Today’s National Mortgage Index Explained in Under 3 Minutes: What Georgia and Virginia Homeowners Need to Know

Navigating the housing market requires a clear understanding of where mortgage rates stand today. As of Monday, May 25, 2026, the national mortgage landscape continues to show signs of stabilization. For homeowners and investors in Georgia and Virginia, these shifts directly impact purchasing power and equity strategies.

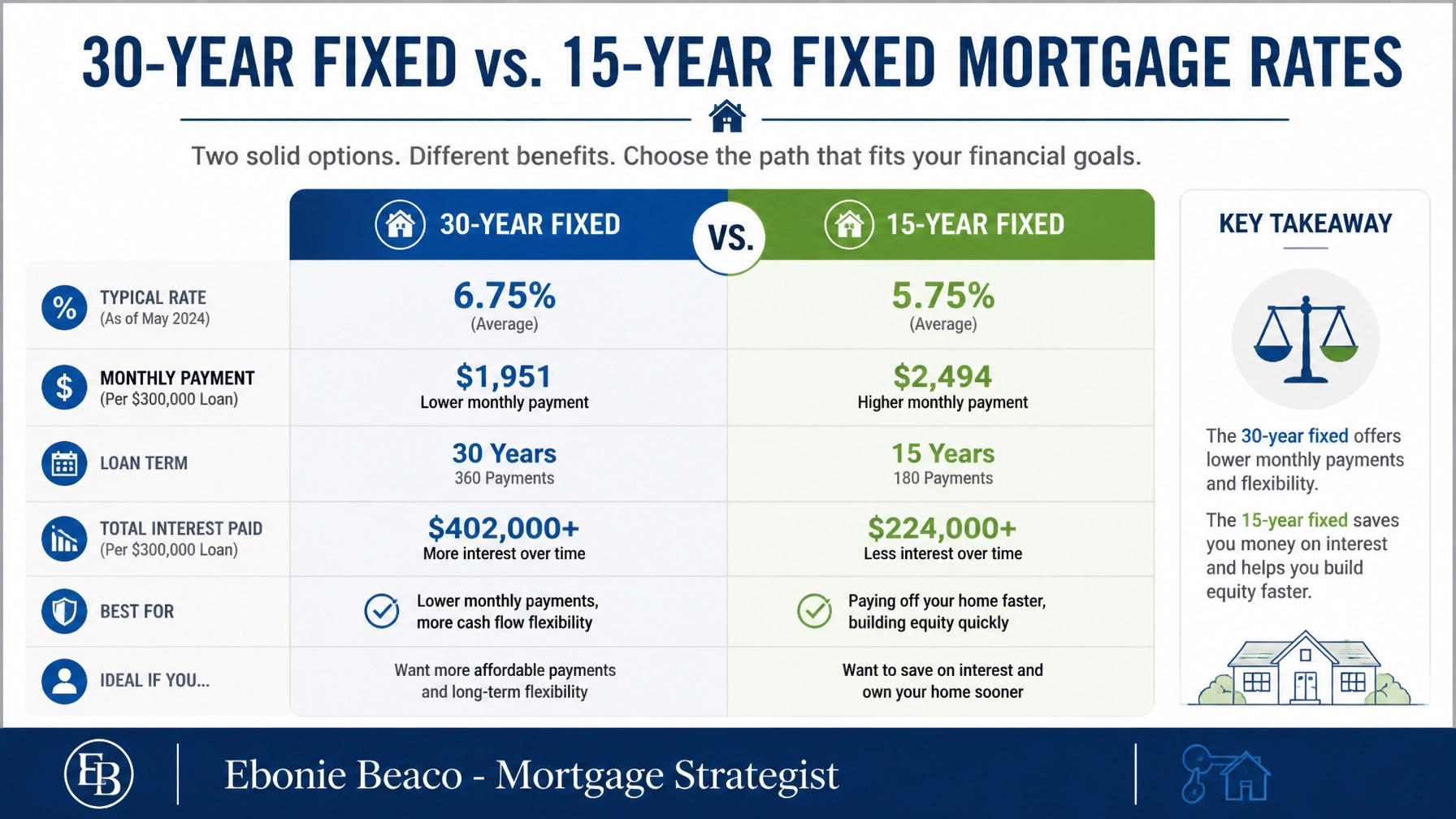

The primary benchmarks we watch closely indicate a steady environment for new originations. Current data from the Freddie Mac Primary Mortgage Market Survey (PMMS) shows the 30 year fixed national average at 6.51%. Meanwhile, daily trackers like Mortgage News Daily suggest a slightly higher average of 6.65% for some conventional products.

Understanding these numbers helps you decide when to move forward with a purchase or a refinance. These indices serve as a compass for the broader market. You can explore how these rates apply to your specific goals by reviewing our comprehensive loan programs.

Defining the National Mortgage Index (NMI)

National Mortgage Index: A statistical benchmark that tracks the average interest rates, loan volumes, or risk profiles of mortgages across the United States.

By monitoring this index, you can determine if the quotes you receive are competitive compared to the broader market. It acts as a standardized baseline for the entire lending industry.

Primary Mortgage Market Survey (PMMS): A weekly report published by Freddie Mac that averages the rates offered by lenders to well qualified borrowers.

This survey is widely considered the most authoritative "national mortgage rate" used by media and financial analysts. You can access the official weekly updates directly via the Freddie Mac PMMS website.

Why Georgia and Virginia Homeowners Should Pay Attention

Mortgage rates in Georgia and Virginia typically track very closely with the national average. While local competition among lenders can cause slight variations, the overall trend is dictated by national bond markets. If the NMI moves down, you will likely see a corresponding drop in cities like Atlanta, Savannah, Richmond, or Virginia Beach.

Current trends suggest that Virginia homeowners are seeing rates within 0.10% to 0.25% of the national benchmark. Georgia is following a similar pattern, making it a prime time to evaluate home equity. Whether you are looking at a home purchase or a refinance, knowing the NMI gives you a significant advantage.

State level differences often stem from typical loan sizes and regional closing costs. However, the direction of the market is almost always a mirror of the national data. Investors in these states often use real time indices like the Optimal Blue Mortgage Market Indices (OBMMI) to catch daily fluctuations before they hit the headlines.

Strategies for Current Homeowners

If you already own a home in Georgia or Virginia, today's index stability offers a unique opportunity. Many homeowners are sitting on significant equity that has built up over the last few years. You can use this equity to consolidate high interest debt or fund home improvements through a home refinance strategy.

Cash-Out Refinance: A mortgage refinancing option where the new loan is larger than the existing one, allowing the borrower to take the difference in cash.

This strategy is highly effective when home values have increased. It provides liquid capital that can be used for various financial goals while maintaining a single mortgage payment.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed.

A HELOC functions similarly to a credit card but uses your home as collateral. It is a flexible tool for homeowners who want access to funds without replacing their entire first mortgage.

Insights for Real Estate Investors

Real estate investors in the Southeast are leveraging today's index stability to scale their portfolios. In markets like Georgia and Virginia, the focus has shifted toward cash flow positive properties. Using specialized mortgage borrower loans tailored for investors is becoming a standard practice.

DSCR Loan (Debt Service Coverage Ratio): A loan program for investors that qualifies the borrower based on the property's rental income rather than personal income.

This is a powerful tool for scaling a portfolio quickly. It allows you to acquire more properties without the constraints of traditional debt to income ratios.

Fix and Flip Financing: Short term funding used to purchase and renovate a property with the intent to sell it for a profit.

Investors in Virginia often use these bridge loans to secure distressed properties before traditional buyers can. It provides the speed necessary to win deals in competitive metropolitan markets.

Practical Financial Example: Tapping Into Your Equity

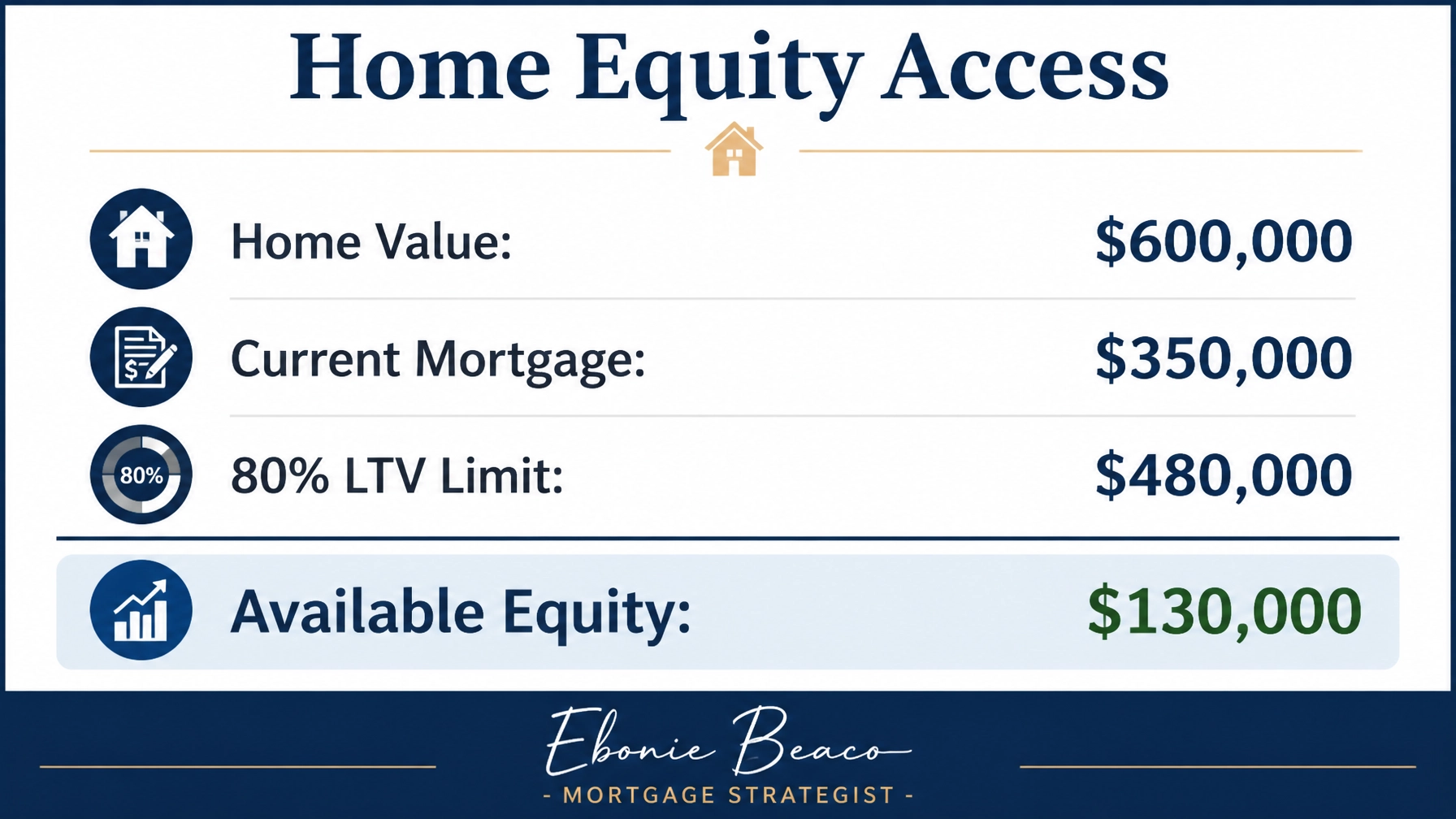

Let's look at a real world scenario for a homeowner in a thriving Virginia suburb. If your home is currently valued at $600,000 and your remaining mortgage balance is $350,000, you have $250,000 in total equity. Most lenders allow you to borrow up to 80% of your home's total value.

In this case, an 80% loan to value (LTV) limit would be $480,000. By subtracting your existing $350,000 mortgage from that limit, you find that you have $130,000 in available cash. This capital could be used to put a down payment on a new investment property or to completely renovate your current residence.

This type of equity extraction is a cornerstone of wealth building. By using the current NMI as a guide, you can time your refinance to ensure you are getting the best possible terms. Comparing these scenarios is a vital part of our loan process.

Maximizing Your Investment Potential

Investors are also finding success by focusing on Debt Service Coverage Ratios. For a property in Georgia with a purchase price of $450,000 and a monthly rental income of $3,200, the DSCR calculation is critical. If the total mortgage payment is $2,500, the DSCR would be 1.28.

A ratio above 1.20 is generally considered very strong by many lenders. This allows investors to secure financing based on the property's performance. Jump in and analyze your next deal using these benchmarks to ensure your portfolio remains profitable.

Explore your options and stay informed about daily market changes. Our team is here to guide you through the complexities of the current mortgage index. Compare your options and access the tools you need to succeed in today's market.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664