The Ultimate Guide to Tonight’s Mortgage News: 5 Things Homebuyers and Realtors Need to Know Now

Navigating the real estate landscape requires more than just a keen eye for property; it demands a deep understanding of the financial mechanisms driving the market. As we step into June 2026, the mortgage industry continues to evolve with significant shifts in interest rates, inventory levels, and investor strategies. For homeowners, real estate investors, and realtors across states like Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia, staying informed is the primary way to maintain a competitive edge. This editorial guide explores the critical updates from tonight's mortgage news, providing the clarity you need to make informed decisions for your portfolio or your clients.

Explore the nuances of today's market conditions to see how they align with your long-term wealth-building goals. Whether you are looking at a single-family home in Chicago or a multi-unit investment in Florida, these five insights will help you steer through the complexities of modern real estate finance.

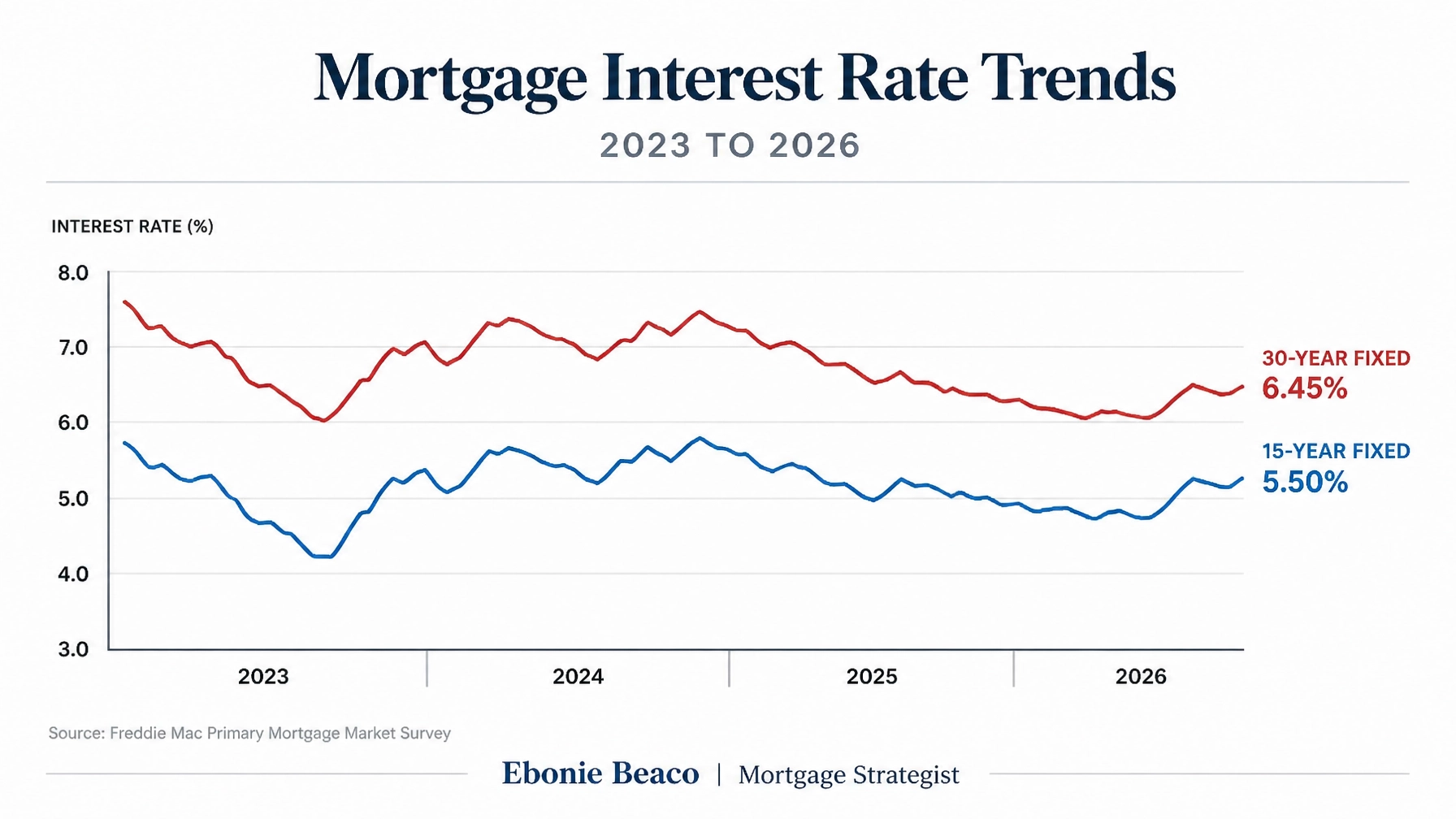

1. Mortgage Rates Stabilize in the Mid-6% Range

The most recent data indicates that the average 30-year fixed mortgage rate has found a new baseline in the mid-6% territory. This stabilization follows a period of significant volatility that defined the 2023 and 2024 housing cycles. Prime borrowers are currently seeing rates clustered between 6.3% and 6.7%, offering a predictable environment for those planning their next acquisition or refinance.

Jump in and compare these rates to the historical highs of previous years to understand the current value proposition. While we are far from the pandemic-era lows, the current downward drift toward the high-5% range is a welcome sign for many. According to Freddie Mac, this trend is largely supported by moderating inflation and steady bond yields. Realtors should note that this stability often leads to increased buyer confidence, as the fear of sudden, drastic rate hikes begins to fade from the headlines.

Accessing the right loan programs during this window is essential for maximizing your purchasing power. For investors, this rate environment makes the Debt Service Coverage Ratio (DSCR) calculation even more vital. When rates hold steady, it becomes easier to project long-term cash flow and evaluate whether a rental property meets your financial criteria.

2. Regional Market Divergence and Inventory Shifts

The national housing market is currently experiencing a significant regional divergence that homebuyers and realtors must recognize. In metropolitan areas like Chicago, inventory remains relatively tight, which helps maintain property values despite the broader economic shifts. Conversely, certain regions in Florida and California are seeing a more mixed performance, with some metros experiencing flat or slightly declining prices as affordability pressures reach a ceiling.

Realtors operating in these diverse markets must adapt their strategies based on local supply and demand. In states like Virginia and Georgia, the influx of new residents continues to support a robust market, even as overall transaction volumes remain lower than the decade average. This variation means that a "one size fits all" approach to real estate no longer works. You must analyze each market individually to identify where the best opportunities for growth reside.

For homeowners in Michigan or Missouri, this regional stability provides an excellent opportunity to evaluate home equity. Even if your local market isn't seeing the explosive growth of the past, your property remains a powerful financial tool. Understanding the mortgage basics of your local area is the first step toward leveraging that value for future investments or debt consolidation.

3. The Growing Dominance of DSCR and Landlord Loans

Real estate investors are increasingly turning to Non-QM solutions, particularly DSCR (Debt Service Coverage Ratio) loans, to scale their portfolios. These loans allow you to qualify based on the rental income of the property rather than your personal debt-to-income ratio. This is a game-changer for entrepreneurs and self-employed borrowers who may have complex tax returns but own high-performing rental assets.

DSCR Loan: A mortgage specifically for real estate investors that qualifies the borrower based on the property’s ability to cover its own debt payments with rental income.

This financing strategy is particularly effective for those managing Airbnb or short-term rental properties in vacation-heavy markets like Florida or the California coast. By focusing on the property's cash flow, investors can secure financing for multiple properties without hitting the traditional lending walls encountered with conventional loans.

If you are looking to acquire a multi-unit building or a fix-and-flip project, exploring DSCR investor loans can provide the flexibility needed to close deals quickly. This product aligns perfectly with the needs of professional landlords who prioritize asset performance over personal income documentation.

4. Tapping Into Home Equity: HELOC vs. Cash-Out Refinance

With home values remaining resilient across many states, homeowners are sitting on a record amount of equity. Tonight's news highlights a growing interest in utilizing this equity to fund everything from home renovations to the down payment on a second investment property. The choice between a Home Equity Line of Credit (HELOC) and a Cash-Out Refinance depends entirely on your current mortgage rate and your long-term goals.

HELOC: A revolving line of credit secured by your home equity that allows you to borrow as needed and pay back only what you use.

Cash-Out Refinance: The replacement of your existing mortgage with a new, larger loan, where the difference is paid out to you in cash.

For many who secured low rates in 2020 or 2021, a HELOC is often the preferred choice because it allows you to access funds without disturbing your existing first mortgage. However, if you are looking to consolidate high-interest debt or fund a major construction project, a home refinance might offer the structured payment schedule you need.

Realtors can add immense value by helping their clients understand these options. A client who feels "locked in" to their current home might realize they can actually use their equity to buy a larger home or start an investment portfolio. This knowledge transforms a simple transaction into a comprehensive wealth strategy.

5. Strategic Timing: The "Wait and See" Cost

One of the most profound takeaways from the current mortgage data is the cost of waiting for a significant drop in rates. While the trend is downward, many analysts, including those cited by the National Association of Realtors (NAR), suggest that any noticeable dip in rates will immediately unlock pent-up demand. This surge in buyer activity often leads to increased competition and higher home prices, effectively negating any savings from a lower interest rate.

For buyers in competitive markets like Chicago or Northern Virginia, the "buy now and refinance later" strategy remains a dominant theme. By securing a property today, you avoid the bidding wars that are likely to return if rates hit the 5% mark. You can then look at a rate-term refinance once market conditions shift in your favor.

Explore the current mortgage calculators to run these scenarios for yourself. Seeing the numbers on paper often provides the confidence needed to move forward in a market that feels uncertain. Remember, the goal is not to time the market perfectly but to make a strategic move that aligns with your financial timeline.

Practical Financial Example: Unlocking Equity with a HELOC

To understand how these strategies work in a real-world scenario, let's look at a homeowner in a mid-sized city in Georgia. This example demonstrates how a strategic mortgage move can provide the capital needed for future growth.

Imagine you own a home valued at $450,000 with a current mortgage balance of $250,000. Many lenders will allow you to access a total loan-to-value (LTV) of up to 85% across your first mortgage and your equity line.

The Calculation:

- Current Property Value: $450,000

- Max LTV (85%): $382,500

- Minus Current Mortgage: $250,000

- Available Equity for HELOC: $132,500

With $132,500 in available funds, this homeowner could easily fund a major renovation to increase the property value further or use the funds as a down payment on a new rental property. This approach allows you to build wealth using the assets you already own, without needing to save up a massive cash reserve.

Conclusion: Lead with Strategy

The mortgage market in June 2026 is full of nuance, but for the informed homebuyer, investor, or realtor, it is also full of opportunity. By focusing on rate stabilization, regional trends, and the power of home equity, you can navigate these waters with professional confidence. Whether you are managing a single property or a growing portfolio, the right financing strategy is the foundation of your success.

The key to succeeding in today's environment is proactive education. Stay close to the data, understand the products available in your specific state, and always align your financing with your ultimate wealth goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664