The Ultimate Guide to Reverse Mortgages: Everything You Need to Succeed with Your Equity

For many homeowners in cities like Chicago, Atlanta, or Los Angeles, the home is more than just a place to live. It is the largest asset they own. As you enter your retirement years, that equity can serve as a powerful financial tool. A reverse mortgage allows you to tap into that value without the burden of a monthly mortgage payment.

Explore the mechanics of these loans and how they function as a strategic wealth management tool for seniors. Whether you are a homeowner in Georgia looking to supplement your income or an investor helping a family member in Florida, understanding these rules is the first step toward financial flexibility.

Defining the Reverse Mortgage

Reverse Mortgage: A specialized loan for older homeowners that converts a portion of home equity into cash while allowing the borrower to remain in the residence.

Equity: The difference between the current market value of your home and the amount you owe on any existing mortgage.

Unlike a traditional "forward" mortgage where you make monthly payments to a lender, the lender makes payments to you. The loan is typically repaid only when the last surviving borrower moves out, sells the house, or passes away.

Age Requirements: Who Qualifies?

Eligibility is primarily driven by age and the amount of equity held in the property. There are two main paths based on age and the type of loan you select.

The 62+ Rule for HECM

The most common type of reverse mortgage is the Home Equity Conversion Mortgage (HECM). This program is regulated and insured by the Federal Housing Administration (FHA). To qualify for a HECM, at least one borrower must be 62 years of age or older.

The 55+ Rule for Proprietary Loans

For those who have high value homes or are slightly younger, Proprietary Reverse Mortgages (also known as Jumbo Reverse Mortgages) are available. In many states, including California and Virginia, these private loans allow borrowers to start as young as 55 years old.

Explore our mortgage basics glossary to understand more about these terms.

HECM vs. Proprietary Loans: Comparing the Options

Jump in and compare the two primary vehicles for accessing equity. While both offer no monthly payments, they serve different financial profiles.

HECM (Home Equity Conversion Mortgage)

- Insured by: Federal Housing Administration (FHA).

- Lending Limits: Subject to FHA nationwide limits (currently $1,149,825 for 2024).

- Counseling: Requires a session with a HUD-approved counselor.

- Usage: Funds can be used for any purpose, including paying off an existing mortgage.

Proprietary (Jumbo) Reverse Mortgage

- Insured by: Private lenders (not government insured).

- Lending Limits: Designed for "Jumbo" properties valued up to $4 million or more.

- Counseling: Often requires counseling, though rules vary by state.

- No Mortgage Insurance Premium: Typically does not require the upfront and annual mortgage insurance premiums found with HECMs.

Understanding the Math: The Principal Limit

Accessing your equity requires a clear understanding of how much cash you can actually receive. This is determined by the Principal Limit.

Principal Limit: The maximum amount of money a borrower can receive from a reverse mortgage.

The Principal Limit Factor (PLF)

Lenders use a calculation involving the age of the youngest borrower, the current interest rate, and the appraised value of the home. The resulting percentage is called the Principal Limit Factor (PLF).

Generally, the older you are and the lower the interest rate, the higher your PLF will be.

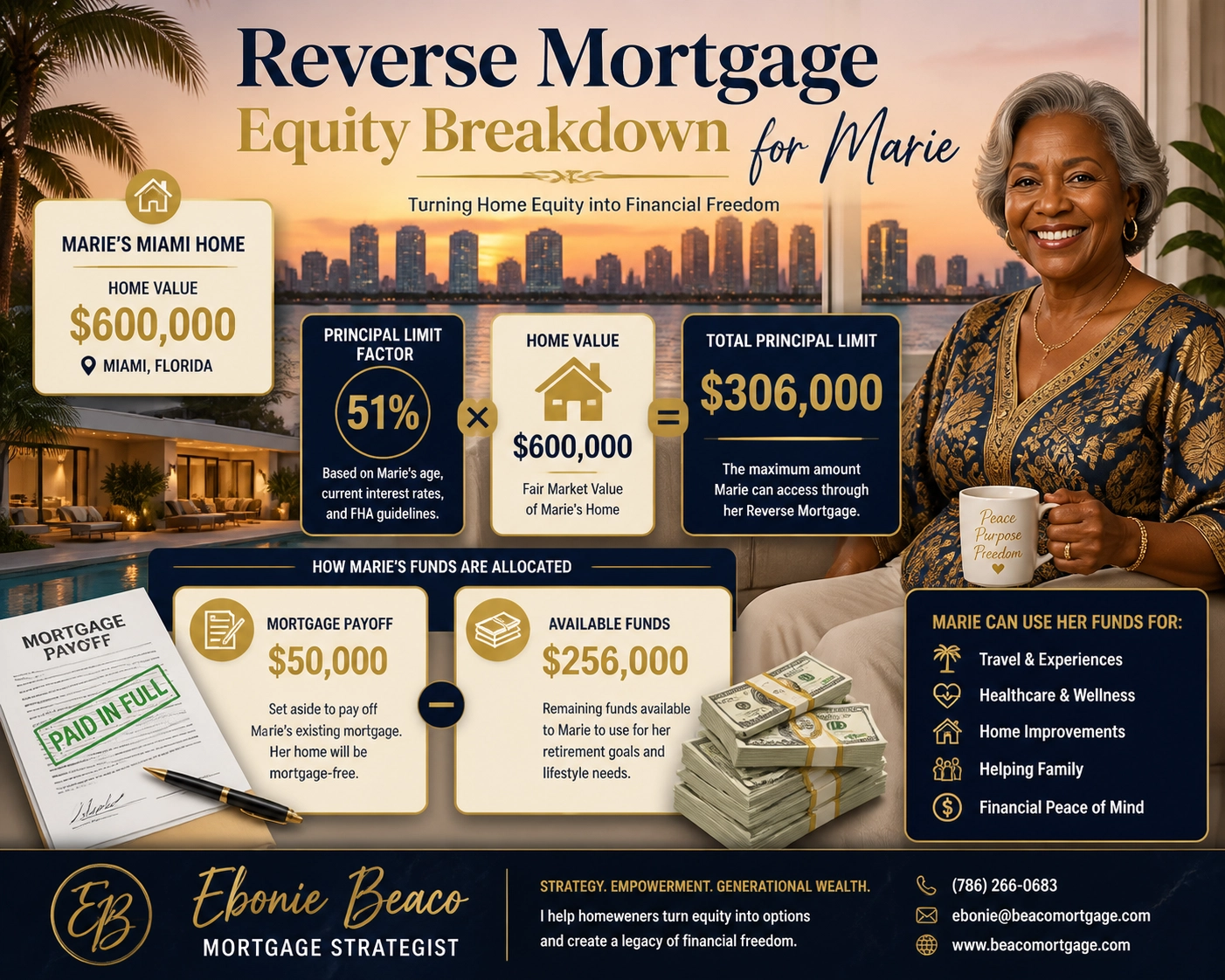

A Sample Equity Calculation

Imagine a homeowner in Miami, Florida, with the following profile:

- Home Value: $600,000

- Existing Mortgage: $50,000

- Age: 72

- Assumed PLF: 0.45 (45%)

Step 1: Multiply the Home Value by the PLF.

$600,000 x 0.45 = $270,000 (Gross Principal Limit)

Step 2: Subtract the existing mortgage and closing costs.

$270,000 - $50,000 (Mortgage) - $15,000 (Estimated Closing Costs) = $205,000 (Net Available Funds)

The borrower can take this $205,000 as a lump sum, a monthly payment, or a line of credit that grows over time.

https://cdn.marblism.com/1LSjKKTAZun.webp

{kind=link}

Case Study: Strategic Equity Access in California

Consider the scenario of Mr. Chen, a 74-year-old Chinese-American homeowner living in the San Francisco Bay Area.

Mr. Chen owns a home worth $1,500,000. He paid off his mortgage years ago, but his property taxes and insurance in California have continued to rise. He wants to supplement his retirement income without moving out of the neighborhood he loves.

The Strategy: Proprietary Jumbo Loan

Because his home value exceeds the FHA HECM limit, Mr. Chen chooses a Proprietary Reverse Mortgage.

- Home Value: $1,500,000

- Age: 74

- Principal Limit Factor: 0.40

- Total Available Equity: $600,000

Mr. Chen decides to take $100,000 upfront to handle immediate home repairs and places the remaining $500,000 into a line of credit. This provides him with a "rainy day" fund that allows him to remain in his home comfortably while maintaining his lifestyle.

Important Borrower Obligations

Even though you are not making a monthly mortgage payment, you still have responsibilities as a homeowner. Failure to meet these requirements can lead to the loan becoming due and payable.

Primary Residence: You must live in the home as your main residence. If you move out for more than 12 consecutive months (for example, to an assisted living facility), the loan balance is usually due.

Property Taxes: You are responsible for staying current on all property taxes.

Homeowners Insurance: You must maintain adequate insurance coverage on the property.

Maintenance: The home must be kept in good repair. Lenders may perform periodic inspections to ensure the asset is being preserved.

If you are concerned about your credit history affecting these obligations, you can review our guide on understanding credit.

How You Receive Your Money

One of the most flexible aspects of a reverse mortgage is the payout structure. You can customize how you receive your funds to fit your specific financial goals.

- Lump Sum: Receive all your available funds at once at closing (typically restricted to a fixed-rate loan).

- Tenure: Equal monthly payments as long as at least one borrower lives in the home.

- Term: Equal monthly payments for a fixed period of time.

- Line of Credit: Access funds as you need them. The unused portion of the line of credit often grows over time, giving you access to more capital in the future.

- Modified Tenure/Term: A combination of a line of credit and monthly payments.

Is a Reverse Mortgage Right for You?

Deciding to use your home equity is a significant financial move. It is often a great fit for homeowners in markets like Chicago or Virginia who plan to stay in their homes for a long time and want to eliminate their monthly mortgage payment.

However, you should consider the impact on your heirs. Since the loan balance grows over time as interest and fees are added, the amount of equity left for your estate will decrease. Most reverse mortgages are "non-recourse" loans, meaning you or your heirs will never owe more than the home is worth at the time of sale, even if the loan balance exceeds the home's value.

Access our mortgage calculators to run different scenarios based on your current home value and age.

Take the Next Step with Your Equity

Understanding the math and the rules of reverse mortgages helps you navigate your retirement with confidence. Whether you are looking at a HECM in Michigan or a Proprietary Jumbo loan in California, Home Loans Network is here to guide you through the process.

Position your equity to work for you. If you have questions about Principal Limit Factors or want to see how these numbers look for your specific property, connect with a specialist today.

https://cdn.marblism.com/GcSUXf3h-Fz.webp

{kind=link}

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664