Today’s Mortgage Rate Movement: Analyzing the Economic Impact on FL and CA Homebuyers

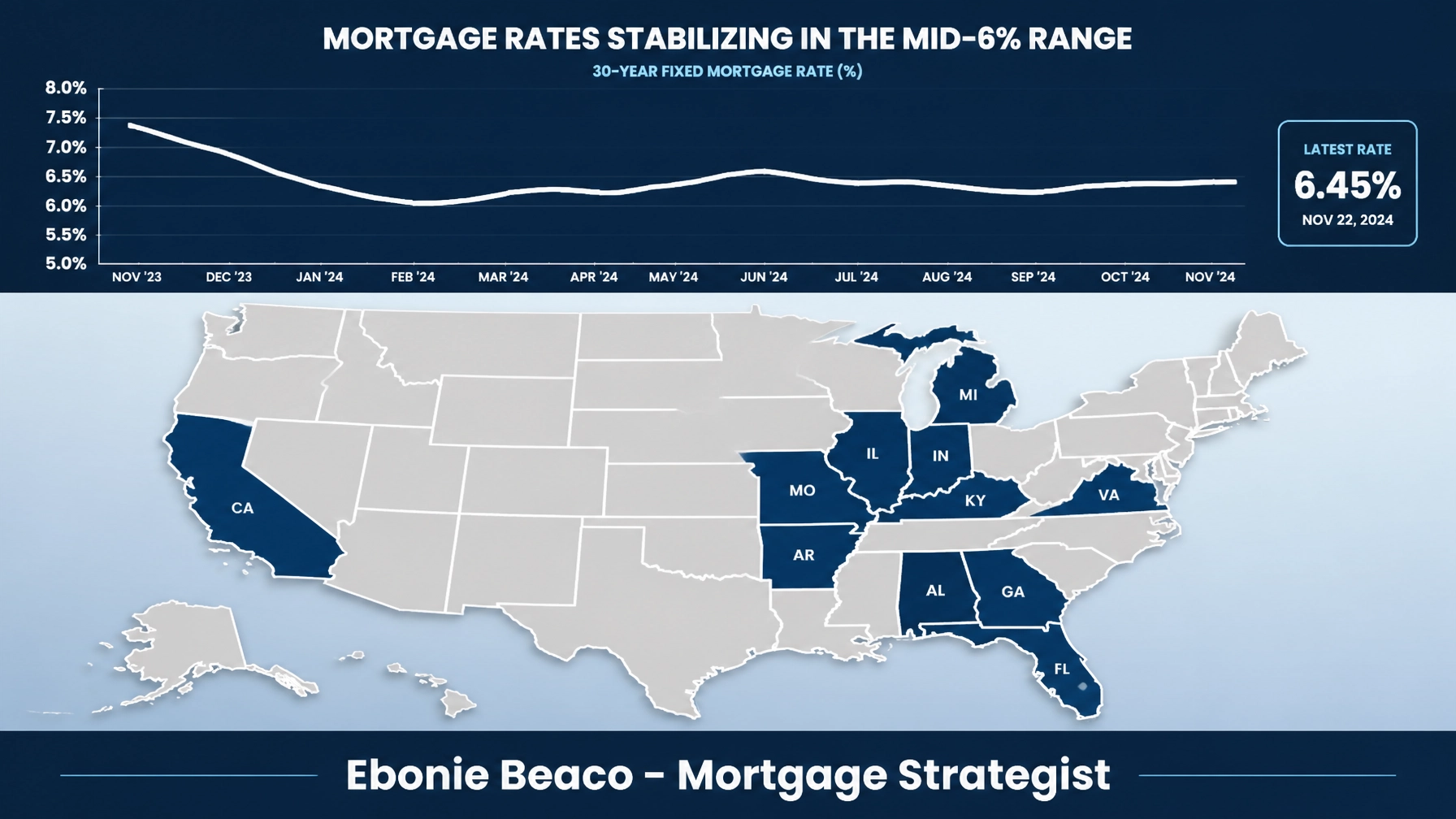

Today’s financial environment continues to present a dynamic landscape for individuals navigating the housing market. As of June 8, 2026, the 30-year fixed-rate mortgage is averaging approximately 6.48 percent, reflecting a period of relative stability after the volatility seen in previous years. This leveling off provides a critical window for homeowners and real estate investors to evaluate their current portfolios and future acquisition strategies.

Understanding these shifts is essential for anyone involved in real estate, from first-time buyers to seasoned portfolio managers. In high-demand regions such as Florida and California, even minor fluctuations in borrowing costs influence purchasing power and monthly carrying costs. While the rapid escalations of the early 2020s have subsided, the current mid-6 percent range requires a disciplined approach to financing.

Current market data indicates that national mortgage rates remain significantly lower than the peaks reached in 2023, yet they are nearly double the historic lows of 2021. This middle-ground positioning creates a unique opportunity for those utilizing Non-QM mortgage loans and equity-based financing. Exploring these options allows borrowers to bypass some of the traditional constraints associated with conventional lending.

The Florida Housing Landscape: Inventory and Investment Yields

The Florida real estate market is currently experiencing a recalibration as inventory levels adjust to the prevailing interest rate environment. In major metropolitan areas like Miami, Tampa, and Orlando, the demand for rental properties remains robust, driven by steady migration and a growing workforce. However, the intersection of mortgage rates and rising insurance premiums has shifted the focus toward more sophisticated investment vehicles.

Investors in the Sunshine State are increasingly looking toward DSCR investor loans to fund their acquisitions. These loans prioritize the property’s income potential over the borrower’s personal income, making them an ideal fit for Florida’s active short-term and long-term rental markets. By focusing on the asset's performance, investors can scale their portfolios even when personal debt-to-income ratios are high.

For homeowners in Florida, the stability in rates offers a chance to reconsider property improvements or debt consolidation. Accessing equity through a cash-out refinance or a HELOC remains a viable strategy for those who have seen their property values appreciate over the last several years. This capital can be redeployed into property upgrades that mitigate insurance costs or used as a down payment for secondary investment properties.

California Real Estate: Equity Management in High-Value Markets

California continues to lead the nation in property valuations, creating substantial equity cushions for long-term homeowners. In markets such as Los Angeles, San Diego, and the Bay Area, the challenge for many is not a lack of value, but the high cost of entry for new participants. Today’s mortgage rate movement influences how these homeowners choose to leverage their existing assets.

Many California residents are turning to HELOC loans to tap into their home's value without disturbing their existing low-rate first mortgages. This strategy is particularly effective for those who secured sub-4 percent rates during the pandemic era and now wish to access liquidity for renovations or other investments. It allows for financial flexibility while maintaining the benefits of a low-interest primary loan.

Strategic financing in California also involves the use of bridge loans and fix and flip financing. For those looking to renovate distressed properties in competitive coastal markets, these short-term solutions provide the necessary capital to move quickly on deals. Once the renovation is complete, many investors transition these properties into long-term holdings using traditional or specialized rental financing.

Technical Definitions and Practical Applications

Understanding the terminology used in real estate finance is the first step toward making informed decisions. Below are concise definitions of key concepts followed by their practical application in today’s market.

LTV (Loan-to-Value)

Definition: A financial term used by lenders to express the ratio of a loan to the value of an asset purchased.

Application: Lenders use the LTV ratio to determine the risk level of a mortgage; a lower LTV often results in better interest rates and terms for the borrower.

DSCR (Debt Service Coverage Ratio)

Definition: A measurement of a property's available cash flow to pay current debt obligations.

Application: Real estate investors use the DSCR to qualify for loans based on the property’s rental income rather than their personal tax returns.

HELOC (Home Equity Line of Credit)

Definition: A revolving line of credit that uses the equity in a home as collateral.

Application: Homeowners use a HELOC to access funds as needed for expenses like home improvements, educational costs, or as a source of capital for new investments.

Non-QM (Non-Qualified Mortgage)

Definition: A type of mortgage loan that does not follow the traditional standards set by government-sponsored enterprises.

Application: These loans are ideal for self-employed borrowers or those with unique financial profiles who require more flexible underwriting criteria.

Financial Case Study: Accessing Equity in California

To illustrate how these concepts function in a real-world scenario, consider a homeowner in San Jose, California. With property values consistently high, many owners find themselves "house rich" but in need of liquid capital for strategic growth.

- Property Value: $950,000

- Current Mortgage Balance: $480,000

- Maximum Combined Loan-to-Value (80%): $760,000

- Available Equity for HELOC: $280,000

In this example, the homeowner can establish a HELOC for $280,000. This provides a revolving line of credit that can be used to fund a down payment on a new investment property or to perform high-ROI renovations. Because the homeowner is not refinancing their primary $480,000 mortgage, they keep their existing low interest rate while gaining access to substantial liquidity.

Accessing equity in this manner is a common strategy for building wealth in high-appreciation markets. It allows for the expansion of a real estate portfolio without the need for significant out-of-pocket cash. You can explore similar scenarios using the resources available on the Home Loans Network mortgage calculators page.

Investment Strategy: DSCR Financing in Florida

Florida’s rental market provides a different set of opportunities, particularly for those focused on cash flow. When analyzing a potential rental acquisition, the DSCR is the primary metric used to determine loan eligibility and investment health.

Consider an investor purchasing a duplex in Jacksonville, Florida. The goal is to ensure the property generates enough income to cover all expenses and provide a profit margin.

- Gross Monthly Rental Income: $3,600

- Monthly Mortgage Payment (PITI): $2,800

- DSCR Calculation: $3,600 / $2,800 = 1.28

A DSCR of 1.28 indicates that the property generates 28 percent more income than the monthly debt obligation. For most DSCR investor loans, a ratio above 1.20 is considered strong and often qualifies the investor for competitive terms. This approach allows the investor to secure financing without providing personal income documentation, accelerating the acquisition process.

For more details on specific loan requirements, you can visit the Home Loans Network loan programs section. This resource provides a breakdown of various financing options tailored to different investor needs.

Regional Trends Across the United States

While Florida and California are major drivers of real estate activity, mortgage rate movement influences other states within our service area. In Alabama, Arkansas, and Georgia, lower entry prices combined with stable rates have encouraged a rise in first-time homebuyer activity. Buyers in these states often utilize FHA loans or VA loans to achieve homeownership with lower down payment requirements.

In the Midwest, including Illinois, Indiana, Michigan, and Missouri, the focus often shifts to the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). Investors in cities like Chicago and St. Louis use fix and flip loans to renovate properties and then use a cash-out refinance to pull their initial capital back out. This strategy relies heavily on understanding the current rate environment to ensure the final refinance is profitable.

Virginia and Kentucky also see significant activity in the HELOC and home equity sectors. As suburban markets in these states continue to grow, homeowners are leveraging their increased equity to fund education or second home purchases. Regardless of the location, the primary objective remains the same: aligning your financing strategy with the current market reality to build long-term wealth.

Navigating the Path Forward

The stability in today's mortgage rates provides a sense of predictability that was lacking in previous years. For homeowners, this is an opportune time to review your current mortgage terms and see if a rate-term refinance could lower your monthly obligations. For investors, the current environment allows for more accurate long-term projections of cash flow and ROI.

Successful real estate participation requires a proactive approach to financing. Jump in by reviewing your current financial profile and identifying where you have untapped equity or opportunities for acquisition. Compare different loan products, such as bank statement loans for the self-employed or ITIN mortgage loans, to find the fit that matches your specific situation.

As a mortgage strategist, my goal is to provide the educational foundation you need to navigate these decisions with confidence. Whether you are looking to purchase your first home in Michigan or expand your short-term rental portfolio in Florida, the right financing structure is the key to your success. Access the expertise and guidance necessary to turn your real estate goals into a reality.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664