Today's Market Insight: What This Morning's Rate Shift Means for Your Next Closing

The mortgage landscape moved again this morning, continuing a trend of volatility that has defined the final weeks of May 2026. As financial markets opened, the 10-year Treasury yield: the primary benchmark for 30-year fixed mortgage pricing: saw a notable uptick in response to fresh inflation data and ongoing geopolitical shifts in the Middle East. For homebuyers and real estate investors across the country, particularly in high-activity regions like Illinois, Florida, and California, these shifts necessitate a proactive approach to rate locking and deal structuring. Understanding the "why" behind these movements is the first step in protecting your bottom line and ensuring your next closing stays on track.

Current data from major trackers indicates that the average 30-year fixed conforming rate is currently hovering between 6.5% and 6.7%, a significant rise from the 6.09% lows we witnessed in mid-February. Recent reports from Fortune suggest that the average for a 30-year fixed loan settled near 6.483% just yesterday, though individual quotes vary based on credit profile and loan type. This drift higher is largely attributed to the Federal Reserve’s decision to keep the federal funds rate at 3.50% to 3.75%, citing a persistent need to cool inflationary pressures that remain stubbornly above target. When inflation readings come in higher than anticipated, bond investors demand higher yields, which directly translates to the mortgage rates you see at the kitchen table.

Navigating the Rate Shift Across the States

Whether you are looking at a condo in downtown Chicago, a single-family home in the suburbs of Atlanta, or a coastal investment property in Virginia, the impact of these rate shifts is felt locally. In states like Indiana, Michigan, and Kentucky, where property values remain competitive, even a small increase in the interest rate can alter the monthly payment enough to shift a buyer's debt-to-income (DTI) ratio. Meanwhile, in higher-priced markets like California and Florida, a 0.25% move can represent hundreds of dollars in monthly carrying costs, making current market insight vital for those in the middle of a home search. Explore the current landscape of mortgage programs to see how different products can mitigate these rising costs.

For those looking at government-backed options, FHA and VA loans continue to offer a slight buffer against the peak of conventional rates. Currently, FHA 30-year fixed rates are averaging approximately 6.248%, while VA rates remain even more attractive for eligible veterans, often landing near 6.093% according to Bankrate. These programs remain essential tools for first-time buyers in Missouri, Arkansas, and Alabama who are looking for lower down payment options and more flexible credit requirements. Jump in and compare these government-backed programs against conventional financing to determine which path offers the best long-term stability for your specific financial profile.

Strategic Financing for Real Estate Investors

Real estate investors are feeling the pinch of higher rates, but they are also finding unique ways to pivot using specialized loan products. The DSCR (Debt Service Coverage Ratio) loan has become a favorite for landlords in Georgia and Virginia because it allows for qualification based on the property's rental income rather than the borrower's personal tax returns. This is particularly useful for Airbnb and short-term rental operators who may have high gross revenues but significant business deductions that can complicate a standard W-2 loan application. By focusing on the property's ability to cover its own debt, investors can continue to scale their portfolios even when rates are not at historic lows.

Another critical strategy for current property owners is the Cash-Out Refinance. Even with rates in the mid-6% range, many investors in the Midwest and South have seen substantial equity growth over the last three years. Extracting that equity to fund a Fix and Flip project or to provide the down payment for a new acquisition can be a more efficient move than waiting for rates to drop. This is especially true for Non-QM Mortgage Loans, which offer the flexibility that modern entrepreneurs and self-employed borrowers require to stay competitive in a fast-moving real estate market.

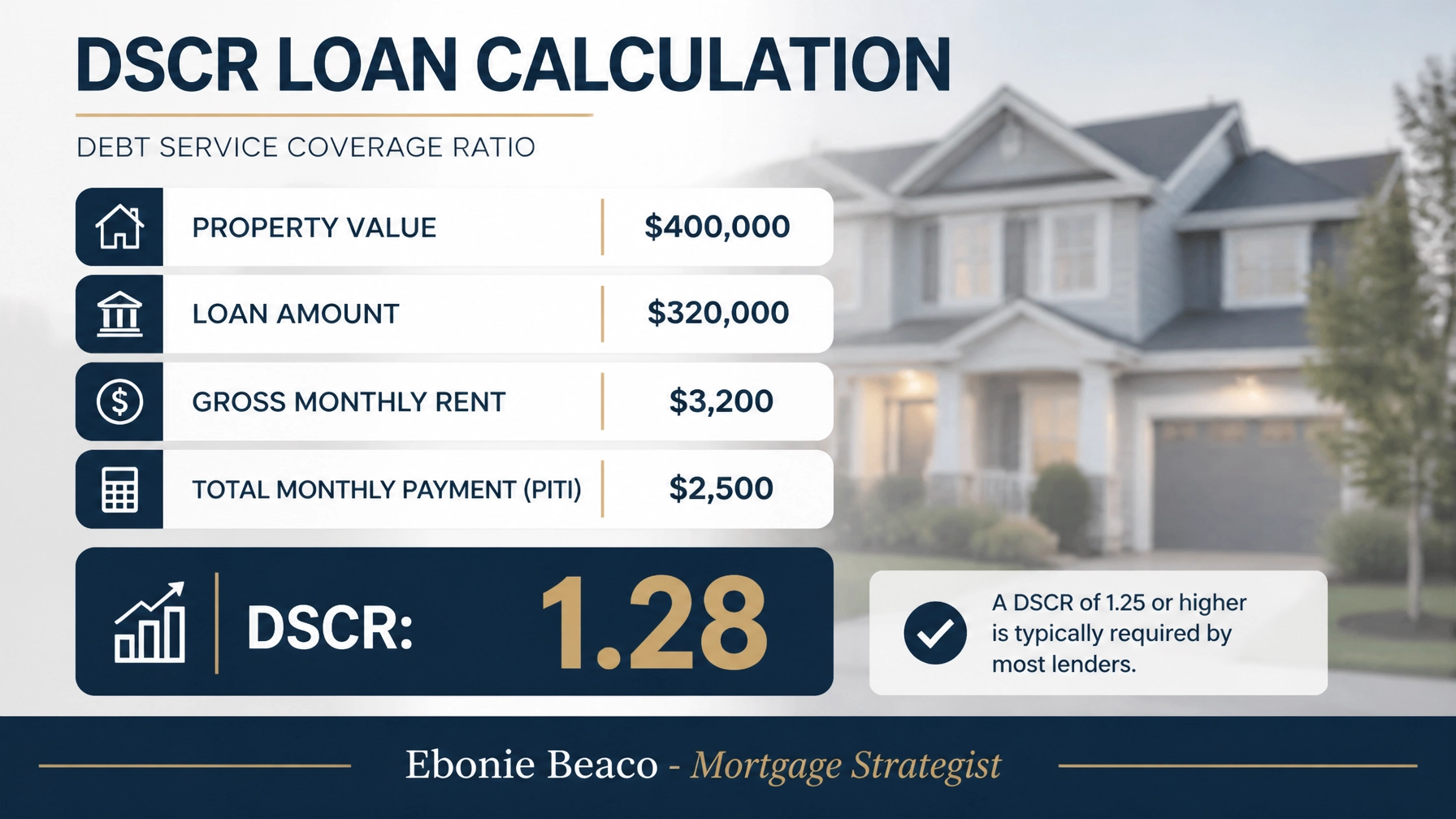

Real-World Financial Example: The DSCR Advantage

To understand how these numbers play out in a real transaction, let's look at a typical investment scenario in a market like Orlando or Indianapolis. Imagine an investor identifies a residential rental property with a purchase price of $400,000. Under current DSCR Investor Loan guidelines, the investor might opt for an 80% Loan-to-Value (LTV) mortgage, requiring a $320,000 loan amount. If the property generates $3,200 in gross monthly rent and the total monthly payment: including principal, interest, taxes, and insurance (PITI): is $2,500, the DSCR is 1.28.

A DSCR of 1.28 is considered strong, as most lenders look for a ratio of 1.20 or higher to qualify. This means the rental income covers the mortgage 1.28 times over, providing a healthy buffer for maintenance and vacancies. This calculation allows the investor to secure the property without relying on personal income documentation, making it a powerful tool for those with multiple properties or complex tax situations. You can use our mortgage calculators to run similar scenarios for your own prospective deals and see how a change in interest rate might affect your coverage ratio.

Protecting Your Equity with HELOC Loans

For homeowners in California or Illinois who are not looking to move but want to access their home's value, a HELOC (Home Equity Line of Credit) remains a strategic alternative to a full refinance. A HELOC allows you to keep your existing low-interest primary mortgage while tapping into a line of credit based on your increased home value. This is a popular choice for homeowners planning major renovations or those who want to have a "just in case" fund available for future investment opportunities. Accessing your equity this way ensures you don't lose a 3% or 4% rate on your main loan while still having the capital needed to grow your wealth.

The current rate shift is a reminder that the real estate market is always in motion, and success often depends on timing and the right financing structure. As we look toward June, the market will be closely watching the next round of consumer price index (CPI) data and Federal Reserve commentary. Staying informed through resources like the Home Loans Network FAQ and working with an experienced mortgage strategist can help you navigate these fluctuations with confidence. Whether you are a first-time buyer or a seasoned landlord, the right plan can turn market volatility into a strategic advantage.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664