The Ultimate Guide to Today’s Housing Market: Everything You Need to Succeed in June

Navigating the housing market in June 2026 requires a sharp eye for detail and a solid understanding of current economic shifts. As we move deeper into the summer season, the landscape for buyers, sellers, and investors is defined by a stabilized but elevated interest rate environment. With the 30-year fixed mortgage rate currently hovering between 6.4% and 6.6%, the frenetic pace of previous years has transitioned into a more deliberate and strategic marketplace. Whether you are looking to acquire your first property, refinance an existing asset, or scale a multi-state investment portfolio, understanding these dynamics is the first step toward achieving your financial goals.

The current climate is influenced significantly by broader economic factors, including persistent inflation and geopolitical tensions that have kept upward pressure on Treasury yields. While many hoped for a sharp decline in rates by mid-year, the market has instead settled into a "higher for longer" pattern that rewards those who prioritize long-term equity over short-term speculation. This shift has created unique pockets of opportunity across the states we serve, from the high-value coastal markets of California to the steady, affordable suburbs of Michigan and Indiana. By staying informed on regional trends and specialized financing tools, you can position yourself to act with confidence in this evolving June market.

Current Mortgage Rate Trends: What You Need to Know

Understanding the cost of capital is essential for any real estate transaction, and the current June 2026 averages provide a clear baseline for your planning. According to Freddie Mac, the 30-year fixed-rate mortgage has remained relatively flat, showing only minor fluctuations based on weekly economic data releases. As of early June, top-tier borrowers are seeing conforming 30-year rates near 6.53%, while 15-year fixed options are providing a slight reprieve, typically landing between 5.8% and 5.9%.

These rates reflect a market that has largely priced in the Federal Reserve's current stance on holding policy rates steady through the summer. For you, this means the era of extreme rate volatility has likely paused, allowing for more predictable monthly payment projections. While government-backed options like FHA and VA loans continue to offer competitive pricing: often in the low 6% range: conventional financing remains the primary vehicle for many move-up buyers and investors. Exploring conventional loan programs can help you determine how these national averages apply to your specific credit profile and down payment capacity.

Regional Market Snapshots: From California to Virginia

The national narrative of a "slowing market" often hides the distinct realities found at the state and local levels. In high-cost states like California and parts of Virginia, the impact of 6.5% interest rates is most visible in extended days-on-market and a higher frequency of price adjustments. Buyers in these regions now have more leverage to negotiate for seller concessions, such as temporary rate buydowns or closing cost credits, which were nearly non-existent two years ago.

Conversely, the Midwest and parts of the South continue to display remarkable resilience due to their inherent affordability. States like Indiana, Michigan, Missouri, and Kentucky are seeing steady, albeit slower, price appreciation as buyers from higher-cost regions seek value. In Georgia and Florida, the market remains active but more balanced, with inventory levels finally catching up to demand in several major metropolitan areas. For a detailed look at specific local dynamics, you can access our Chicago neighborhoods market reports or contact us for insights on other service areas like Alabama and Arkansas.

Leveraging DSCR Loans for Real Estate Investment

For real estate investors, the Debt Service Coverage Ratio (DSCR) loan has become a vital tool in a mid-6% rate environment. These loans are specifically designed for landlords and portfolio builders because they qualify the property based on its rental income rather than the borrower’s personal income or debt-to-income ratio. This is particularly beneficial for self-employed investors or those who have reached the limit of conventional financing.

Consider an investor looking at a single-family rental in a market like Atlanta or Indianapolis. If the property has a purchase price of $450,000 and generates $3,200 in gross monthly rent, a DSCR calculation would look like this:

- Purchase Price: $450,000

- Gross Monthly Rent: $3,200

- Monthly PITI (Principal, Interest, Taxes, Insurance): $2,500

- DSCR Ratio: 1.28 ($3,200 / $2,500)

A DSCR ratio of 1.28 is typically considered strong by most lenders, as it shows the property generates 28% more income than the cost of the mortgage. This allows you to scale your portfolio more rapidly, as the qualification focus remains on the asset’s performance. You can explore more about these and other investor loan programs to see if they align with your acquisition strategy this June.

Unlocking Home Equity: Refinance and HELOC Strategies

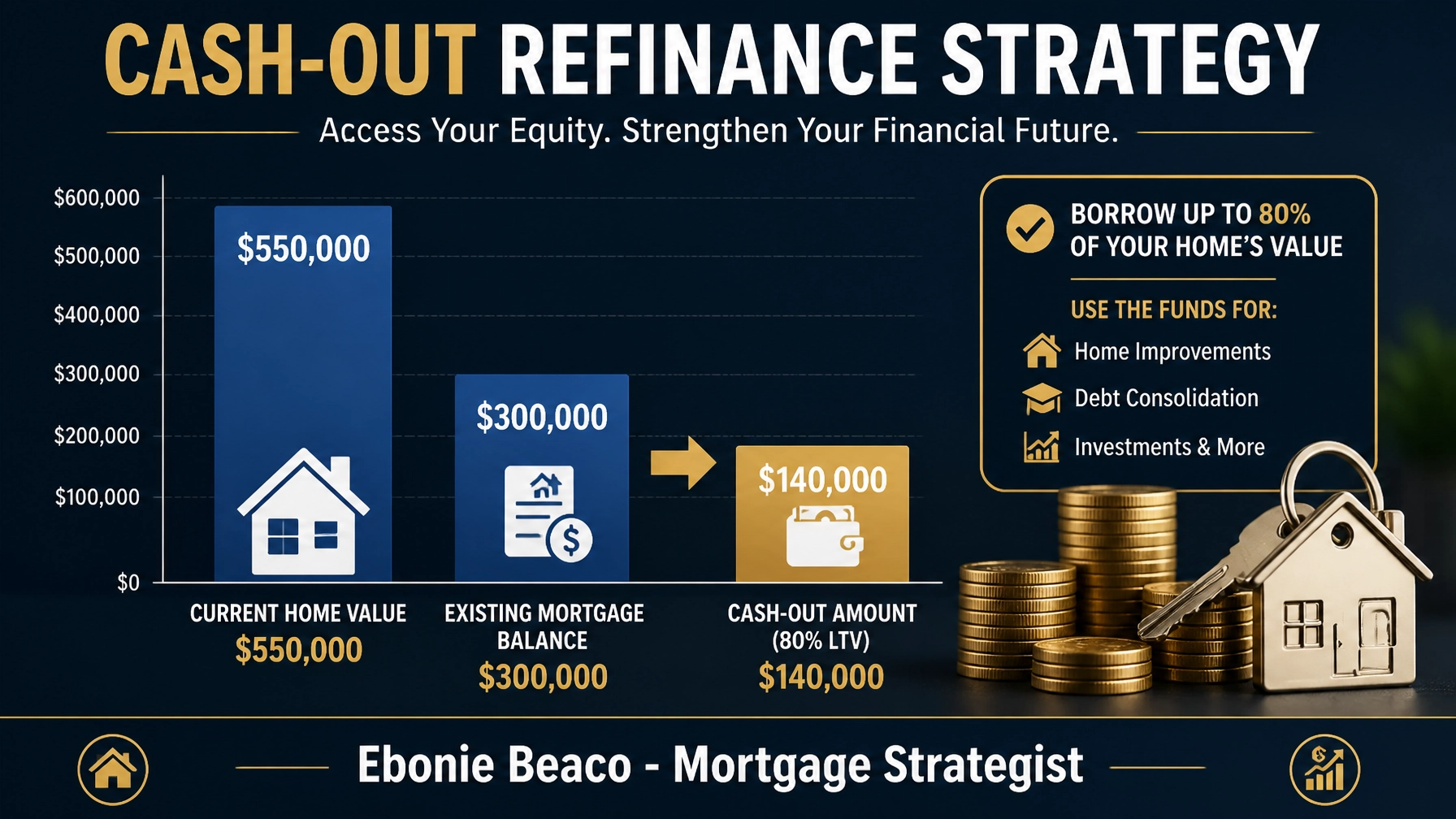

Many homeowners in states like Illinois, Michigan, and Florida have seen substantial equity growth over the last several years. Even as national price growth slows to a modest 0.7% annually, the "equity cushion" remains a powerful financial asset. A cash-out refinance or a Home Equity Line of Credit (HELOC) can provide the necessary capital for property renovations, debt consolidation, or the down payment on a new investment property.

Let's examine how a strategic cash-out refinance can fuel your next move. Suppose you own a home currently valued at $550,000 with an existing mortgage balance of $300,000. By utilizing a cash-out refinance at an 80% Loan-to-Value (LTV) ratio, you could potentially access significant funds:

- Current Home Value: $550,000

- Max Loan Amount (80% LTV): $440,000

- Existing Balance: $300,000

- Available Cash-Out: $140,000 (minus closing costs)

This $140,000 can be deployed as a down payment for a duplex or a fix-and-flip project, effectively turning your primary residence into a wealth-building engine. While home refinance activity is lower than historical norms, it remains a highly effective strategy for those with a clear plan for the extracted capital.

Strategies for First-Time Buyers in a Changing Market

If you are entering the market as a first-time homebuyer this June, the current slowdown is actually your ally. The reduction in bidding wars means you have the time to perform thorough due diligence and utilize mortgage calculators to ensure your monthly payment fits your budget. In states like Alabama and Missouri, where entry-level pricing is more accessible, many buyers are finding success by focusing on properties that need cosmetic updates.

Jump in by researching down payment assistance programs or low-down-payment options like FHA or VA loans. These programs often provide more flexible credit requirements, which is essential if you are still building your financial profile. Remember that a 6.5% interest rate does not have to be permanent; many buyers are choosing to "marry the house and date the rate," with the intention of refinancing if rates dip in the future. Comparing loan programs now will give you the clarity needed to make a strong offer when you find the right home.

Final Thoughts for the June Market

The June 2026 housing market is one of stabilization and strategic planning. While the days of 3% interest rates are in the rearview mirror, the current environment offers a level of transparency and predictability that was missing during the recent "boom" years. Whether you are navigating the high-stakes markets of California or the affordable neighborhoods of the Midwest, success comes down to having the right financing strategy in place.

Access professional guidance to explore how these national trends affect your local options. By aligning your mortgage solution with your long-term wealth goals, you can navigate the complexities of today's market with confidence and precision.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664