Today’s Mortgage Rates and Market Shifts Explained in Under 3 Minutes (June 1, 2026)

The first day of June 2026 brings a sense of stability to the housing market that many homeowners and investors have been waiting for over the past several years. After the volatility witnessed throughout 2023 and 2024, the current landscape has settled into a "new normal" where the average 30-year fixed-rate mortgage is hovering comfortably in the low-to-mid 6% range. This consistency allows for more strategic long-term planning, as the erratic swings of the previous era have largely subsided in favor of a sideways-moving market.

For those navigating real estate transactions in states like Illinois, Florida, and California, the predictability of today’s financing environment is a welcome change. While affordability remains a primary focus for many, the gradual easing of inflation has allowed the Federal Reserve to maintain a posture that supports steady, if not dramatic, market activity. Accessing financing now involves a deeper look at specific loan programs designed to optimize monthly cash flow or unlock existing home equity.

The State of 30-Year Fixed Rates

Current data from major housing indices indicates that the average 30-year fixed rate is currently sitting around 6.42%. This represents a significant improvement from the peaks of previous years, though it remains higher than the historical lows of 2021. For most borrowers, the focus has shifted from "waiting for 3%" to finding the right program that aligns with their immediate goals, such as Conventional Loans or specialized investor products.

Market analysts suggest that we are unlikely to see another sharp drop in rates this summer, as the 10-year Treasury yield continues to trade within a narrow band. This environment favors buyers who are prepared to act, particularly in competitive markets like Northern Virginia or Metro Atlanta, where inventory remains relatively tight. The strategy for many today is to secure a property with a manageable payment while keeping an eye on future refinance opportunities if the market dips further toward the 5% threshold.

Navigating Investor Strategies: DSCR and Fix-and-Flip

Real estate investors are currently leaning heavily into Debt Service Coverage Ratio (DSCR) loans to scale their portfolios without the constraints of personal income verification. These loans focus on the cash flow generated by the property itself, making them an ideal tool for landlords in high-rental-demand areas like Chicago or various coastal cities in Florida. By prioritizing the property’s performance, investors can move more quickly to acquire multi-unit buildings or short-term rentals.

The fix-and-flip market has also seen a resurgence as renovation financing becomes more streamlined. Investors in Michigan and Missouri are finding success by targeting distressed properties and utilizing bridge loans to cover both the acquisition and the rehab costs. This "buy, renovate, refinance" cycle remains a cornerstone of wealth building, especially as property values continue to show modest, single-digit growth across most of the Midwest and South.

Key Definitions for Investors

- DSCR (Debt Service Coverage Ratio): A financial metric used to determine if a property’s rental income can cover its debt obligations. This allows investors to qualify for loans based on a property’s cash flow rather than their personal tax returns.

- Bridge Loan: A short-term financing solution used until a person or company secures permanent financing or removes an existing obligation. This provides the speed necessary to win deals in competitive markets where quick closing is a priority.

Unlocking Equity: HELOC and Cash-Out Refinance

Homeowners who have seen their property values rise steadily over the last few years are now looking for ways to put that equity to work. A Home Equity Line of Credit (HELOC) remains one of the most flexible tools for financing home improvements or consolidating high-interest debt. Unlike a standard refinance, a HELOC allows you to access funds as needed while keeping your primary mortgage rate intact.

Alternatively, the Cash-Out Refinance is being utilized by those who wish to restructure their entire debt profile. In states like Georgia and Alabama, where home appreciation has been notable, many are extracting equity to fund the down payment on a second home or an investment property. This strategy effectively turns a primary residence into a funding machine for future real estate ventures.

Regional Market Snapshots

The housing market in 2026 is far from monolithic, with different regions experiencing varying levels of demand and inventory. In Illinois, particularly within the Chicago market, the demand for multi-unit properties remains high as buyers seek to offset mortgage costs with rental income. The stability of the Chicago market continues to attract both local homeowners and out-of-state investors.

In California and Florida, the focus has shifted toward Non-QM (Non-Qualified Mortgage) products. These programs serve self-employed entrepreneurs and ITIN borrowers who may not fit into the traditional lending box but possess strong assets and cash flow. As these markets continue to evolve, professional guidance is required to navigate the nuances of local regulations and specific property types, such as mixed-use or short-term rental condos.

Understanding the Financial Impact

To truly grasp how these market shifts affect your bottom line, it is helpful to look at a concrete example. Consider a homeowner in a mid-growth market like Indiana who wants to access their equity to renovate their kitchen or build an ADU (Accessory Dwelling Unit). By understanding the relationship between current property value and loan-to-value (LTV) limits, a homeowner can calculate exactly how much liquidity they have available.

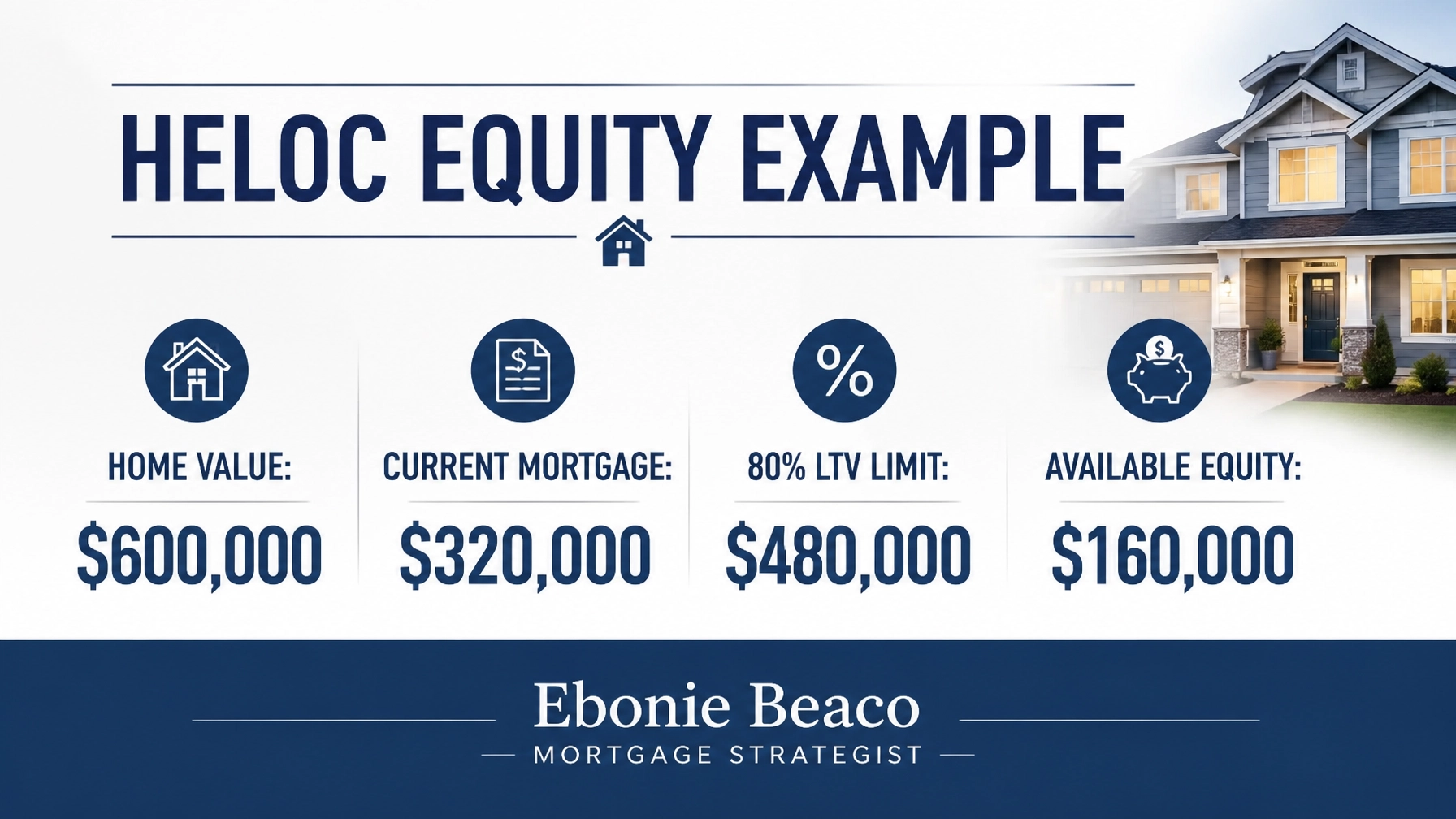

The following example illustrates a standard HELOC calculation for a property that has appreciated significantly over the last five years. By staying within an 80% LTV limit, the homeowner maintains a healthy equity cushion while still accessing a substantial amount of capital for their projects.

Home Equity Access Example

Imagine a home valued at $600,000 with an existing mortgage balance of $320,000. If a lender allows an 80% LTV, the total allowable debt on the property is $480,000. After subtracting the existing mortgage, the homeowner has $160,000 in available equity that can be accessed through a HELOC or a cash-out refinance.

Practical Guidance for Today's Market

Whether you are a first-time homebuyer or a seasoned landlord, the current environment requires a strategic approach. Explore your options by utilizing Mortgage Calculators to compare different scenarios and see how changes in rates or down payments impact your monthly commitment. Transparency in the lending process is key to making confident decisions that align with your long-term financial health.

As we move through the summer of 2026, staying informed on daily market shifts and new Loan Programs will be your greatest advantage. The goal is no longer just to find a house, but to build a comprehensive financing strategy that supports wealth creation and stability in any market condition.

Glossary of Terms

- LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased. Lenders use this to assess risk; a lower LTV generally results in better terms for the borrower.

- Cash-Out Refinance: A mortgage refinancing option where the new mortgage is for a larger amount than the existing one, and the borrower gets the difference in cash. This is a primary tool for extracting large sums of equity for significant investments.

- ITIN Loan: A mortgage designed for individuals who do not have a Social Security Number but have an Individual Taxpayer Identification Number. These loans open the door to homeownership for a broader range of hardworking residents.

Explore more about current market trends and data-driven forecasts at The Mortgage Reports and Freddie Mac.

Jump in and resolve your financing uncertainty by speaking with a strategist today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664