Today’s Mortgage Rates: How the Latest Market Shift Impacts Your Florida Investment Strategy

Navigating the housing market in early June 2026 requires a sharp eye on both national economic data and localized state trends. As of June 3, 2026, the mortgage landscape has entered a phase of cautious stabilization following a period of persistent upward pressure. Average 30-year fixed mortgage rates are currently hovering in the mid-6% range, specifically between 6.51% and 6.61% for well-qualified borrowers. This shift follows five consecutive weeks of rate hikes that peaked in late May, driven by "sticky" inflation and high Treasury yields. While we are seeing a slight easing from those recent peaks, the overall environment remains firmly in a "higher-for-longer" pattern that influences how investors in Florida and beyond structure their next moves.

Interest Rate

A percentage of the principal loan amount charged by a lender to a borrower for the use of assets.

In the current market, your interest rate directly determines your monthly debt service and the ultimate profitability of your real estate acquisitions.

The June 2026 Rate Landscape and Economic Drivers

The current volatility in rates is a direct response to the Federal Reserve's stance on inflation and global economic indicators. According to recent data from Mortgage News Daily, the 30-year fixed index saw a minor uptick of 0.04 percentage points today, settling at 6.61%. This follows a broader trend where investors have largely ruled out immediate Fed rate cuts, with some even pricing in a potential hike before the year concludes if inflation does not cool further. For borrowers in states like Illinois, Virginia, and Georgia, this means that waiting for a return to 3% or 4% rates is likely not a viable short-term strategy.

Professional forecasters, including those at Fannie Mae and the Mortgage Bankers Association, suggest that the average rate for the remainder of 2026 will likely sit between 6.0% and 6.4%. This projection indicates that while some relief is possible, the era of ultra-low borrowing costs has been replaced by a more balanced, albeit more expensive, credit environment. Many investors are now turning to Adjustable-Rate Mortgages (ARMs) or Non-QM solutions to bridge the gap until more significant downward movement occurs. Understanding these macro drivers is the first step in aligning your financing with long-term wealth goals in a shifting market.

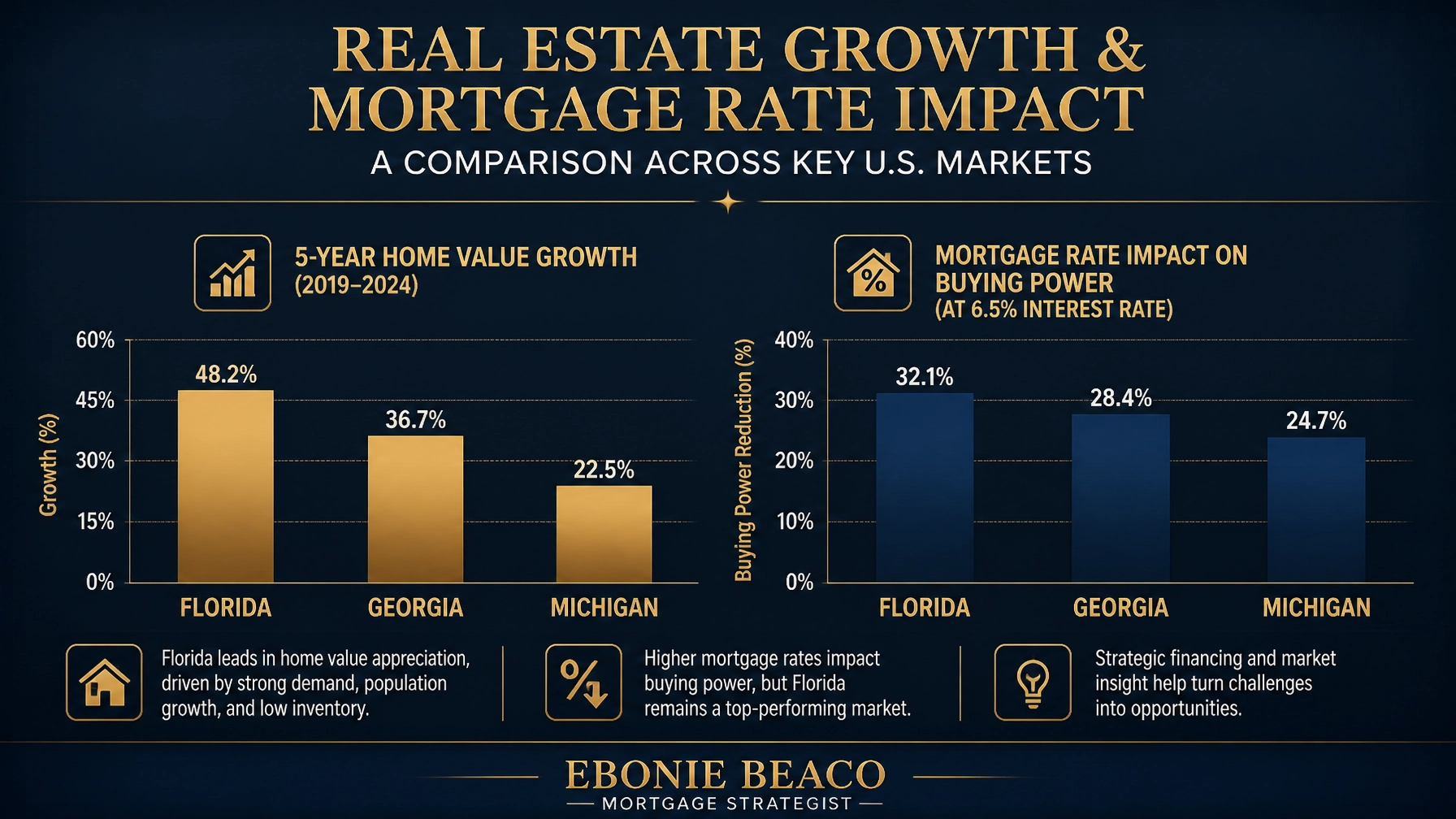

Florida’s Real Estate Pivot: From Boom to Stability

Florida remains a primary focus for both domestic and international investors, but the narrative of the market has evolved significantly this year. After a multi-year period of explosive growth, Florida is now experiencing an affordability squeeze that is reshaping demand. The influx of high-income residents into cities like Miami, Tampa, and Orlando has sustained luxury property values, but it has also made entry-level and middle-market homes increasingly difficult for local earners to acquire. This transition has led some analysts to label Florida as one of the tougher markets for typical buyers in 2026, especially compared to more affordable regions in Michigan or Indiana.

Despite these challenges, the Florida investment market offers unique opportunities for those who utilize the right mortgage strategies. Rental demand remains robust in metropolitan areas and vacation hubs, driven by the state's favorable tax climate and lifestyle appeal. However, the days of relying on rapid price appreciation alone are fading. Successful investors in Jacksonville, Naples, and Fort Lauderdale are now focusing on cash flow and yield-based metrics. This shift requires a deeper understanding of loan programs that prioritize property performance over personal income, such as the DSCR loan.

Strategic Financing for Florida Investors

In a market where traditional financing can be restrictive due to high debt-to-income (DTI) requirements, specialized investor loans have become essential tools. These programs allow investors to scale their portfolios in Florida, California, and Virginia without being limited by their personal tax returns or employment history. By focusing on the income-producing potential of the property itself, investors can navigate the mid-6% rate environment with greater flexibility.

DSCR Loan (Debt Service Coverage Ratio)

A mortgage program for investment properties that qualifies borrowers based on the property's rental income rather than personal income.

You can use this loan to acquire or refinance rental properties by ensuring the monthly rent covers the mortgage payment, which simplifies the approval process for multi-property owners.

DSCR Loans: The Solution for Rental Portfolios

The DSCR loan is currently one of the most popular choices for landlords in Alabama, Arkansas, and Kentucky. Because these loans do not require W-2s or pay stubs, they are ideal for self-employed entrepreneurs and experienced investors. In the current 6.5% rate environment, the key is to find properties where the rental income exceeds the principal, interest, taxes, insurance, and association dues (PITIA). As long as the ratio is typically 1.0 or higher, the loan can be approved based on the property’s performance.

Explore how a typical DSCR calculation looks for an investment property in a high-demand market like Orlando:

- Purchase Price: $450,000

- Down Payment (20%): $90,000

- Loan Amount: $360,000

- Interest Rate: 6.5%

- Monthly Rental Income: $3,800

- Total Monthly Mortgage Payment (PITIA): $2,900

- Calculation: $3,800 / $2,900 = 1.31 DSCR

In this scenario, a DSCR of 1.31 indicates a healthy cash-flowing property that easily qualifies for financing. This strategy is particularly effective for Short-Term Rental (STR) operators in Florida who are looking to leverage Airbnb income to secure funding for new acquisitions.

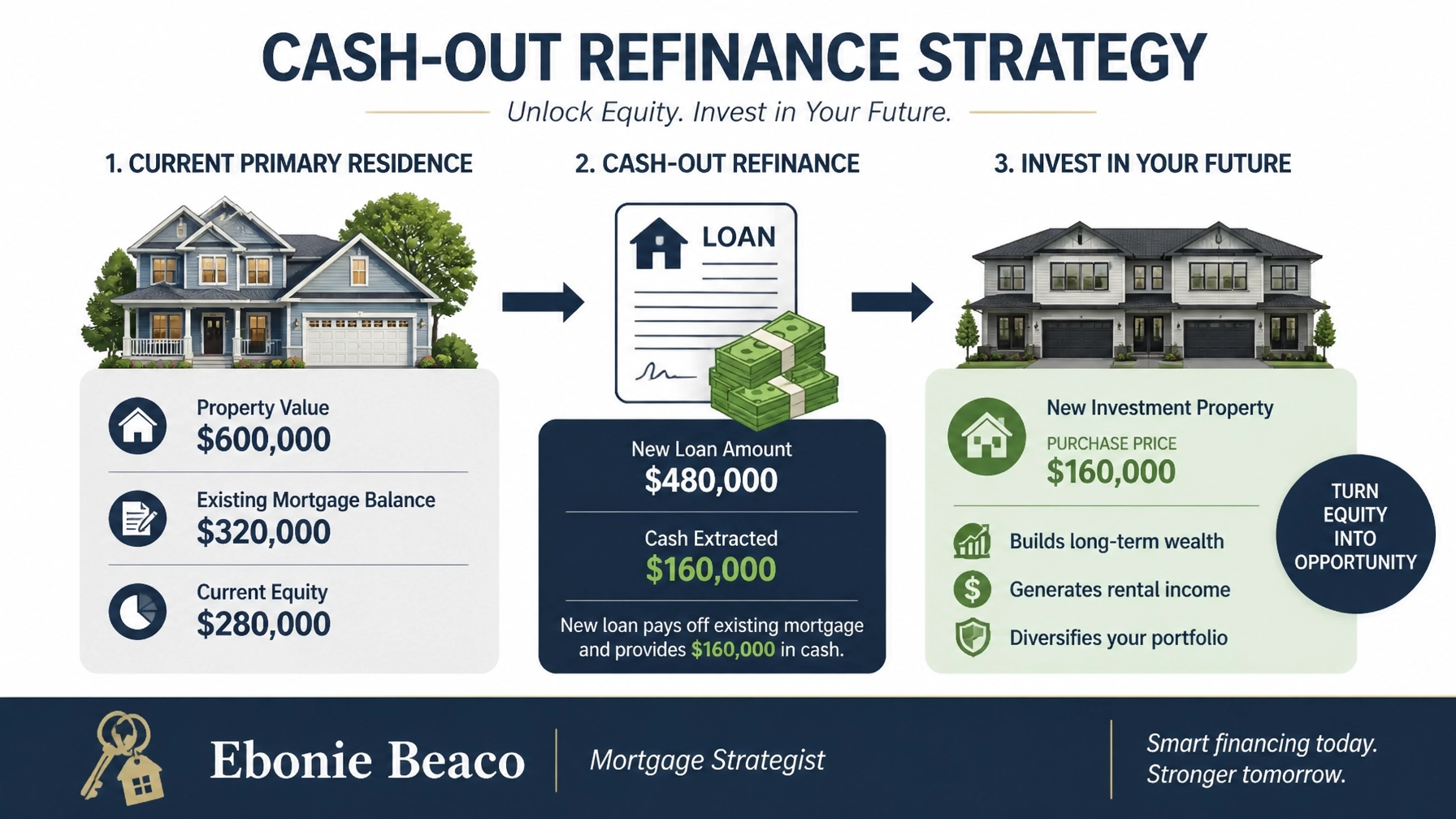

Cash-Out Refinance: Accessing Trapped Equity

Many homeowners in California and Missouri have seen significant equity growth over the last several years. Even with today's higher rates, a cash-out refinance can be a powerful wealth-building tool if the funds are used to acquire higher-yielding assets. By tapping into the equity of a primary residence or a stabilized rental property, you can generate the down payment needed for your next investment.

Cash-Out Refinance

A mortgage refinancing option where the new loan is larger than the existing one, allowing the borrower to take the difference in cash.

This strategy enables you to pull liquid capital from your property's value to fund renovations, consolidate debt, or purchase additional real estate assets.

For example, an investor in Atlanta, Georgia, might have a property valued at $600,000 with an existing mortgage of only $320,000. By performing a cash-out refinance at a 75% loan-to-value (LTV) ratio, they could secure a new loan of $450,000. After paying off the old mortgage and covering closing costs, they would have approximately $120,000 in cash. This capital could then be used as a 20% down payment on a $600,000 multi-unit building, effectively doubling their real estate holdings without using personal savings.

Navigating the Environment in Other Target States

While Florida is a major focal point, the "higher-for-longer" rate environment impacts every state differently. In Michigan and Indiana, where property prices are generally lower, the absolute impact of a 6.5% rate on the monthly payment is less dramatic than in California or Virginia. This has made the Midwest a "winner" in the current market, attracting investors who are priced out of coastal regions.

In Chicago, the market remains resilient due to its diverse economy and steady rental demand. Investors there are frequently utilizing Fix-and-Flip loans and Bridge financing to revitalize older properties in emerging neighborhoods. These short-term interest-only loans provide the capital needed for acquisition and renovation, allowing the investor to refinance into a long-term DSCR loan once the property is stabilized and appraised at a higher value.

Bridge Loan

A short-term loan used to provide immediate financing until a permanent loan is secured or an existing obligation is removed.

You can use a bridge loan to quickly close on a distressed property, complete repairs, and then transition into a traditional mortgage once the property value has increased.

Jump in and compare your options across state lines. Whether you are looking at a multi-family building in Kentucky or a condo in Miami, the strategy remains the same: align your debt structure with the property's income potential and your personal long-term financial profile. Access the expertise needed to navigate these complex scenarios by consulting with a strategist who understands the nuances of Non-QM and investor-focused lending.

Conclusion: Adapting Your Strategy for 2026

The mortgage market of June 2026 is defined by stability rather than the frantic swings of previous years. While mid-6% rates are higher than the historical lows of the early 2020s, they represent a normalizing market where deals are still abundant for the educated investor. In Florida, the shift from rapid appreciation to income-focused stability means that your financing strategy is the most critical component of your success.

By leveraging tools like DSCR loans, cash-out refinances, and bridge lending, you can continue to build wealth even in a "higher-for-longer" environment. The key is to remain proactive, stay informed on daily rate shifts, and work with a mortgage strategist who can help you navigate the specific requirements of lenders across AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA.

If you are ready to explore how today's rates impact your specific investment goals, let's connect for a personalized strategy session. We can break down your current equity, analyze your target property's income potential, and find the financing solution that fits your portfolio.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664