Today’s Mortgage Market Shifts Explained in Under 3 Minutes: What Buyers Need to Know Right Now

The landscape of real estate financing continues to evolve as we move into the second quarter of 2026. Understanding the current momentum of interest rates and inventory availability is essential for anyone looking to acquire or refinance property. This update provides a concise look at the economic indicators driving today’s mortgage environment and how they influence your borrowing power.

While the volatility seen in previous years has largely subsided, the "new normal" of the housing market requires a more strategic approach to leverage. Whether you are a first-time homebuyer in Virginia or a seasoned investor scaling a portfolio in Florida, current data suggests a market characterized by stabilization. Explore the latest insights to align your financial goals with today’s lending realities.

The Current State of Interest Rates and Inflation

Recent reports from the Federal Reserve indicate that inflation has entered a phase of sustained moderation, which has allowed mortgage rates to settle into a predictable range. As of June 2, 2026, the 30-year fixed mortgage rate has shown a slight downward trend compared to the previous month. This easing provides a window of opportunity for borrowers who were previously sidelined by higher borrowing costs.

The relationship between the 10-year Treasury yield and mortgage pricing remains tight, reflecting a market that is cautiously optimistic about long-term economic growth. For homeowners looking to restructure debt, this period of stability makes it an opportune time to review home refinance options. Accessing professional guidance can help you determine if a lower rate or a term adjustment fits your current profile.

Despite the softening of rates, home prices in major metropolitan areas continue to hold firm due to persistent inventory shortages. This "sideways" movement in pricing means that while financing may be slightly more affordable, the competition for quality properties remains high. Buyers should remain prepared to act quickly when the right opportunity arises in their local market.

Market Dynamics Across Key Regions

Real estate activity varies significantly by geography, with the Midwest and Southeast showing particularly strong resilience. In Chicago, the demand for both residential and multi-unit properties remains robust as the city continues to attract corporate investment and a growing workforce. You can access detailed Chicago neighborhoods market reports to see how specific districts are performing this season.

In states like Florida and Georgia, the influx of new residents is driving a surge in construction and a high demand for Short-Term Rental (STR) financing. Investors in these regions are increasingly looking toward specialized products that can account for the unique income potential of vacation properties. Exploring diverse Non-QM mortgage loans can often provide the flexibility needed to secure these types of assets.

Meanwhile, the markets in California and Virginia are seeing a rise in "move-up" buyers who are leveraging substantial home equity. These individuals are utilizing bridge loans or HELOCs to secure their next primary residence before selling their current one. This strategy allows for a seamless transition in a market where timing and liquidity are often the deciding factors in a successful transaction.

Specialized Financing for Real Estate Investors

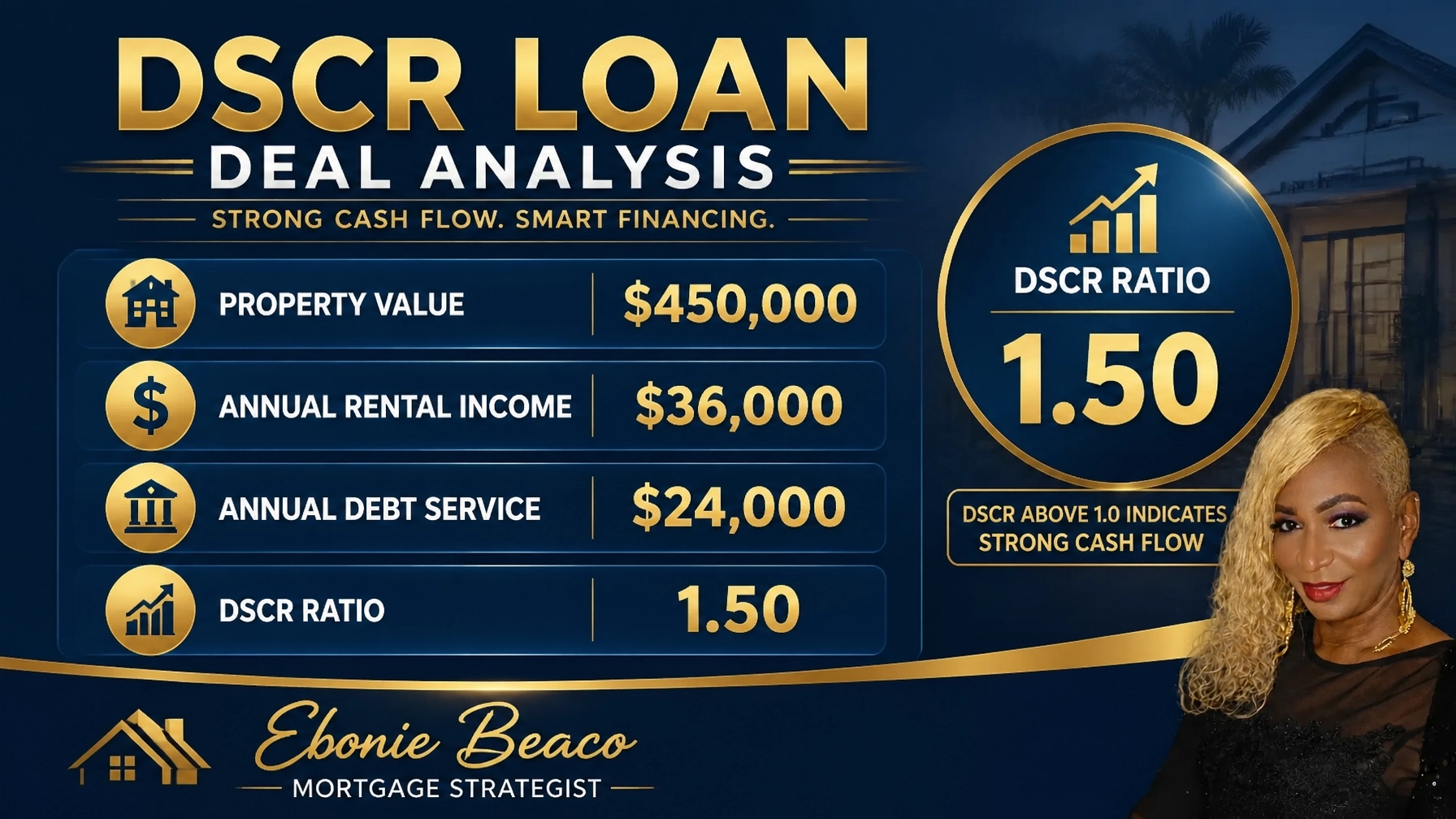

For the active real estate investor, the shift in market sentiment has brought a renewed focus on cash flow and debt coverage. Many landlords are moving away from traditional conventional loans in favor of DSCR (Debt Service Coverage Ratio) investor loans. These programs prioritize the property’s ability to generate income over the borrower’s personal debt-to-income ratio.

Consider the following scenario for a rental property acquisition:

- Property Value: $450,000

- Annual Rental Income: $36,000 ($3,000 per month)

- Annual Debt Service (Principal, Interest, Taxes, Insurance): $24,000 ($2,000 per month)

- Calculation: $36,000 / $24,000 = 1.50 DSCR

In this example, the property produces 50% more income than is required to cover its monthly debt obligations. Lenders typically look for a DSCR of 1.20 or higher, making this a highly attractive scenario for financing. Investors focusing on fix-and-flip or BRRRR strategies can use these metrics to project the long-term viability of their holdings. Jump in and use our mortgage calculators to run your own scenarios.

Technical Definitions for the Informed Borrower

To navigate the current mortgage market effectively, it is helpful to understand the core terminology used by lenders and strategists. Clear definitions help you communicate more effectively during the application process.

- DSCR (Debt Service Coverage Ratio): A measurement used to assess a property’s ability to cover its own debt payments based on rental income. It is the primary qualifying metric for many landlord loans.

- DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying your monthly debt obligations. This is a critical factor for conventional and FHA loan approvals.

- LTV (Loan-to-Value Ratio): The ratio of the loan amount to the appraised value of the property. Lenders use this to determine the level of risk and the required down payment.

- Non-QM (Non-Qualified Mortgage): A type of loan that does not conform to the standard federal guidelines. These are often used by self-employed borrowers or investors who need alternative income documentation.

- PMI (Private Mortgage Insurance): Insurance that protects the lender if the borrower defaults. It is typically required on conventional loans with a down payment of less than 20%.

Strategic Equity Use for Homeowners

Homeowners in states like Indiana, Michigan, and Missouri have seen steady equity growth over the past few years. This accumulated wealth can be accessed through a HELOC (Home Equity Line of Credit) or a Cash-Out Refinance to fund home improvements, consolidate high-interest debt, or provide a down payment for an investment property.

Let’s examine how a homeowner might access their equity in today’s market:

- Current Home Value: $600,000

- Existing Mortgage Balance: $350,000

- Maximum Combined Loan-to-Value (CLTV) at 80%: $480,000

- Calculation: $480,000 - $350,000 = $130,000 in Available Equity

By establishing a HELOC, the homeowner can access up to $130,000 as needed, only paying interest on the amount they actually use. This is a powerful tool for those looking to maintain liquidity while their primary asset continues to appreciate. Compare your current position with our loan programs to see which equity product aligns with your 2026 financial plan.

Moving Forward with Confidence

The shifts in the 2026 mortgage market suggest a period of maturity and opportunity. While the era of record-low rates is behind us, the current stability allows for more precise financial planning and long-term wealth building. By understanding the regional nuances and the specialized loan programs available, you can position yourself to succeed in any market condition.

The data provided by the National Association of Realtors continues to highlight that real estate remains a cornerstone of financial security for American families and investors alike. As you evaluate your next move, remember that the right financing strategy is as vital as the property itself. Focus on your long-term objectives and utilize the tools available to make informed, confident decisions.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664