The Ultimate Mortgage Strategy Map: From Bourbon Street to the Windy City (2026 Edition)

Mortgages are not "one size fits all" in 2026. If you are looking at your home loan as a simple monthly bill, you are missing the biggest wealth-building opportunity in the modern economy. Financing is a strategic lever. It is the difference between owning one home and owning a ten-door portfolio.

Whether you are navigating the high-octane short-term rental market in Florida, the steady multi-unit yields in Chicago, the corporate growth of Atlanta, or the high-cash-flow potential of Louisiana, your success hinges on the debt you choose.

The Strategy Menu: Tools for Every Investor

The modern lending landscape offers specialized programs designed for specific financial profiles. To win in 2026, you need to know which tool to pull from the belt.

DSCR (Debt Service Coverage Ratio)

Definition: A mortgage program where qualification is based solely on the rental income generated by the subject property rather than the borrower's personal income or tax returns. Practical Application: Use this to scale your portfolio quickly without letting your personal Debt-to-Income (DTI) ratio slow you down.

Explore more about how we help investors scale at our Loan Programs page.

Non-QM and Bank Statement Loans

Definition: Loans that use alternative documentation, such as 12 to 24 months of bank deposits, to verify income for self-employed borrowers and entrepreneurs. Practical Application: If you are a business owner with heavy write-offs, this allows you to qualify based on your actual cash flow rather than your bottom-line tax number.

Fix-and-Flip and Bridge Loans

Definition: Short-term, interest-only financing designed for the rapid acquisition and renovation of distressed properties. Practical Application: These loans allow you to make "cash-like" offers on properties that would not qualify for traditional Conventional Loans, enabling you to renovate and refinance into long-term debt later.

HELOC vs. Cash-Out Refi: The "Second-Lien" Secret

Definition: A Home Equity Line of Credit (HELOC) is a revolving second mortgage, while a Cash-Out Refinance replaces your entire primary mortgage with a new, larger loan. Practical Application: In a 2026 market where many homeowners have existing 3% or 4% rates, a HELOC allows you to tap into equity without losing that low-interest primary rate.

State-by-State Comparison: Where the Money Moves

The geography of your investment dictates the complexity of your financing. Here is how the "big four" markets stack up this year.

Florida: The Airbnb and STR Capital

Florida remains the top destination for short-term rental (STR) operators. While insurance costs and property taxes have increased across the state, the migration of wealth into cities like Miami, Orlando, and Tampa keeps occupancy high.

- The Strategy: Use Florida rental property financing specifically tailored for STRs. Some lenders now allow us to use "AirDNA" projected data to qualify you for a DSCR loan before the property even has a booking history.

Atlanta: The Pivot to Buyer Leverage

Atlanta has transitioned from a frantic seller's market to a balanced hub for corporate relocations and film industry professionals. We are seeing a significant rise in "Assumable Mortgages," where buyers take over the seller's existing low-rate loan.

- The Strategy: If you cannot find an assumable deal, look for an Atlanta DSCR loan lender who understands the high-demand rental pockets in Midtown or the Perimeter. This allows you to build equity in a market with strong long-term appreciation prospects.

Chicago: The Multi-Unit Master

Chicago is the king of "house hacking." The city is filled with classic two-to-four-unit buildings. Investors here often use Chicago investment property loans to buy small multifamily properties, live in one unit, and let the other tenants pay the mortgage.

- The Strategy: Focus on properties near transit hubs or major universities. Chicago's price growth is stable, making it a "yield market" where cash flow is the primary driver of value.

Louisiana: The Cash-Flow Sleeper

Louisiana often flies under the radar, but for investors looking for low entry prices and high yields, it is a goldmine. While the appreciation might be slower than in the Sunbelt, the rental-to-price ratio in cities like Baton Rouge or parts of New Orleans is often superior.

- The Strategy: Be aggressive with your insurance underwriting. Use the high cash flow from these units to aggressively pay down high-interest debt or fund your next down payment.

Real-World Examples: The Math Behind the Moves

Numbers tell the story. Let’s look at how these strategies play out in real-world scenarios.

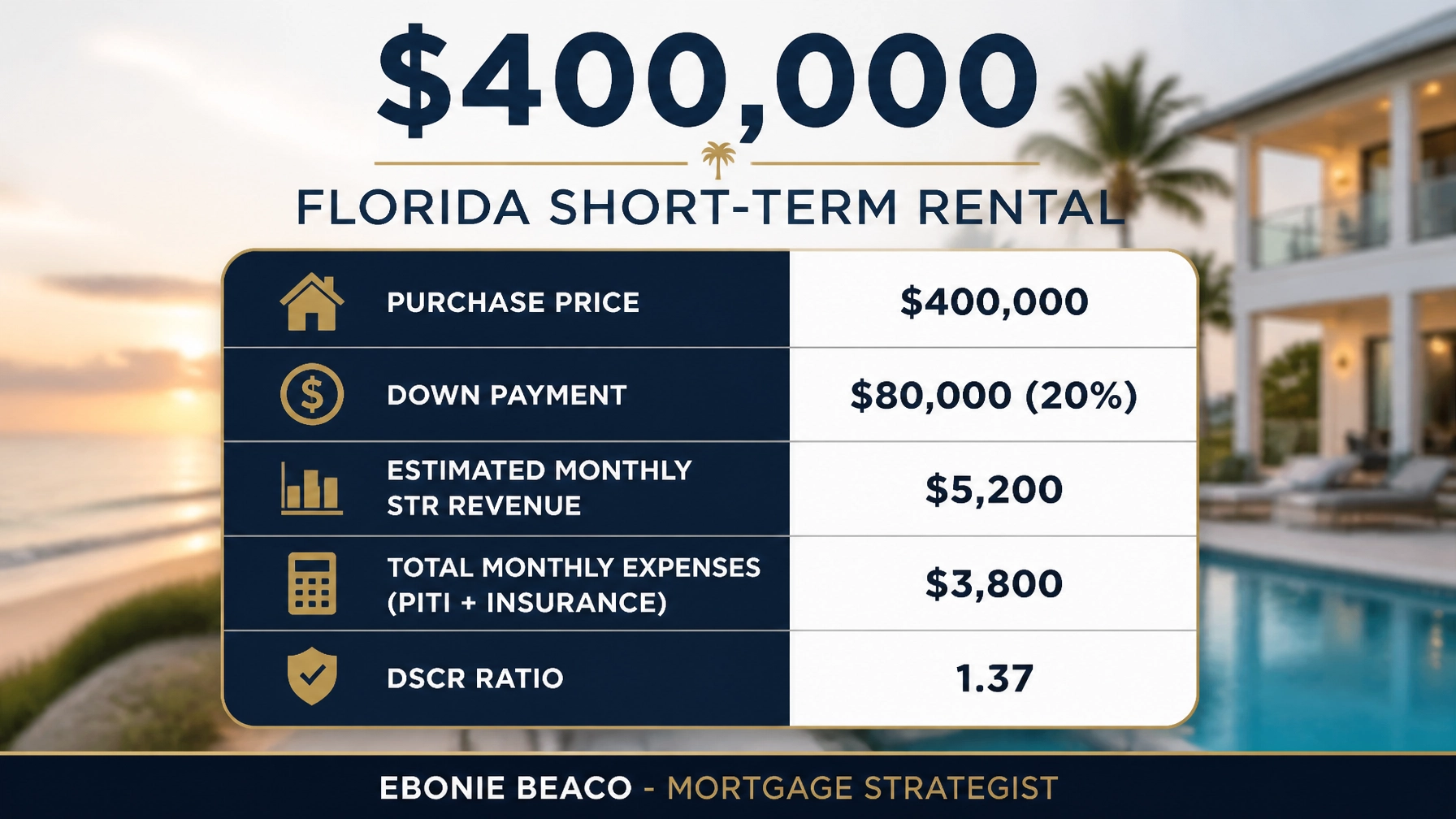

Scenario A: The Florida STR DSCR Play

Imagine you find a coastal condo in Florida for $400,000. You don't want to use your personal income to qualify because you just started a new business.

By using a DSCR loan, the property qualifies itself. With a 1.37 ratio, most lenders will jump at the chance to fund this deal. You keep your personal DTI clean, and the property pays for itself while building equity.

Scenario B: The Chicago 2-Unit Renovation

You find a distressed duplex in a transitioning Chicago neighborhood for $300,000. It needs work, but the After Repair Value (ARV) is high. You use fix and flip loans to cover the purchase and the rehab.

This strategy allows you to create value where it didn't exist. Once the renovation is complete, you can refinance into a long-term loan, pull your initial capital back out, and hold the property as a cash-flowing rental.

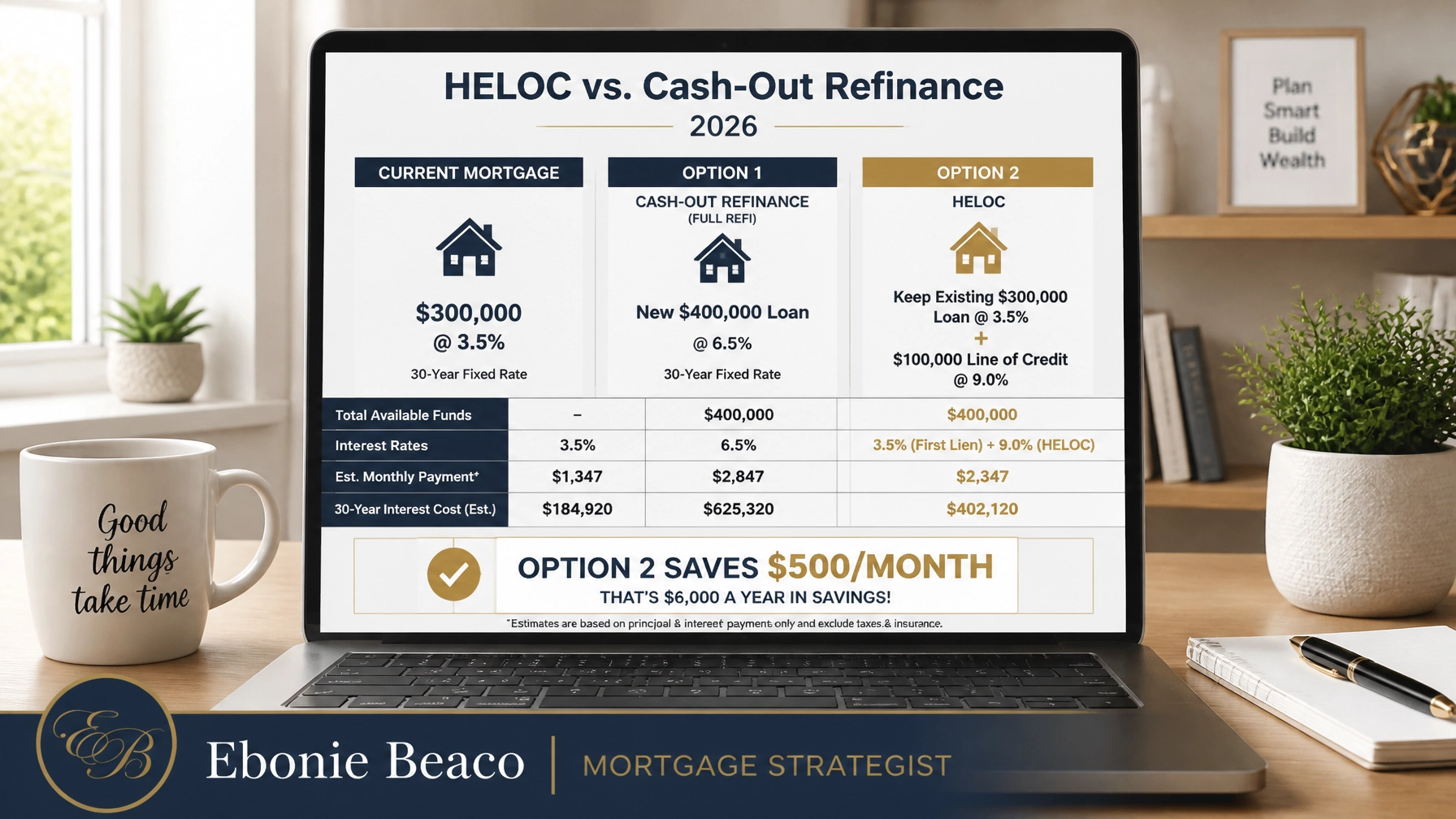

Scenario C: The Atlanta Equity Bridge

You own a primary residence in Atlanta valued at $600,000. Your current mortgage is only $300,000 at a 3.5% interest rate. You want to buy a rental property in Alabama, but you don't want to touch your savings.

Instead of a full cash-out refinance: which would raise the rate on your entire $300,000 balance: you take out a $100,000 HELOC. You keep your 3.5% rate on the first mortgage and only pay the higher rate on the money you actually use for the new down payment. This move saves you approximately $500 per month in interest costs compared to a full refinance.

Access Your Next Opportunity

The real estate market in 2026 requires more than just a "pre-approval." It requires a comprehensive financing roadmap. Whether you are buying your first home or your fiftieth unit, the way you structure your debt will dictate your long-term wealth.

Jump in and compare your options. Our team is ready to help you navigate the nuances of these different markets and programs. We provide the clarity you need to move forward with confidence.

Explore our Mortgage Calculators to see how these scenarios fit your specific goals.

Ready to build your roadmap?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664