Today’s Mortgage Rate News Explained in Under 3 Minutes

The mortgage landscape as of Tuesday, June 2, 2026, continues to reflect a steady transition toward lower borrowing costs for homeowners and real estate investors. Following a series of strategic pivots by the Federal Reserve throughout the latter half of 2025 and into this spring, the market is finally seeing a more consistent downward trend in long term yields. This shift has unlocked new opportunities for those who were sidelined during the high rate peaks of 2024, particularly across high demand markets like Chicago, Miami, and Los Angeles.

For the active participant in the real estate market, understanding these daily fluctuations is critical for timing acquisitions or restructuring existing debt. Whether you are an experienced landlord managing a multi-state portfolio or a first-time buyer in Virginia or Georgia, today’s data suggests that the aggressive inflation-fighting stance of previous years has evolved into a more balanced monetary policy. This environment allows for more predictable planning regarding DSCR investor loans and cash-out refinance strategies.

Understanding Today's Rate Movement

The average 30 year fixed mortgage rate has settled into a more comfortable range, currently hovering near 6.53%, according to the latest data from Freddie Mac. This represents a significant improvement compared to the 7% levels that dominated the headlines exactly two years ago. While volatility remains a factor due to global economic indicators, the primary driver for today's pricing is the cooling of core inflation and the market’s anticipation of further easing by the central bank.

Investors should note that the spread between the 10 year Treasury yield and mortgage rates is slowly normalizing. This normalization typically leads to better pricing for Non-QM mortgage loans and bank statement loans, which are essential for self-employed entrepreneurs. As the gap narrows, lenders are becoming more competitive, offering improved terms for borrowers who may not fit the traditional W-2 profile but have strong assets and cash flow.

The Federal Reserve’s Role

The Federal Reserve's recent meetings have signaled a commitment to maintaining economic stability without over-tightening. By initiating rate cuts late in 2025, the Fed has provided the housing market with the "green light" many were waiting for. For you as a borrower, this means that while we may not return to the historic lows of 2021, the current environment is significantly more favorable for long term wealth building through real estate.

Financial analysts suggest that as the Fed continues its gradual descent, we may see more inventory enter the market. Many homeowners who were "locked in" to low rates are now finding that the current spread makes a move more palatable. This increased fluidity is a positive sign for realtors and brokers in states like Michigan, Indiana, and Missouri, where inventory constraints have historically hampered sales volume.

Strategic Implications for Investors

Real estate investors are currently pivoting their strategies to capitalize on this lower rate environment. For those focused on the "Buy, Rehab, Rent, Refinance, Repeat" (BRRRR) method, the lower cost of permanent financing makes the exit strategy much more profitable. Today’s news indicates that fix and flip loans and bridge financing are being utilized at higher frequencies as investors look to acquire distressed properties before competition intensifies further.

DSCR Loans for Landlords

The DSCR (Debt Service Coverage Ratio) loan remains the premier choice for rental property owners. These loans focus on the income generated by the property rather than the personal income of the borrower. In today’s market, higher rental rates combined with lower interest rates have improved DSCR ratios significantly, making it easier to qualify for financing on single family homes and multi-unit buildings alike.

As shown in the example above, a property generating $3,500 in monthly rent against a $2,800 PITI payment yields a DSCR of 1.25. This is a strong benchmark that many lenders look for when approving investor financing. With rates trending downward, many investors are using this opportunity to refinance their higher-rate loans from 2024 into new DSCR products to increase their monthly cash flow.

Airbnb and Short-Term Rental Financing

The short-term rental (STR) market continues to thrive in vacation destinations across Florida and California. Investors in these regions are increasingly looking at specialized STR financing that uses projected AirDNA data for qualification. With mortgage rates becoming more favorable, the ROI on these high-yield properties is becoming even more attractive to those looking to diversify their investment portfolios.

Equity Strategies for Homeowners

Homeowners who have seen significant appreciation over the last few years are now evaluating the best ways to access their equity. The two primary paths are the Cash-Out Refinance and the HELOC (Home Equity Line of Credit). Each strategy serves a specific purpose depending on your immediate financial goals and long-term investment plans.

Cash-Out Refinance vs. HELOC

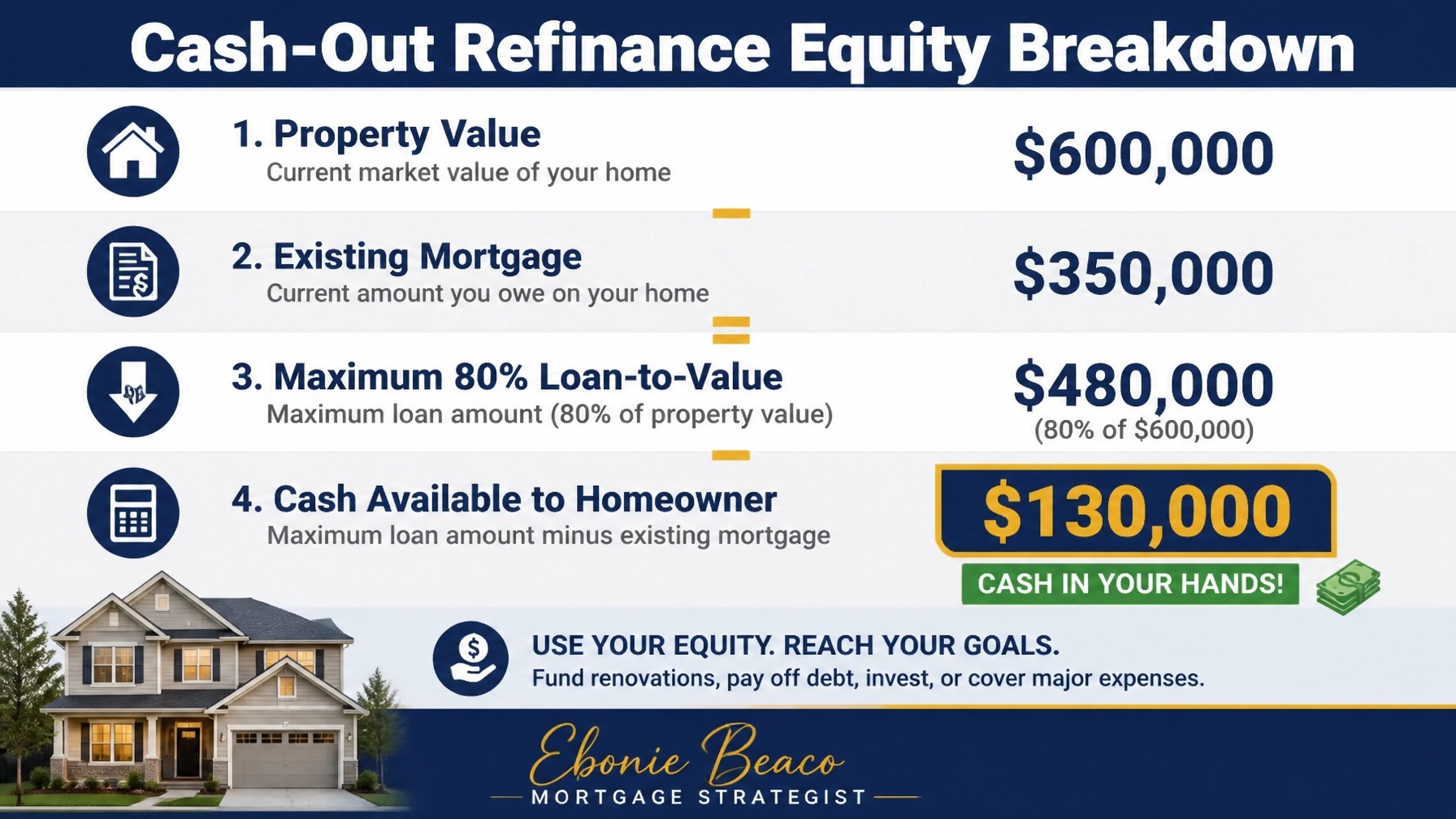

A cash-out refinance replaces your existing mortgage with a new, larger loan, allowing you to take the difference in cash. This is often the preferred route when the new interest rate is lower than your current rate, or when you need a large lump sum for a major project, such as a ground-up development or purchasing a secondary investment property.

In the scenario above, a homeowner with a $600,000 property and a $350,000 balance can access up to $130,000 in cash while staying within a conservative 80% loan-to-value (LTV) limit. This capital can be used to fund a down payment on a rental property or to perform high-value renovations that further increase the primary residence's worth.

Conversely, a HELOC acts as a revolving line of credit, similar to a credit card but secured by your home. This is an excellent tool for investors who need flexible access to funds for fix and flip projects or for homeowners who want a safety net for emergency expenses. Explore your options carefully to ensure the structure aligns with your monthly budget and tax strategy.

Regional Market Focus: AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, VA

The impact of today’s mortgage rate news varies by region, reflecting the unique economic drivers in each state. In Illinois, particularly within the Chicago metro area, we are seeing a surge in demand for multi-unit financing as investors seek to hedge against inflation with tangible assets. Meanwhile, in Florida cities like Orlando and Tampa, the focus remains on accommodating the steady influx of new residents through both new construction and sub-market acquisitions.

In the Southeast, including Alabama, Arkansas, and Georgia, the affordability of land makes construction and renovation financing a top priority. Investors in these states are utilizing bridge loans to secure land and start projects quickly, knowing they can transition into a long-term conventional or DSCR loan once the property is stabilized. In the Mid-Atlantic, Virginia continues to see strong demand from W-2 earners and government contractors who benefit from the stability of the local job market.

Definitions for the Smart Investor

To navigate the current market effectively, you must be familiar with the technical language used by lenders and strategists. Understanding these terms allows you to compare loan offers more accurately and communicate your goals clearly.

- DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments using its own rental income.

- LTV (Loan-to-Value): The ratio of the loan amount to the appraised value of the property, which determines the required down payment or available equity.

- Non-QM (Non-Qualified Mortgage): A loan that does not conform to the standard federal guidelines, often used for self-employed borrowers or those with unique financial situations.

- PITI: An acronym for Principal, Interest, Taxes, and Insurance, representing the total monthly cost of a mortgage payment.

- Escrow: A legal arrangement where a third party holds funds or assets on behalf of the two parties involved in a transaction until specific conditions are met.

Accessing the right information is the first step toward successful property ownership. Whether you are looking to purchase a single family home in Kentucky or refinance a commercial building in Indiana, staying informed about daily rate movements ensures you never miss a window of opportunity. The current trend suggests a stabilizing market that rewards proactive participants who have their financing pre-approved and their investment strategies ready for execution.

Jump in and explore the possibilities that today’s rates offer for your specific financial profile. Compare the benefits of a bank statement loan if you are a business owner, or look into down payment assistance programs if you are a first-time buyer. The path to wealth through real estate is built on consistent action and expert guidance.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664