The Ultimate Guide to Today’s Rate Volatility: Everything Alabama and Indiana Investors Need to Succeed

Navigating the mortgage landscape in June 2026 requires a shift in perspective for real estate investors and homeowners alike.

While the extreme fluctuations of the early 2020s have subsided, current interest rates remain in a stable yet elevated range between 6.4% and 6.6%.

For those active in the Alabama and Indiana markets, this stability provides a unique window to plan long-term wealth strategies without the fear of sudden, massive shifts in borrowing costs.

Understanding how to leverage these conditions is essential for scaling your real estate portfolio or maximizing your primary residence's potential.

Defining the Current Landscape

Before diving into specific regional strategies, it is helpful to establish a clear understanding of the technical terms shaping today’s financial decisions.

Rate Volatility: The frequency and magnitude of changes in interest rates over a specific period.

In the current market, volatility has decreased, meaning daily rate moves are smaller and more predictable than in previous years.

Basis Point (BPS): A unit of measure equal to one one-hundredth of one percent (0.01%).

A move of 50 basis points represents a half-percentage point change in your mortgage rate.

Debt Service Coverage Ratio (DSCR): A measurement of a property's ability to cover its debt obligations through its own generated income.

Investors use this metric to qualify for DSCR investor loans without relying on personal income or employment history.

Loan-to-Value (LTV): The ratio of the loan amount divided by the appraised value of the property.

LTV determines the amount of equity you must maintain and influences the terms of your financing.

The State of Play: June 2026

As of early June 2026, the 30-year fixed conforming mortgage rate is averaging approximately 6.5%.

According to recent updates from The Mortgage Reports, the trading range for the year has remained significantly tighter than in previous cycles.

This decrease in volatility allows you to underwrite deals with a higher degree of confidence.

You no longer have to worry about a rate jumping a full point between the time you find a property and the time you close the loan.

For investors in states like Alabama, Indiana, and Michigan, this predictability is a welcome change that simplifies the acquisition process.

Alabama Market Focus: Cash Flow in Birmingham and Huntsville

Alabama continues to be a cornerstone for cash-flow-heavy investment strategies due to its favorable price-to-rent ratios.

In cities like Birmingham and Huntsville, the demand for workforce housing remains strong, even as national home price appreciation slows.

Alabama investors are increasingly looking toward landlord financing and DSCR-based products to bypass the complexities of traditional W-2 verification.

The focus here is on immediate yield rather than speculative growth.

Case Study: Birmingham DSCR Rental Strategy

Imagine you are looking at a single-family home in a stable Birmingham neighborhood.

If the monthly market rent is $2,200 and your total monthly mortgage payment (including taxes, insurance, and fees) is $1,750, your DSCR is 1.25.

Lenders typically look for a DSCR of 1.20 or higher to offer the most competitive terms on rental property loans.

This approach ensures the property is self-sustaining and provides a buffer for maintenance and vacancies.

Indiana Market Focus: Stability in Indianapolis and Fort Wayne

Indiana offers a similar profile of stability, often characterized by moderate appreciation and steady tenant demand.

Indianapolis, in particular, has seen a rise in sophisticated investors using bridge loans and fix-and-flip financing to revitalize aging housing stock.

Because Indiana’s entry prices are lower than national averages, the impact of a 6.5% interest rate is less restrictive on monthly cash flow than in high-cost states like California or Virginia.

Indiana homeowners are also sitting on significant amounts of home equity that can be tapped for further investment.

Unlocking Home Equity with HELOCs

A Home Equity Line of Credit (HELOC) remains one of the most versatile tools for homeowners looking to build wealth.

A HELOC allows you to access the value built up in your home to use as a down payment on a second property or to fund renovations that increase your primary home's value.

Explore how your equity can work for you by visiting our mortgage calculators to run your own scenarios.

Accessing this capital is often faster and more flexible than a full cash-out refinance, especially if your current first mortgage has a rate significantly lower than today’s market average.

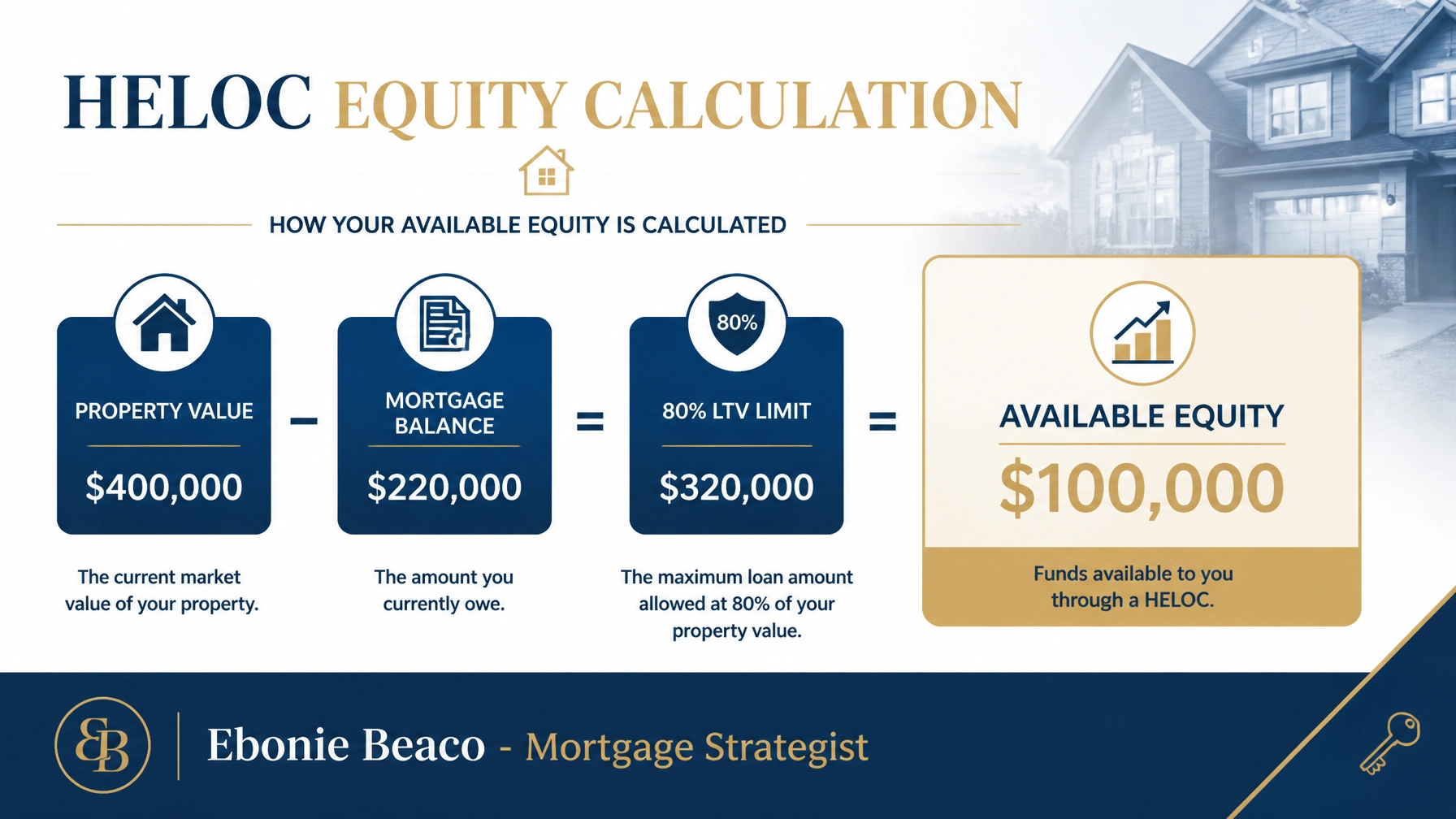

Calculating Your Available Equity in Indiana

Consider an Indianapolis homeowner with a property valued at $400,000 and an existing mortgage balance of $220,000.

If a lender allows for a combined loan-to-value (CLTV) of 80%, the total allowable debt on the property is $320,000.

Subtracting the existing $220,000 mortgage leaves $100,000 in available equity for a HELOC.

This $100,000 could serve as the cash needed to purchase two additional rental properties with 20% down payments in more affordable markets.

Navigating Volatility with Non-QM Loans

For self-employed borrowers and entrepreneurs in states like Florida, Georgia, and Illinois, standard loan products may not always fit their unique financial profiles.

Non-QM (Non-Qualified Mortgage) loans, such as bank statement loans, provide an alternative path to homeownership.

These programs allow you to qualify based on the cash flow of your business or personal bank deposits rather than tax returns.

This flexibility is vital in a rate environment where traditional debt-to-income (DTI) requirements can become a hurdle.

Jump in and compare these options with a strategist who understands the nuances of the self-employed lifestyle.

Strategic Tips for Today's Market

While you cannot control the Federal Reserve’s decisions, you can control your strategy and how you respond to market shifts.

- Prioritize Cash Flow: Ensure every investment deal pencils out at current rates. Do not rely on future rate cuts to make a deal work.

- Lock in Predictability: Fixed-rate loans provide peace of mind in a "higher-for-longer" environment.

- Use Equity Wisely: Whether through a cash-out refinance or a HELOC, your home equity is a powerful tool for portfolio expansion.

- Partner with Experts: Work with a mortgage strategist who has experience in multiple states and understands the regional differences between markets like Alabama, Arkansas, and Kentucky.

According to research from NerdWallet, timing the market is less effective than time in the market.

Staying informed and moving forward with a clear, data-driven plan is the most reliable way to achieve your long-term financial goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664