The Ultimate Guide to June 8th’s Housing News: Everything You Need to Succeed

The housing market landscape on June 8, 2026, presents a complex yet opportunistic environment for homeowners, real estate investors, and industry professionals. Current data indicates that mortgage rates are maintaining a steady position in the mid-6% range, following a period of significant volatility driven by global economic shifts and domestic inflation. For buyers and refinancers across Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia, understanding these nuances is essential for making informed financial decisions. This guide explores the latest trends in interest rates, inventory levels, and regional market shifts to help you navigate your next transaction with confidence.

Explore the current state of the market to identify where the best opportunities for growth and equity extraction currently reside. Accessing timely information allows you to pivot your strategy as the economic backdrop evolves, particularly as inflation figures and geopolitical tensions influence the Federal Reserve’s upcoming policy decisions. Jump in as we dissect the metrics defining early June 2026 and provide the technical insights required to scale your real estate portfolio.

Understanding the Current Mortgage Rate Environment

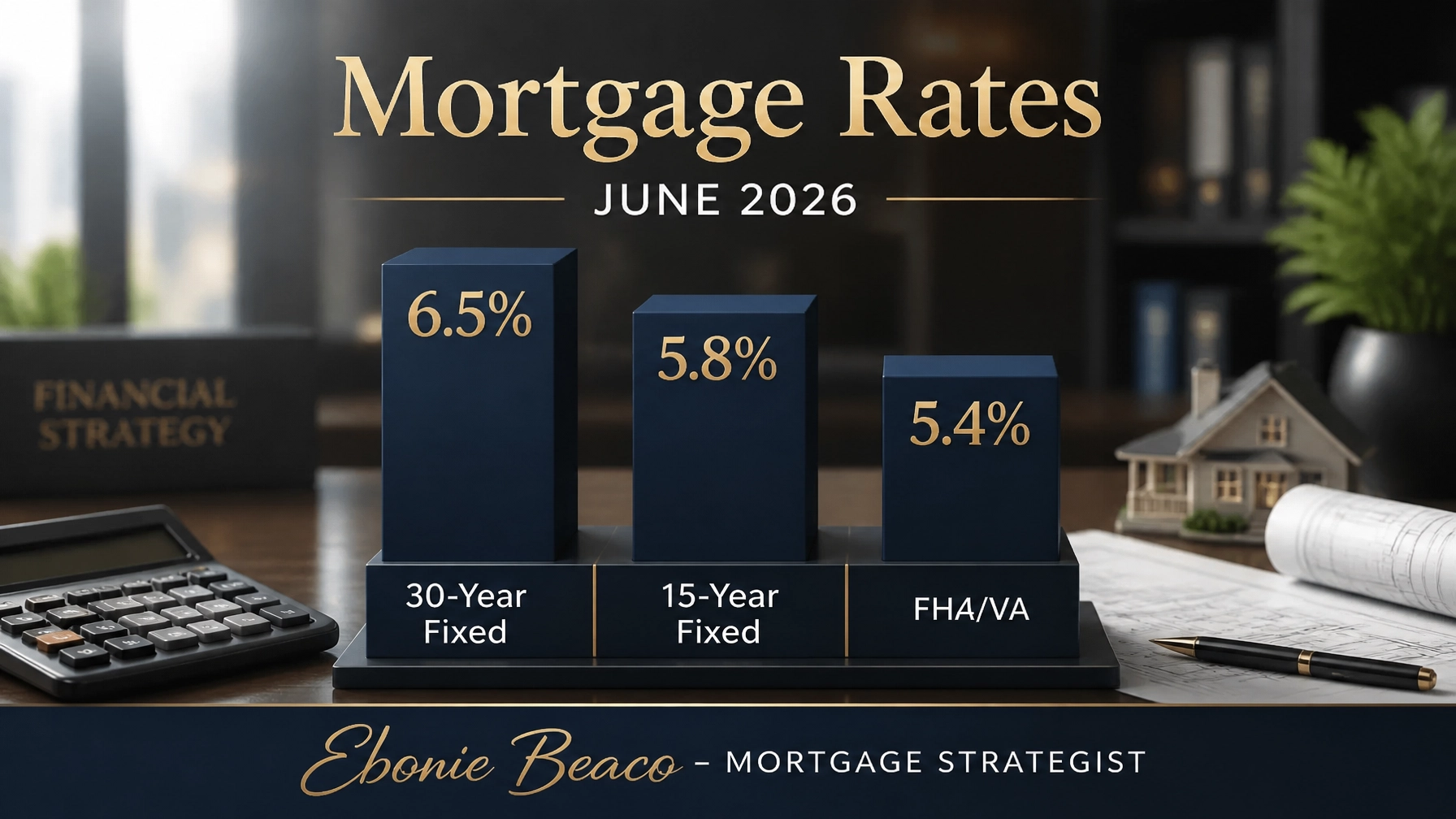

As of June 8, 2026, mortgage rates have found a temporary plateau, providing a clearer window for those looking to lock in financing for new acquisitions or refinances. According to recent data from Freddie Mac, the 30-year fixed-rate mortgage is averaging approximately 6.48%, a slight decrease from previous weeks but still reflective of a tight monetary policy. This stability is a welcome change for investors who have been navigating a high-rate environment for several quarters. For a more detailed daily breakdown, Bankrate’s mortgage analysis notes that 15-year fixed rates are clustering around the 5.82% mark, offering a lower-interest alternative for those with higher monthly cash flow capabilities.

Defining Key Mortgage Terms

Conforming Loan: A mortgage that adheres to the funding criteria and dollar limits set by government-sponsored entities like Fannie Mae and Freddie Mac.

You use these loans to secure standardized interest rates and terms for residential properties that fit within local price limits.

Jumbo Loan: A type of financing that exceeds the conforming loan limits established by the Federal Housing Finance Agency (FHFA).

You utilize jumbo loans when purchasing high-value properties, particularly in competitive markets like California or Northern Virginia, where home prices often surpass standard limit thresholds.

FHA Loan: A government-backed mortgage insured by the Federal Housing Administration, typically requiring lower down payments and credit scores than conventional loans.

You explore FHA options to reduce your initial capital outlay, which is particularly useful for first-time buyers in emerging markets like Alabama or Indiana.

Regional Market Trends: Inventory and Demand

National housing inventory growth has recently stalled, turning slightly negative year-over-year as of early June 2026. This trend creates a competitive atmosphere for well-priced listings, particularly in high-demand regions such as Florida, Georgia, and Illinois. While supply remains constrained, buyer demand has stayed surprisingly positive, suggesting that many have adjusted their expectations to the current rate environment. In states like Michigan and Missouri, we are seeing a focus on affordability, while California continues to experience low inventory coupled with high sustained property values.

Comparing different regions reveals a broadening slowdown in price growth, with some major metropolitan areas witnessing year-over-year price declines for the first time in years. This cooling effect is reflected in the S&P CoreLogic Case-Shiller index, which shows national home prices up only 0.7% annually. For investors, this environment underscores the importance of focusing on cash flow rather than banking solely on rapid appreciation. Strategic acquisition in markets like Arkansas or Kentucky can still yield strong returns if the financing is structured to account for localized demand and rental yields.

Real Estate Investor Strategy: Leveraging DSCR Loans

In a market where inventory is tight and prices are softening, real estate investors are increasingly turning to Debt Service Coverage Ratio (DSCR) loans to expand their portfolios. Unlike traditional mortgages that rely on personal income and W-2 documentation, DSCR loans qualify the borrower based on the income potential of the property itself. This approach is highly effective for landlords and short-term rental operators in states like Florida and Virginia, where vacation and urban rentals generate significant monthly revenue.

Calculating the DSCR Opportunity

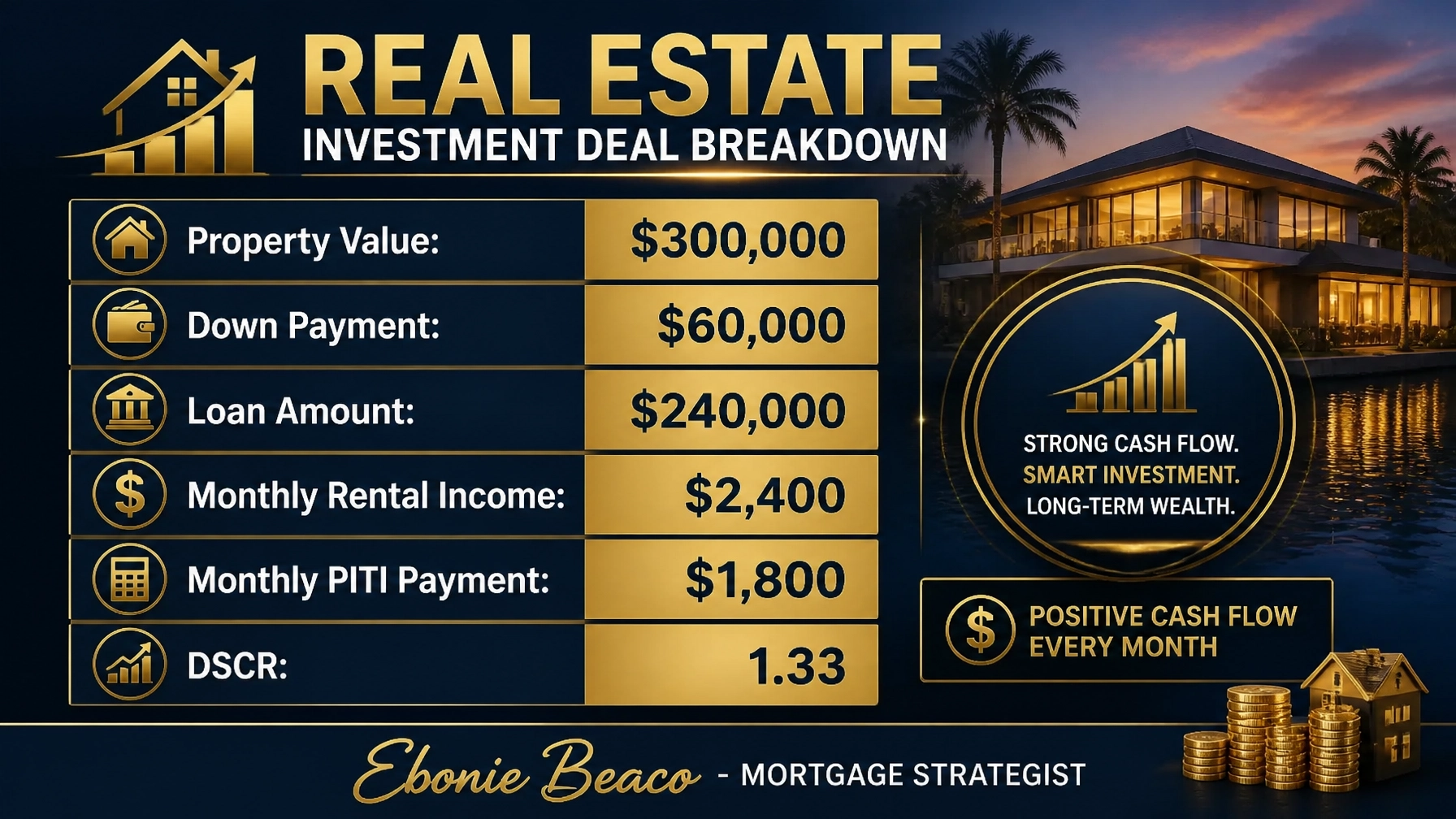

To understand how a DSCR loan works in practice, let us examine a typical investment scenario for a single-family rental property in a mid-sized market like Atlanta, Georgia, or Chicago, Illinois.

- Property Purchase Price: $300,000

- Down Payment (20%): $60,000

- Loan Amount: $240,000

- Monthly Rental Income: $2,400

- Total Monthly Expenses (PITI): $1,800

In this case, you calculate the DSCR by dividing the monthly rental income by the total monthly debt obligation ($2,400 / $1,800). This results in a DSCR of 1.33. Most lenders look for a ratio of 1.20 or higher to approve the loan without needing to verify your personal employment income. This strategy allows you to scale more quickly, as your ability to acquire the next property is not limited by your personal debt-to-income ratio.

Homeowner Equity Strategies: Refinancing and HELOCs

Current homeowners in states such as Virginia and California often sit on significant amounts of untapped equity due to the price appreciation seen over the last few years. Despite the current rates being higher than the historic lows of the early 2020s, there are still strategic reasons to access this capital. A cash-out refinance or a Home Equity Line of Credit (HELOC) can provide the necessary funds for property renovations, debt consolidation, or the down payment on a subsequent investment property.

Defining Equity Access Tools

Cash-Out Refinance: A mortgage refinancing option where the new loan is larger than the existing one, allowing the homeowner to receive the difference in cash.

You implement this strategy when you need a lump sum of capital for a major project, such as a fix-and-flip renovation or a ground-up development project.

HELOC (Home Equity Line of Credit): A revolving line of credit that uses your home as collateral, allowing you to borrow against your equity as needed.

You use a HELOC for ongoing flexibility, as it functions similarly to a credit card where you only pay interest on the amount you have actually drawn.

The Renovation Equity Multiplier

Consider a homeowner in Birmingham, Alabama, who owns a property valued at $500,000 with a remaining mortgage balance of $200,000. By utilizing a cash-out refinance at an 80% Loan-to-Value (LTV) ratio, they could potentially access $200,000 in liquid capital. If $100,000 of that capital is invested into a strategic kitchen and bathroom renovation, the overall property value could potentially rise to $650,000. This not only increases the homeowner's net worth but also prepares the property for higher rental yields if they decide to convert it into a long-term investment asset.

Navigating Macro-Economic Factors

The broader economic environment continues to influence the housing market through several key levers. Inflation remains a primary concern, with the April 2026 CPI showing a 3.8% year-over-year increase, which is significantly above the Federal Reserve's target. Geopolitical conflicts, particularly recent tensions in the Middle East, have also contributed to oil price spikes, adding further upward pressure on mortgage rates. Understanding these macro-trends helps you anticipate whether rates are likely to stay elevated or begin a downward trajectory in the coming months.

The Federal Reserve’s current federal funds rate of 3.50%–3.75% suggests a cautious stance toward further rate hikes, but also a reluctance to cut rates prematurely. For professionals in the real estate industry, this means operating in a "new normal" where financing must be structured with precision. Whether you are a wholesaler in Indiana looking for the next deal or a developer in Missouri planning a multi-unit complex, aligning your financing with these economic realities is the key to long-term success.

Conclusion: Building Wealth in a Shifting Market

The housing news for June 8, 2026, confirms that while the era of 3% interest rates is behind us, the opportunity to build wealth through real estate remains robust. By focusing on products like DSCR loans, cash-out refinancing, and Non-QM solutions, you can continue to expand your footprint across the 11 states we serve. Education and transparency are the most valuable assets you can have in this market, ensuring that every loan scenario is aligned with your broader financial goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664