Today’s Mortgage Market Update Explained in Under 3 Minutes: What Buyers in MI and MO Need to Know

Navigating the mortgage market in early June 2026 requires a sharp eye for detail as national trends continue to stabilize. For residents and investors in Michigan and Missouri, the landscape presents a unique blend of steady appreciation and accessible entry points. If you are tracking the latest shifts in interest rates and inventory, this three-minute summary provides the clarity you need to move forward with confidence.

Currently, 30-year fixed mortgage rates in Michigan and Missouri are hovering in the mid-6% range, specifically around 6.74% for conventional purchase loans. This reflects a modest improvement from the high-7% levels seen during the peak volatility of June 2024. While we have moved away from the extreme highs of previous years, the current environment remains a "higher-for-longer" reality dictated by persistent inflation and the Federal Reserve’s cautious stance on policy adjustments.

The National Macro-Economic Environment

Mortgage rates do not move in a vacuum; they respond directly to the health of the broader economy. Inflation indicators remain the primary driver of today's pricing, as the Federal Reserve seeks to anchor price growth near its 2% target. When inflation data comes in higher than expected, bond yields tend to rise, which in turn pushes mortgage rates upward.

Explore the current state of the market by recognizing that stability is the new trend. Experts anticipate that rates will stay within the 6% to 7% band for the foreseeable future, as noted in recent national mortgage forecasts. This stabilization allows buyers in states like Virginia, Georgia, and Illinois to plan their long-term financing without the fear of sudden, double-digit rate spikes.

Access the current Loan Programs at Home Loans Network to see how these national trends translate into specific financing options for your next move. Whether you are a first-time buyer or a seasoned investor, understanding the "why" behind the numbers is the first step to securing a favorable deal.

Michigan Market Insight: Resilience and Growth

The Michigan housing market remains incredibly resilient, particularly in regions like Grand Rapids, Detroit, and the surrounding suburbs. Current data shows that Michigan’s average rate for a 30-year fixed purchase is approximately 6.74%, which aligns closely with the national average. Homeowners in the Great Lakes State are increasingly looking toward equity-based strategies to fund renovations or new acquisitions.

Inventory levels in Michigan have seen a slight uptick compared to last year, yet demand remains high for well-maintained single-family homes. Many buyers are utilizing Non-QM Mortgage Loans and Bank Statement Loans to qualify, especially those who are self-employed or have complex tax returns. These programs bypass traditional W-2 requirements, focusing instead on actual cash flow to determine eligibility.

Jump in and review the Michigan mortgage rates to see how your local area compares. By focusing on property-specific value and long-term equity growth, Michigan buyers are finding ways to navigate the current rate environment successfully.

Missouri Market Insight: Opportunities for Investors

In Missouri, the story is one of opportunity and affordability. Cities like St. Louis and Kansas City continue to attract real estate investors due to their strong rental yields and stable property values. The average 30-year fixed rate in Missouri matches Michigan at 6.74%, making it a competitive environment for those looking to expand their portfolios.

Missouri’s market is particularly well-suited for the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). Investors are finding that while purchase rates are higher than they were five years ago, the rental demand remains robust enough to support healthy cash flow. Financing solutions like DSCR Investor Loans allow these professionals to qualify based on the property’s income potential rather than their personal debt-to-income (DTI) ratio.

Compare your options by looking at Different Borrower Types we support. Missouri offers a diverse range of properties, from urban multi-units to rural single-family homes, all of which can be financed through tailored lending strategies designed for the 2026 market.

Essential Industry Definitions

- DSCR (Debt Service Coverage Ratio): A metric used to evaluate a property's ability to cover its own debt payments with rental income. Use this to qualify for investment loans without providing personal income tax returns.

- HELOC (Home Equity Line of Credit): A revolving credit line secured by the equity in your primary residence. Access these funds to pay for home improvements or as a down payment for your next investment property.

- DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying debts. Monitor this closely to ensure you meet the qualifying thresholds for conventional or FHA financing.

- LTV (Loan-to-Value): The ratio of the loan amount to the appraised value of the property. Maintain a lower LTV to secure better interest rates and avoid private mortgage insurance (PMI).

Maximizing Home Equity in 2026

If you already own a home in Michigan or Missouri, you likely have a significant amount of equity built up from the past few years of appreciation. Homeowners are currently choosing between a Cash-Out Refinance and a HELOC to access this wealth. While a cash-out refinance replaces your entire mortgage, a HELOC functions as a second lien, allowing you to keep your existing low-interest first mortgage intact.

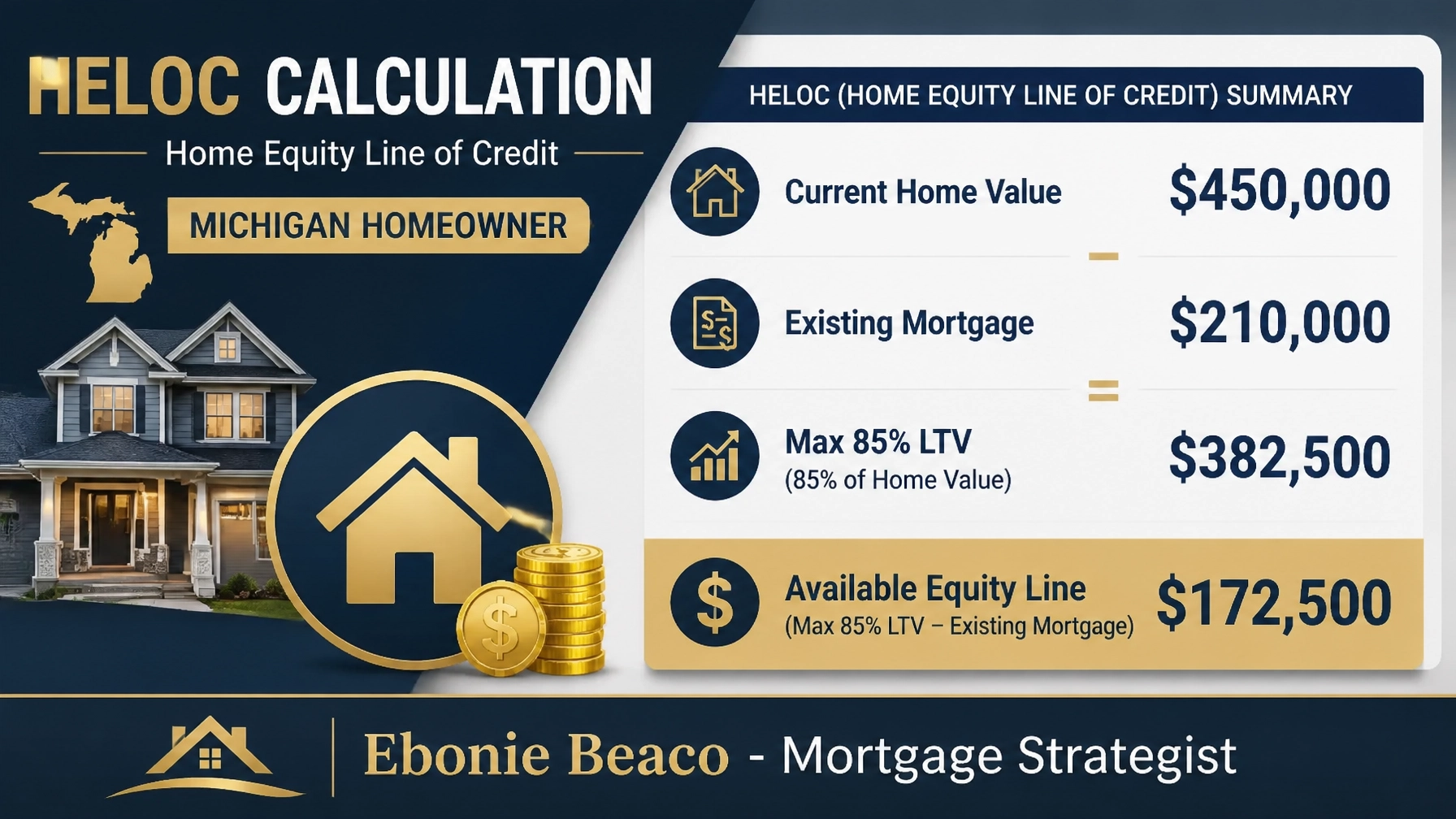

Consider the following calculation to see how much equity you could potentially unlock:

As shown in the example above, a Michigan homeowner with a property valued at $450,000 and an existing mortgage of $210,000 could potentially access over $172,500 through a HELOC, assuming an 85% Loan-to-Value limit. These funds are frequently used by savvy homeowners in Florida, California, and Indiana to acquire short-term rental properties or to consolidate high-interest credit card debt.

Strategies for Real Estate Investors

For investors looking to acquire new doors in Missouri or Michigan, DSCR Rental Property Loans are the gold standard. These loans focus on the cash flow of the asset. If the property's monthly rent exceeds the monthly mortgage payment (including taxes, insurance, and HOA fees), the deal is often eligible for financing.

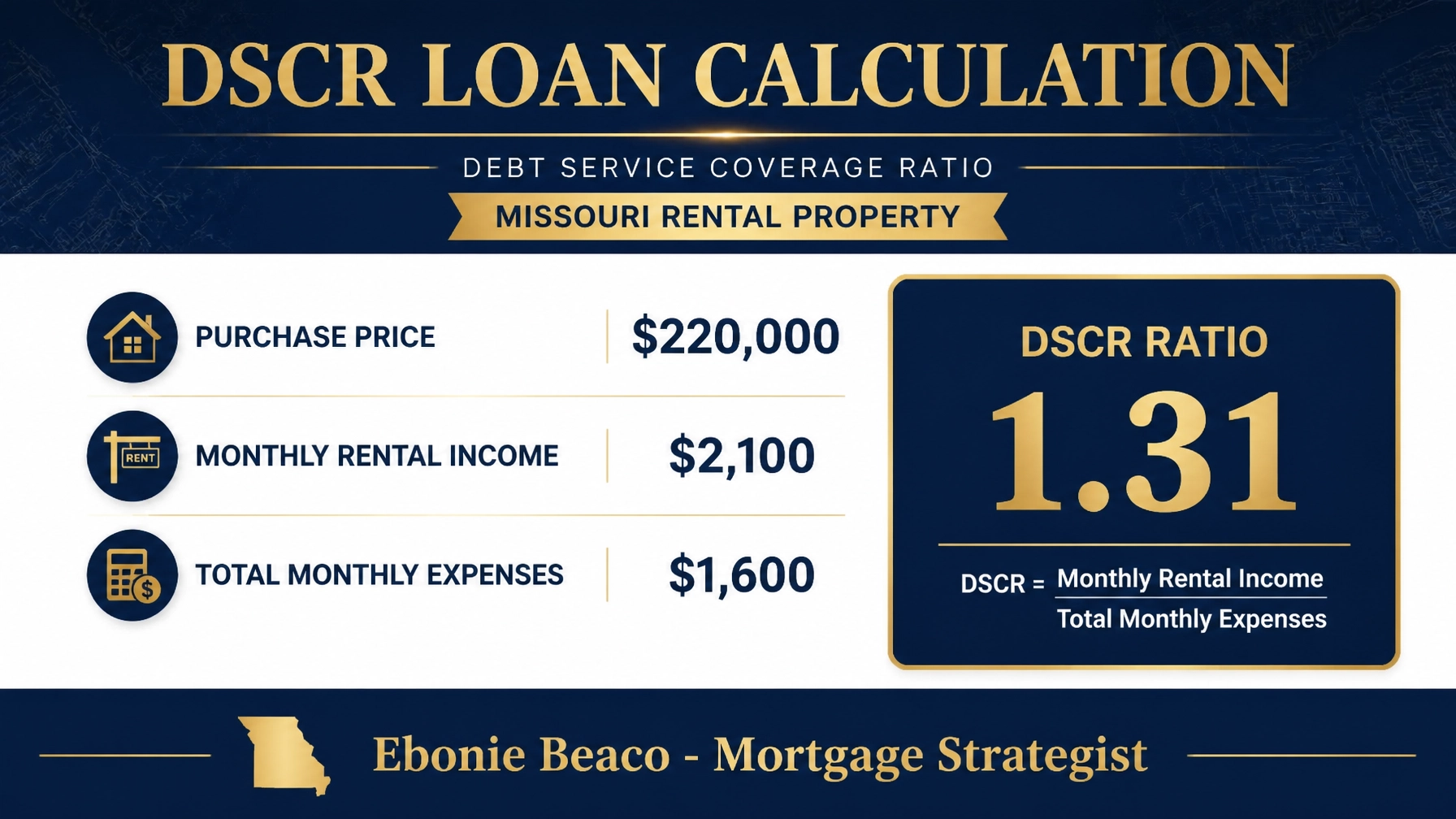

Analyze the potential of a Missouri rental property with this scenario:

In this Missouri example, a purchase price of $220,000 with a monthly rental income of $2,100 and expenses of $1,600 results in a 1.31 DSCR. This strong ratio indicates a healthy investment that would easily qualify for long-term financing, providing the investor with immediate cash flow and long-term appreciation potential.

Navigating the Road Ahead

The 2026 mortgage market requires a proactive approach. Whether you are dealing with Fix and Flip Financing in Alabama, seeking Bridge Loans in Arkansas, or exploring Commercial Real Estate Loans in Kentucky, the key is to have a clear strategy and a reliable lending partner.

Building wealth through real estate is a marathon, not a sprint. By staying informed on the latest market updates and utilizing specialized loan programs like Airbnb and Short-Term Rental Financing, you can stay ahead of the curve. The current stability in the 6% range offers a predictable window for those ready to take action.

Are you ready to explore your financing options in Michigan, Missouri, or beyond?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664