The Ultimate Guide to Florida Jumbo Loans: Everything You Need to Succeed in Luxury Real Estate

Navigating the luxury real estate market requires more than just a sharp eye for architecture and a preferred zip code. In high-demand regions like Florida, California, and Atlanta, the price of entry often exceeds the limits of standard financing. When a home price climbs into the seven or eight-figure range, you enter the world of high-balance financing.

Florida Jumbo Loans are the primary vehicle for securing these high-end properties. Because these loans exceed the limits set by the Federal Housing Finance Agency (FHFA), they carry different rules, stricter requirements, and unique opportunities for the well-prepared buyer. Whether you are eyeing a waterfront estate in Miami or a historic mansion in Buckhead, understanding the mechanics of these loans is the first step toward a successful closing.

Defining the Jumbo Loan

Jumbo Loan: A non-conforming mortgage that exceeds the annual conforming loan limits established by the FHFA.

Because these loans cannot be purchased by Fannie Mae or Freddie Mac, lenders take on the full risk of the debt, leading to more rigorous underwriting standards.

In most Florida counties, the conforming loan limit for 2026 sits around $806,500. Any loan amount above this threshold is classified as a jumbo loan. However, in high-cost areas like Monroe County (the Florida Keys), the limit is higher, reflecting the local market's premium pricing.

In other major markets where Home Loans Network operates: such as the competitive landscapes requiring California Jumbo Loans or the urban sprawl of Chicago Jumbo Loans: the logic remains the same. You are essentially asking a lender to step outside the safety net of government-backed guarantees to fund your luxury investment.

Qualifying for a Florida Jumbo Loan: The High-Stakes Checklist

Securing a luxury mortgage is a transparent process of proving financial stability. Lenders look for "compensating factors" to offset the higher loan amounts. Here is what you need to prepare:

Credit Score Requirements

Credit Score: A numerical expression based on a level analysis of a person's credit files, to represent the creditworthiness of an individual.

For a jumbo loan, a score of 700 is typically the floor, though a 720 or 740 is preferred to access the most competitive rates. Lenders will examine your payment history, credit utilization, and the depth of your credit profile. If you have a history of high-balance credit management, you are positioned well.

Debt-to-Income (DTI) Ratios

DTI Ratio: The percentage of your gross monthly income that goes toward paying your monthly debt obligations.

While conventional loans might allow a DTI up to 50% in some cases, jumbo lenders usually cap this at 43% to 45%. They want to ensure that your lifestyle and existing debts do not compromise your ability to manage a significant mortgage payment.

Cash Reserves and Assets

Cash Reserves: Liquid assets that remain in your accounts after the down payment and closing costs are paid.

Lenders typically require 6 to 12 months of mortgage payments (Principal, Interest, Taxes, Insurance: PITI) to be held in reserve. For a $1.5 million loan with a $9,000 monthly payment, this means having an additional $54,000 to $108,000 in liquid or semi-liquid accounts. Explore our mortgage basics to see how reserves impact your overall profile.

Down Payment Strategies for High-Value Properties

The days of 3% down do not apply in the luxury sector. For most Florida Jumbo Loans, a 20% down payment is the industry standard. This equity stake protects the lender and often allows the borrower to avoid Private Mortgage Insurance (PMI).

However, flexible options do exist. Some specialized programs allow for 10% or 15% down for borrowers with exceptionally high credit scores and low DTI ratios. Jump in and compare how a larger down payment changes your monthly obligation using our mortgage calculators.

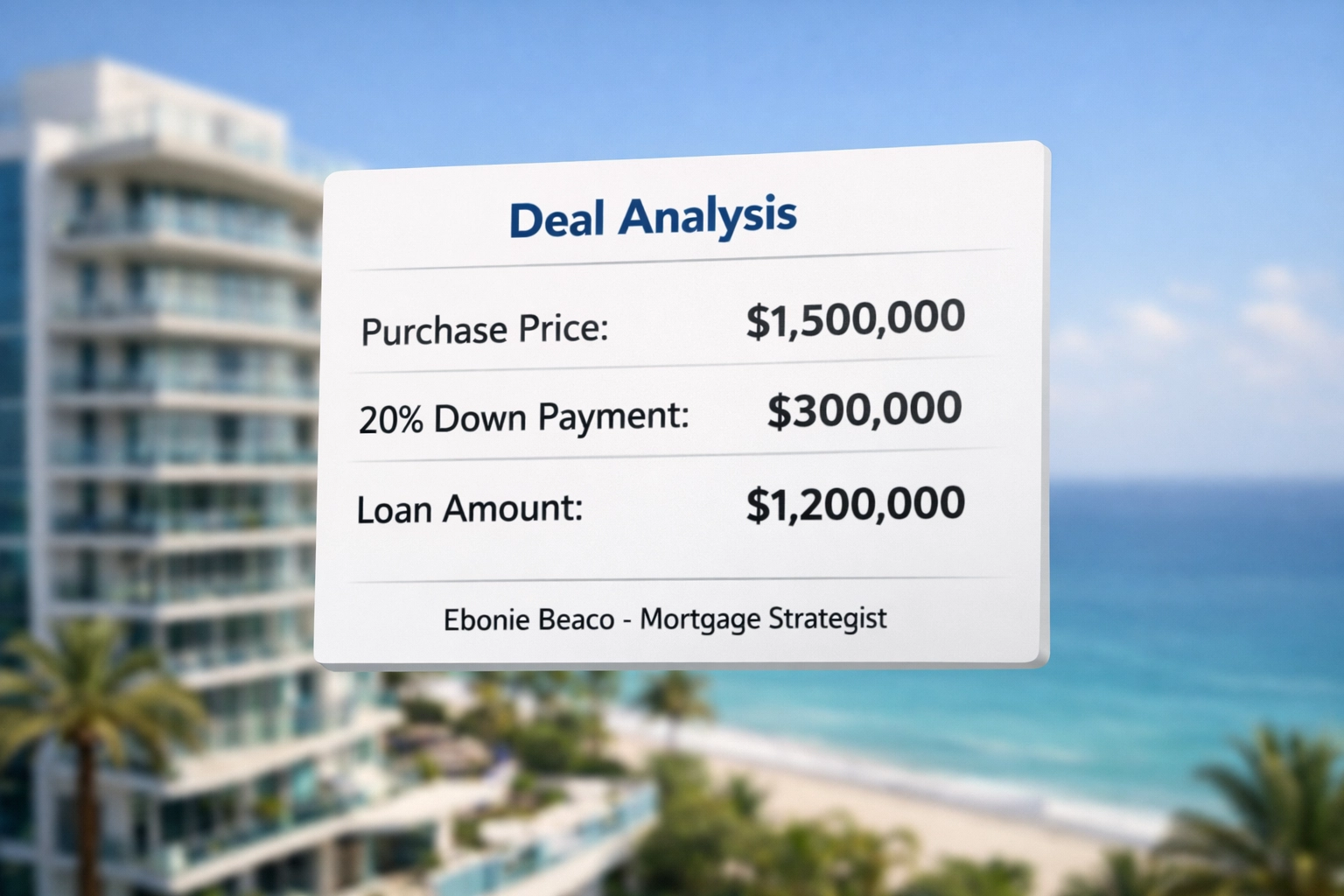

Real-World Example: The Palm Beach Acquisition

Imagine you are purchasing a luxury condo in Palm Beach for $1,500,000.

- Purchase Price: $1,500,000

- Down Payment (20%): $300,000

- Loan Amount: $1,200,000

- Interest Rate (Example): 6.5%

- Monthly P&I: $7,585

- Required Reserves (12 Months): $91,020 (Estimated)

In this scenario, the buyer needs at least $391,020 in total liquidity (excluding closing costs) to satisfy the lender's requirements. This transparency helps you plan your capital allocation before you even sign a purchase agreement.

Regional Nuances: FL, CA, and GA

While the fundamental rules of jumbo lending are consistent, local market activity influences how deals are structured.

- Florida: Focus is often on waterfront properties and high-rise condos. Lenders pay close attention to condo warrantability and association health.

- California: Given the extreme property values in cities like Los Angeles or San Francisco, California Jumbo Loans are the norm rather than the exception. Loan amounts here frequently reach the $3M to $5M range.

- Atlanta (Georgia): The luxury market in areas like Buckhead or Alpharetta often involves large estates with significant acreage. Appraisals for these unique properties can be more complex, requiring an expert who understands "comparable sales" in a niche luxury market.

Beyond the Standard: Non-QM and Interest-Only Options

Not every high-net-worth individual has a standard W-2 income. Many luxury buyers are entrepreneurs, investors, or self-employed professionals. For these scenarios, we look toward Non-QM (Non-Qualified Mortgage) options.

Bank Statement Loans: A mortgage program that uses 12 to 24 months of personal or business bank statements to verify income rather than tax returns.

This is an excellent fit for the self-employed buyer in Florida who has significant cash flow but utilizes legal tax deductions that lower their "taxable income" below jumbo qualification levels.

Interest-Only Mortgages: A loan where the borrower pays only the interest on the principal balance for a set term, usually 5 to 10 years.

Investors often use interest-only mortgages to maximize cash flow or to keep monthly payments low while they wait for a different asset to liquidate or a bonus to pay down the principal.

Financing Unique Properties: Condos and Waterfront Estates

Luxury real estate isn't always a single-family home on a suburban street. In Florida and Chicago, high-end condos are a staple.

Condo Warrantability: A status determining if a condominium project meets specific criteria for a lender to provide a mortgage.

For jumbo financing, lenders will check the "owner-occupancy" ratio of the building and ensure the Homeowners Association (HOA) has adequate insurance and reserve funds. If a building is "non-warrantable" (perhaps it allows short-term rentals or one person owns too many units), you may need a specialized jumbo program or a portfolio lender.

Waterfront estates also require specialized appraisal knowledge. Factors like sea wall condition, dockage rights, and flood zone designations can impact the property's valuation and your loan approval.

The Application Journey: What to Expect

The timeline for a jumbo loan is often longer than a standard mortgage, typically ranging from 30 to 60 days. This is due to the "manual underwriting" process.

Manual Underwriting: A human review of a loan application where the underwriter evaluates the borrower's creditworthiness based on documentation rather than an automated system.

Because the loan amounts are high, an actual person will scrutinize your tax returns, asset statements, and business holdings. You should be prepared to provide:

- Two years of full tax returns (Personal and Business).

- Recent 30 days of pay stubs or profit/loss statements.

- 60 to 90 days of bank statements for all accounts.

- Proof of additional income (RSUs, dividends, or rental income).

Access our loan process page to see a step-by-step breakdown of how we move from application to clear-to-close.

Strategic Thinking for Real Estate Investors

If you are a landlord or real estate investor looking at high-value rental properties, the jumbo landscape changes slightly. DSCR (Debt Service Coverage Ratio) Loans are often a preferred alternative for luxury rentals, including Airbnb or short-term rental properties in Florida.

DSCR: A ratio of a property's net operating income to its debt obligations.

With a DSCR loan, the lender cares less about your personal income and more about whether the property's rent can cover the mortgage payment. For high-end vacation rentals in markets like Destin or Miami, this strategy allows investors to scale their portfolios without hitting the DTI ceilings associated with traditional jumbo loans.

Why Partner with a Mortgage Strategist?

Luxury real estate transactions are complex. They involve high stakes, intricate legal structures (like purchasing through a Trust or LLC), and unique property types. Working with a dedicated strategist ensures that you are not just getting a loan, but building a financial foundation.

We help you compare options between traditional Florida Jumbo Loans, bank statement programs, and investor-focused financing. Our goal is to provide a transparent path to homeownership or investment success, ensuring you understand every calculation and requirement along the way.

Explore our testimonials to see how we have guided other high-balance buyers through the process, or review our frequently asked questions for more targeted insights.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664