Mortgage Loans essential tools for buyers who need to move quickly or have non-traditional income. Meanwhile, in Michigan and Illinois, buyers are finding success with Renovation Financing and Construction Loans to revitalize older housing stock in established neighborhoods. Each region responds differently to interest rate volatility, but the underlying need for strategic financing remains constant.

Investors in Alabama and Arkansas are often focused on "Buy, Rehabilitate, Rent, Refinance, Repeat" (BRRRR) strategies. In these markets, Fix and Flip Loans provide the initial capital needed to acquire and renovate distressed properties. Once the property is stabilized and leased, the investor can transition into a long-term landlord loan. By understanding the daily 7 AM yield updates, these investors can better project their "exit" interest rates, ensuring that their long-term cash flow remains protected from sudden market shifts.

Navigating the Road Ahead

The current economic cycle requires a proactive approach to mortgage planning. Whether you are a first-time homebuyer in Kentucky or a seasoned commercial developer in Missouri, the goal is to align your financing with your long-term wealth objectives. The 10-Year Treasury yield will continue to provide the heartbeat of the mortgage market, but it is your strategy that determines your success. By monitoring these daily shifts and understanding the technical mechanics of different loan products, you can make decisions that build lasting financial stability.

Explore our Mortgage Basics guide to deepen your understanding of how these concepts apply to your specific situation. Jump in and compare options that suit your profile, from bank statement loans for the self-employed to high-leverage options for professional investors. The market is constantly evolving, and having an expert strategist by your side ensures that you are never navigating these changes alone. Access the tools and guidance you need to turn today’s interest rate environment into an opportunity for growth.

Jump in and take control of your real estate journey today. Whether you are looking to purchase a new home, refinance an existing debt, or expand an investment portfolio, we are here to guide you clearly and confidently through every step of the process.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664