Timing the Close: When Does the Wholesale Real Estate Assignment Fee Hit Your Account?

Getting a distressed property under contract is an exhilarating milestone for any real estate wholesaler working the markets in Chicago, Indianapolis, or Atlanta. You have spent hours driving for dollars, cold calling motivated sellers, and negotiating a price that leaves enough meat on the bone for an end buyer. Once that contract is signed and you have successfully assigned it to a cash buyer or an investor using DSCR investor loans, the focus shifts immediately to the payday. You want to know exactly when that assignment fee is going to land in your bank account so you can reinvest in your marketing or cover your business overhead. Understanding the mechanics of the closing table is essential to managing your cash flow and setting proper expectations for your growing wholesaling houses business.

Defining the Wholesale Assignment Fee

Assignment Fee: The profit or finders fee paid to a wholesaler for transferring their interest in a purchase agreement to an end buyer. Practical Application: This fee represents the spread between your contracted price with the seller and the final price paid by the investor who will actually close on the property.

In the world of wholesale real estate, the assignment fee is your primary source of revenue, but it is not always a simple one-step payment process. Typically, this fee is disbursed by the title company or the closing attorney once the entire transaction has been finalized and the deed has been recorded. You are not technically selling the house itself; rather, you are selling your "equitable interest" in the contract you have with the property owner. This distinction is critical for legal compliance in states like Illinois or Virginia, where regulations regarding unlicensed brokerage activity are strictly monitored. By staying focused on the contract assignment, you position yourself as a professional strategist who provides valuable off-market inventory to active property flippers and rental property owners.

The Standard Timeline for Getting Paid

For most wholesalers, the timeline from contract to cash usually spans between 30 and 45 days, depending on the complexity of the title work and the buyer's funding source. If your end buyer is using a cash-out refinance strategy or a fix and flip loan to acquire the property, the process might move at a different pace than an all-cash transaction. Most title companies require a clear title search, which can take anywhere from five to ten business days to complete in busy markets like Florida or California. Once the title is clear and the buyer's funds are in escrow, the closing is scheduled, and your fee is triggered. You should always maintain a close relationship with the escrow officer to ensure you are notified the moment the file is ready to fund.

The Two-Stage Payment Structure

A common strategy used by experienced wholesalers to secure their profit early is the two-stage payment method, which involves a non-refundable deposit from the end buyer. When you sign the assignment contract, you can request that a portion of your fee, perhaps $2,000 or $5,000, be paid immediately as a deposit to show the buyer’s commitment. This deposit is usually held in escrow by the title company and is applied toward your total assignment fee at the time of the final closing. If the buyer decides to walk away from the deal for a reason not covered by contingencies, you may be able to retain that deposit as liquidated damages. This structure provides a layer of financial security and ensures that you are compensated for the time the property was off the market.

Dealing with Single Disbursements at Closing

While some wholesalers prefer early deposits, many transactions are structured so the entire assignment fee is paid in one lump sum at the very end of the deal. In this scenario, the title company prepares a settlement statement, often called a HUD-1 or a Closing Disclosure, which clearly lists your assignment fee as a line item. Once the seller signs the deed and the buyer wires the purchase funds, the title company cuts you a check or initiates a wire transfer to your business account. This is the most transparent way to handle the transaction and is often preferred by title companies in states like Michigan and Georgia to ensure a clean audit trail. Waiting until the final closing ensures that all parties have fulfilled their contractual obligations before any profits are distributed.

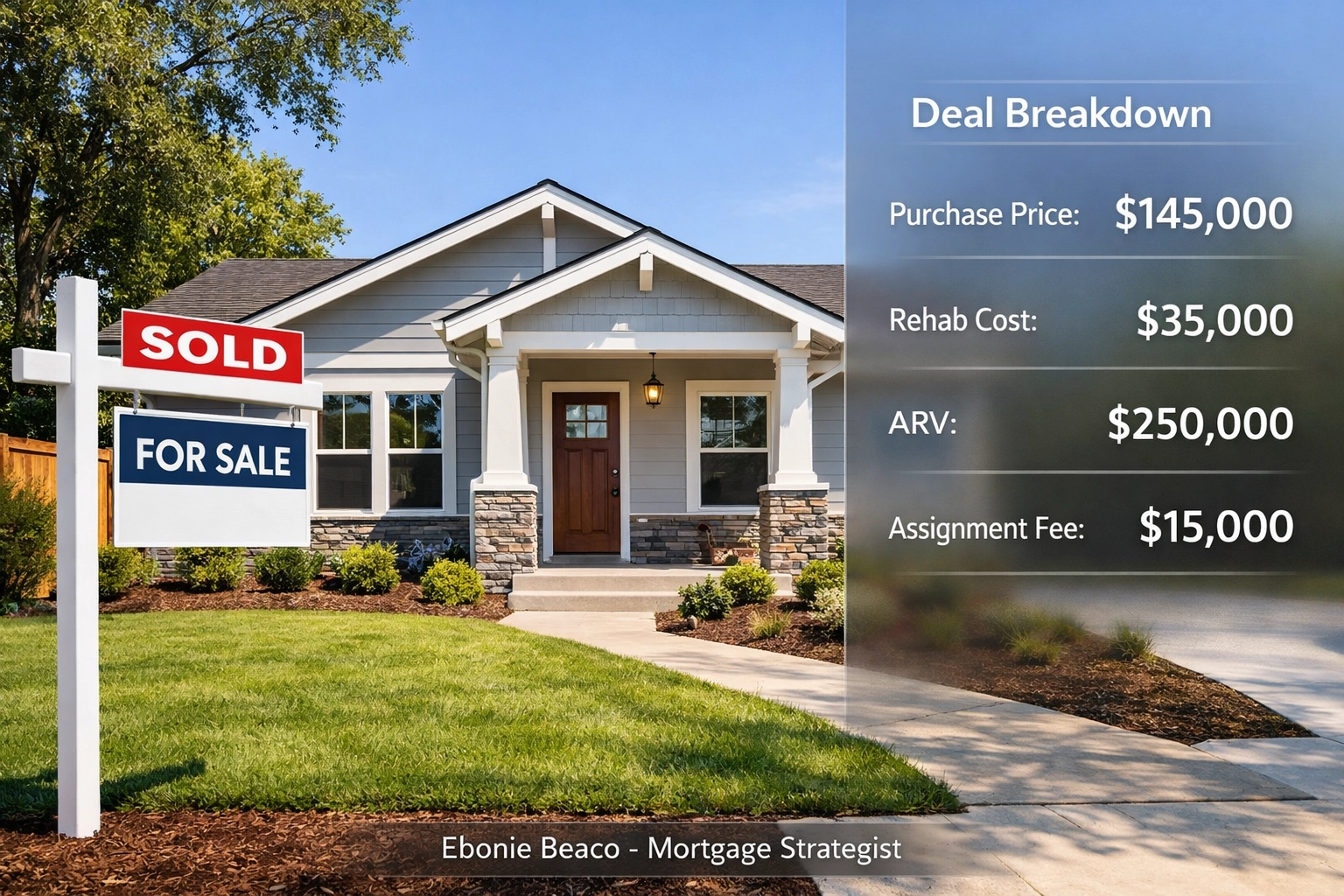

Real-World Example: Breaking Down the Numbers

To understand how the timing and the math work together, let’s look at a typical deal scenario for a single-family home in a suburban market.

Property Purchase Price (Contract with Seller): $145,000 Estimated Renovation Costs: $35,000 After Repair Value (ARV): $250,000 Wholesale Assignment Fee: $15,000 End Buyer Purchase Price: $160,000

In this example, the wholesaler finds a motivated seller in Arkansas and puts the house under contract for $145,000. They then find a fix-and-flip investor who agrees to take over the contract for $160,000, which includes the $15,000 assignment fee. The end buyer might put down a $3,000 non-refundable earnest money deposit (EMD) with the title company upon signing the assignment. At the final closing 30 days later, the title company will disburse the remaining $12,000 to the wholesaler.

Variables That Can Speed Up Your Payday

The speed at which you get paid is often determined by the quality of your end buyer and their choice of financing. If your buyer is working with a specialized lender for landlord loans or bridge financing, they may be able to close much faster than someone using a traditional bank. Working with a mortgage strategist like Ebonie Beaco can help you vet your buyers to ensure they have the "proof of funds" or pre-approval letters necessary to close the gap. A buyer who has a streamlined loan process reduces the risk of the deal falling through at the eleventh hour. When the buyer's financing is solid, the title company can move directly to the funding phase without unnecessary delays or extensions.

Exploring Assignment Fee Advances

Some wholesalers who need immediate capital to scale their operations look into assignment fee advance programs. These financial products allow you to receive a significant portion of your fee: typically 70% to 85%: within 24 to 48 hours of the end buyer depositing their earnest money. While this provides instant liquidity, it does come at a cost, as the service provider will charge a percentage or a flat fee for the convenience of the early payout. This can be a useful tool if you have multiple deals in the pipeline and need to fund a new direct mail campaign or pay for a large skip-tracing list. However, most professionals recommend building enough of a cash reserve so that you can wait for the full disbursement at the closing table without sacrificing a percentage of your profit.

The Role of the Title Company in Your Payout

The title company acts as the neutral third party that ensures everyone gets paid according to the contracts on file. They are responsible for collecting the buyer’s funds, paying off the seller’s existing mortgage, and cutting the checks for any commissions or assignment fees. It is vital to work with "investor-friendly" title companies in cities like Chicago or Richmond who understand the nuances of wholesaling houses and assignment contracts. Some traditional title companies may be confused by assignment fees if they do not regularly work with investors, which can lead to frustrating delays. Establishing a "go-to" escrow officer who knows your business model can drastically simplify the process of getting your funds released.

Navigating Double Closings for Larger Fees

If you are working on a deal with a very large assignment fee: say, $40,000 or more: you might consider a "double closing" instead of a standard assignment. In a double closing, you actually purchase the property from the seller in one transaction (the A-to-B deal) and then immediately sell it to your buyer in a second transaction (the B-to-C deal). This strategy keeps your profit hidden from both the seller and the buyer, which can be helpful if you are concerned about one of the parties feeling the fee is too high. Since there are two separate closings, you will often need "transactional funding" to cover the first purchase for a few hours. Once the second transaction closes, your profit is disbursed, usually on the same day or the following business morning.

Positioning Your Buyer for Success

Your payday is directly tied to your buyer's ability to cross the finish line, so helping them secure the right financing is a win-win strategy. Many investors who buy wholesale deals are looking to build long-term wealth through rental portfolios using DSCR investor loans. These loans focus on the property’s income potential rather than the borrower’s personal debt-to-income ratio, making them a favorite for scaling quickly. By connecting your buyers with a knowledgeable mortgage strategist, you ensure they have the tools to close the deal you just assigned to them. When your buyer wins, you get paid, and the entire ecosystem of real estate investing continues to thrive across the various markets you serve.

Final Steps Before the Check is Cut

As the closing date approaches, you should perform a final audit of your paperwork to ensure nothing is missing that could hold up your payment. Make sure the title company has a fully executed copy of both the original purchase agreement and the assignment of contract. Confirm that the buyer has wired their full closing costs and that any contingencies, such as inspection periods, have been officially waived. Double-check your wire instructions or verify the address where you want your check sent to avoid any last-minute confusion. Taking these proactive steps ensures that the transition from "deal under contract" to "funds in account" is as seamless and stress-free as possible.

📞 Work With Ebonie Beaco

If you are a wholesaler looking to:

- Close more deals

- Connect your buyers with financing

- Structure deals that actually get approved

- Learn how to grow into a real estate investor

I can help you every step of the way.

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork Website: HomeLoansNetwork.com Phone: 312-392-0664

👉 Whether you need lending, deal structuring, or mentorship, reach out today.