Today’s Mortgage Rate Volatility Explained in Under 3 Minutes

Navigating the mortgage market in early June 2026 requires a steady hand and an eye for detail as fluctuations continue to define the current lending environment. For homeowners in Virginia or investors eyeing multi-family properties in Chicago, understanding why rates shift daily is the first step in making a sound financial decision. The 30-year fixed mortgage average currently hovers in the mid-6% range, reflecting a period of relative stability punctuated by sudden, sharp movements in response to economic data. This volatility often creates a sense of urgency for those looking to secure a home refinance or a new purchase. By breaking down the core drivers of these changes, you can better position yourself to capitalize on brief windows of opportunity.

Defining Key Financial Terms

Basis Points

A unit of measure used in finance to describe the percentage change in the value or rate of a financial instrument.

One basis point is equal to 0.01%, meaning a 25-basis point shift represents a 0.25% change in your mortgage interest rate.

10-Year Treasury Yield

The return on investment for the U.S. government’s ten-year debt obligation, which serves as a primary benchmark for mortgage rates.

Mortgage lenders often track this yield closely because it reflects the market's long-term outlook on inflation and economic growth.

Volatility

The degree of variation in a trading price series over time as measured by the standard deviation of returns.

In the mortgage market, high volatility means that rates can change significantly multiple times within a single business day.

The Forces Driving Rates in June 2026

The Federal Reserve and inflation data remain the primary catalysts for the shifts we are observing this month across states like Florida, Georgia, and Michigan. While the Fed does not set mortgage rates directly, its influence on the federal funds rate creates a ripple effect that touches every corner of the housing market. As inflation cooled through 2025 and into 2026, the central bank began a series of gradual rate cuts to find a neutral ground for the economy. However, because the labor market remains resilient in metropolitan hubs like Atlanta and Detroit, the Fed has maintained a cautious stance. This caution leads to a "wait and see" approach in the bond market, which manifests as the volatility you see on your daily rate tracker.

Recent reports from Bankrate suggest that while the peak rates of 2023 are behind us, the journey toward the 5% range is not a straight line. Investors in California and Illinois are particularly sensitive to these shifts, as even a minor uptick in basis points can significantly alter the cash flow of a DSCR rental property loan. Exploring the relationship between economic indicators and your monthly payment is essential for maintaining a competitive edge in these high-demand markets. When a consumer price index report shows higher-than-expected figures, the market reacts by pushing yields up, often causing a corresponding rise in mortgage pricing within minutes. This rapid response is why many borrowers in Virginia and Missouri are choosing to lock their rates early in the application process.

Analyzing the Real-World Impact of Rate Shifts

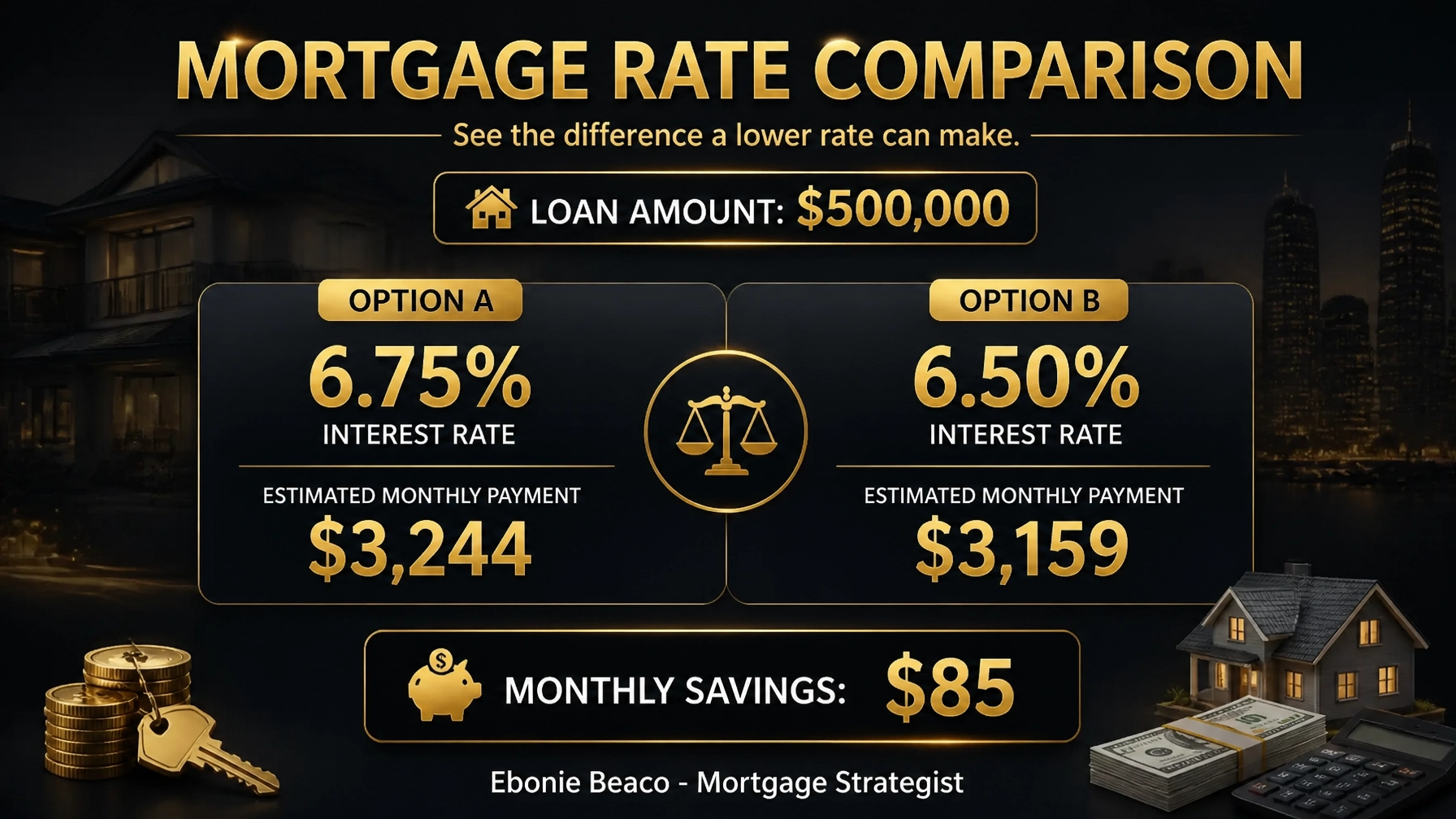

To illustrate how these small daily movements impact your financial profile, let's compare two scenarios for a standard purchase in a market like Chicago or Indianapolis. If you are purchasing a property for $500,000 with a 20% down payment, your loan amount is $400,000. At a mortgage rate of 6.75%, your principal and interest payment would be approximately $2,594 per month. If the market experiences a brief dip and you lock in at 6.50%, that payment drops to $2,528. This $66 monthly difference adds up to nearly $800 in annual savings and over $23,000 over the life of a 30-year loan. Accessing these savings requires you to stay informed and ready to act when the 10-year Treasury yield moves in your favor.

For those considering a cash-out refinance, the stakes are often even higher as they seek to tap into substantial home equity for further investments. Homeowners in Alabama and Arkansas, where property values have seen steady appreciation, often use these funds to finance the acquisition of additional rental units or to cover renovation costs. The current volatility means that the timing of your appraisal and rate lock can determine how much liquidity you actually walk away with at the closing table. Jump in and compare current options using our mortgage calculators to see how a change of just 12.5 basis points could impact your long-term wealth-building strategy.

Financing Strategies for Real Estate Investors

Real estate investors in 2026 are increasingly turning to specialized programs to navigate the current rate environment. Whether you are an Airbnb operator in Florida or a fix-and-flip specialist in Georgia, traditional financing may not always align with your timeline or income structure. DSCR investor loans (Debt Service Coverage Ratio) have become a cornerstone for landlords because they focus on the property’s rental income rather than the borrower’s personal debt-to-income ratio. This allows seasoned investors to scale their portfolios quickly, even when personal tax returns might show significant deductions. In cities like Chicago, these loans are frequently used to acquire multi-unit buildings where the rental demand remains consistently high.

Furthermore, the rise of Non-QM mortgage loans has opened doors for self-employed entrepreneurs and ITIN borrowers who may not fit the strict box of conventional lending. If you are a business owner in Michigan or Kentucky, a bank statement loan can allow you to use your gross deposits to qualify for a mortgage rather than your net income after expenses. This flexibility is vital during periods of volatility, as it ensures that financing remains available even when the broader bond market is in flux. Additionally, bridge loans and hard money loans provide the necessary short-term capital for investors to secure properties and renovate them before transitioning into long-term financing or selling for a profit.

The Long-Term Outlook for 2026 and Beyond

Looking ahead toward the end of 2026, many industry experts, including those at Fannie Mae, anticipate that mortgage rates will eventually trend toward the lower 6% or upper 5% range. This projection is based on the expectation that the spread between the 10-year Treasury yield and mortgage rates will begin to normalize. Historically, this spread has been around 1.7 percentage points, but it has remained elevated over the last few years due to market uncertainty and the Fed’s balance sheet reduction. As the market gains confidence in the path of inflation, we expect this gap to narrow, providing organic relief to borrowers across all eleven states we serve.

For the active homebuyer in California or the growing family in Virginia, the current period of volatility should be viewed as a time for preparation rather than a reason for hesitation. Markets like Chicago continue to show resilience, with inventory levels remaining the primary driver of home prices rather than interest rates alone. By working with a mortgage strategist who understands these regional nuances, you can develop a financing plan that accounts for today's rates while keeping an eye on future opportunities to refinance. Compare the benefits of a HELOC loan versus a cash-out refinance to see which tool best serves your immediate liquidity needs without sacrificing your long-term financial security.

Leveraging Home Equity in a Volatile Market

Homeowners who have seen their property values rise in states like Georgia, Florida, and Missouri often find themselves sitting on significant "dormant" wealth. A HELOC (Home Equity Line of Credit) is an excellent tool for those who want to keep their existing low-rate first mortgage while accessing cash for home improvements or debt consolidation. Because a HELOC is a revolving line of credit, you only pay interest on what you use, providing a flexible buffer against economic uncertainty. This is particularly advantageous for investors who need quick access to capital to fund a down payment on a new STR (Short-Term Rental) property or to cover unexpected maintenance on a commercial building.

In contrast, a cash-out refinance replaces your entire first mortgage with a new, larger loan. This strategy is often preferred when the new interest rate is lower than the current one or when you need a large, fixed sum of money for a long-term project. For example, an investor in Alabama might use a cash-out refinance on a fully-paid property to secure the funds needed for a "ground-up" development project. Each strategy has its place depending on your specific goals, and the current volatility makes it even more important to run the numbers with a professional who can provide clear, dictionary-style clarity on the costs and benefits of each path.

Strategic Deal Breakdown: The Cash-Out Refinance

To better understand the mechanics of equity extraction, consider this example of an investor managing a property in a high-growth area of Florida. The property was originally purchased several years ago and has appreciated significantly.

- Current Property Value: $600,000

- Existing Mortgage Balance: $350,000

- Max Loan-to-Value (LTV): 80% ($480,000)

- New Loan Amount: $480,000

- Total Cash Extracted (before costs): $130,000

With $130,000 in hand, this investor can now fund the down payments for two additional investment properties using DSCR loans, effectively tripling their portfolio's footprint. While the interest rate on the new $480,000 loan may be higher than the original 2021 rate, the wealth generated from the two new rental properties often far exceeds the increased interest expense. This is the "wealth-building" mindset that separates successful real estate investors from the average homeowner. Explore how these numbers work for your own portfolio by reviewing the visual breakdown below.

Conclusion

The mortgage rate volatility of June 2026 is a reflection of a transitionary economy. While the day-to-day changes can be frustrating, they also present unique opportunities for those who are prepared to act. Whether you are a first-time homebuyer in Michigan, a self-employed professional in California, or a seasoned investor in Chicago, your mortgage strategy should be as dynamic as the market itself. By focusing on education and technical understanding, you can navigate these fluctuations with confidence and clarity.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664