The Ultimate Guide to Florida Airbnb Financing Loans: Everything You Need to Succeed

SEO Title: Florida Airbnb Financing Loans: The Ultimate Guide for 2026

Meta Description: Learn how to finance Florida short-term rentals using DSCR loans and bank statement mortgages. Master Florida Airbnb financing strategies for Miami, Orlando, and beyond.

URL Slug: florida-airbnb-financing-loans-guide

Featured Image Recommendation: Use the generated luxury Florida coastal property image (https://cdn.marblism.com/gwX6ffNBdJj.webp) as the primary thumbnail.

SEO Alt Text: Luxury Florida vacation rental home with a private pool and palm trees, showcasing Airbnb investment opportunities.

Social Media Excerpt: Ready to scale your Florida Airbnb portfolio? From DSCR loans to bank statement financing, our ultimate guide covers the strategies you need to thrive in the 2026 Florida rental market.

SEO Tags: Florida Airbnb loans, DSCR financing Florida, short term rental loans, real estate investment Florida, bank statement mortgage, Miami real estate, Orlando vacation rentals.

{kind=link}

Florida remains one of the most competitive and lucrative landscapes for short-term rental (STR) investors. From the high-energy beachfronts of Miami to the family-centric vacation hubs of Orlando, the demand for high-quality Airbnb properties continues to grow. For investors looking to acquire or refinance these assets, traditional mortgage products often fall short because they do not account for the unique income potential of a vacation rental.

Successful investors in the Sunshine State utilize specialized financing strategies to build their portfolios. Whether you are a seasoned landlord or a first-time investor, understanding how to leverage programs like DSCR loans and bank statement mortgages is essential. This guide provides a comprehensive overview of the financing landscape for Florida Airbnbs in 2026, helping you navigate regulations and optimize your cash flow.

Understanding DSCR Loans for Florida Rental Properties

DSCR Loan Definition: A Debt Service Coverage Ratio (DSCR) loan is a mortgage program that qualifies a borrower based on the cash flow generated by the investment property rather than personal income documentation such as tax returns or W-2s.

The practical benefit of this program is that it allows you to scale your portfolio without being restricted by your personal debt-to-income (DTI) ratio. In Florida, lenders analyze the projected or actual Airbnb revenue to determine if the property can cover its own mortgage payments. This is particularly useful in high-yield markets like Sarasota and Tampa, where short-term rental rates significantly outperform long-term lease rates.

When applying for a DSCR loan, you will often need to provide a 12-month history of platform statements from Airbnb or Vrbo. If you are purchasing a new property, lenders may use an "AirDNA" report or similar market data to estimate the potential income. To prepare your application, you can use a DSCR loan pre-qualification worksheet to organize your numbers before speaking with a lender.

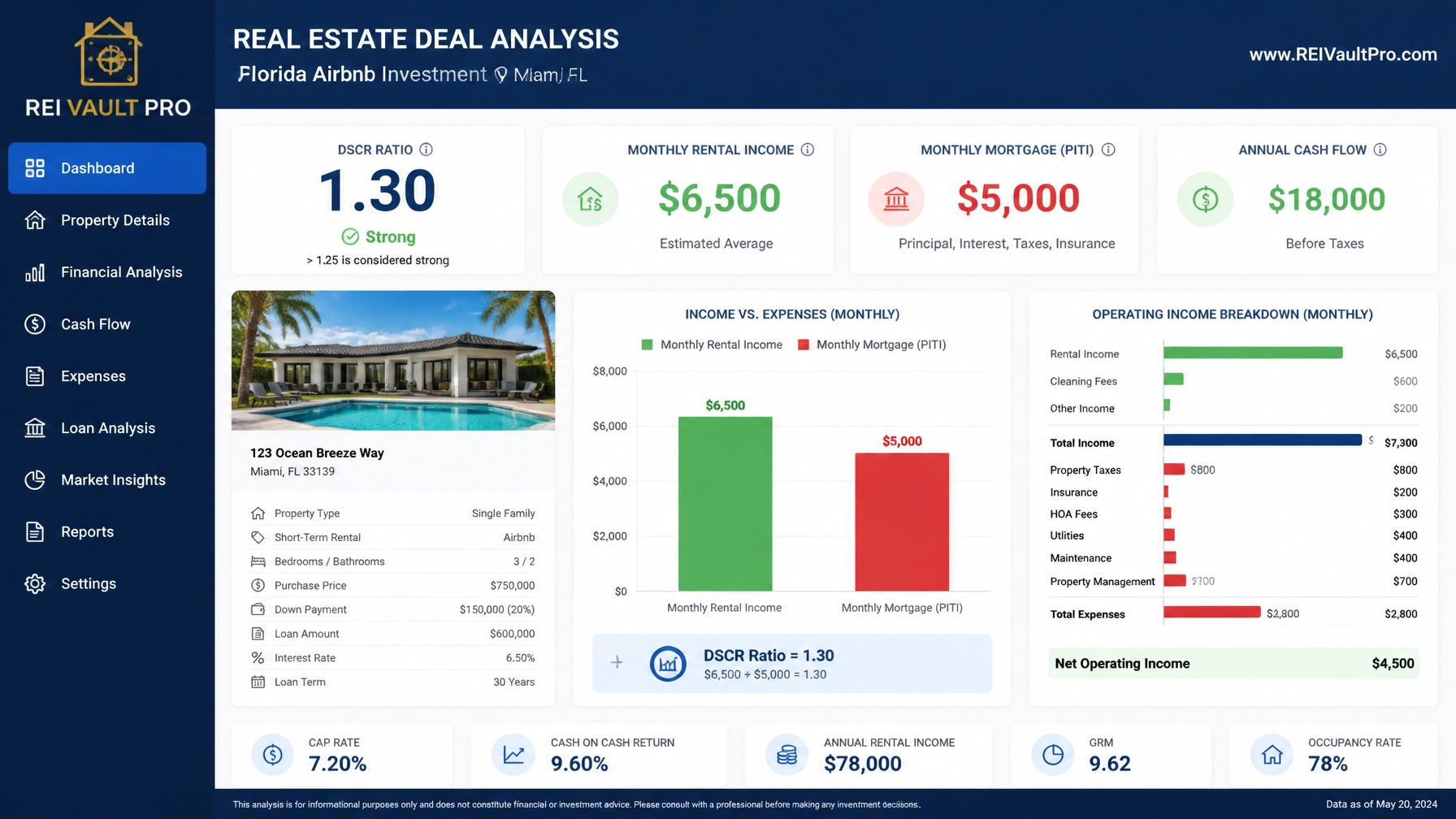

Financial Strategy: The DSCR Calculation in Action

To understand how a lender views your Florida Airbnb, look at the math behind the approval. Lenders typically look for a ratio of 1.0 or higher, though a 1.20 to 1.30 ratio often secures more favorable interest rates.

Imagine you are purchasing a luxury vacation home in Miami for $750,000. You plan to put 25% down, resulting in a loan amount of $562,500. After calculating your principal, interest, taxes, insurance, and HOA fees (PITI), your total monthly obligation is $5,000.

If the property generates a monthly average of $6,500 in short-term rental income, your DSCR is calculated as follows:

$6,500 (Income) / $5,000 (Debt) = 1.30 DSCR

A 1.30 ratio indicates that the property produces 30% more income than is required to pay the mortgage. This makes the deal highly attractive to lenders.

Bank Statement Loans for Self-Employed Hosts

Bank Statement Loan Definition: A mortgage program designed for self-employed borrowers that uses 12 to 24 months of personal or business bank statements to verify income instead of traditional tax documentation.

Many Airbnb hosts are entrepreneurs or business owners whose tax returns show significant deductions, which can lower their qualifying income for a conventional loan. In Florida's thriving gig and tourism economy, bank statement loans provide a vital path to ownership.

These loans are ideal when your property is located in a seasonal market where the DSCR might fluctuate throughout the year. If your personal business income is strong and consistent, you can use that strength to secure financing for a vacation home or investment property. You should maintain an accurate rent roll template to show the stability of your existing portfolio when opting for this route.

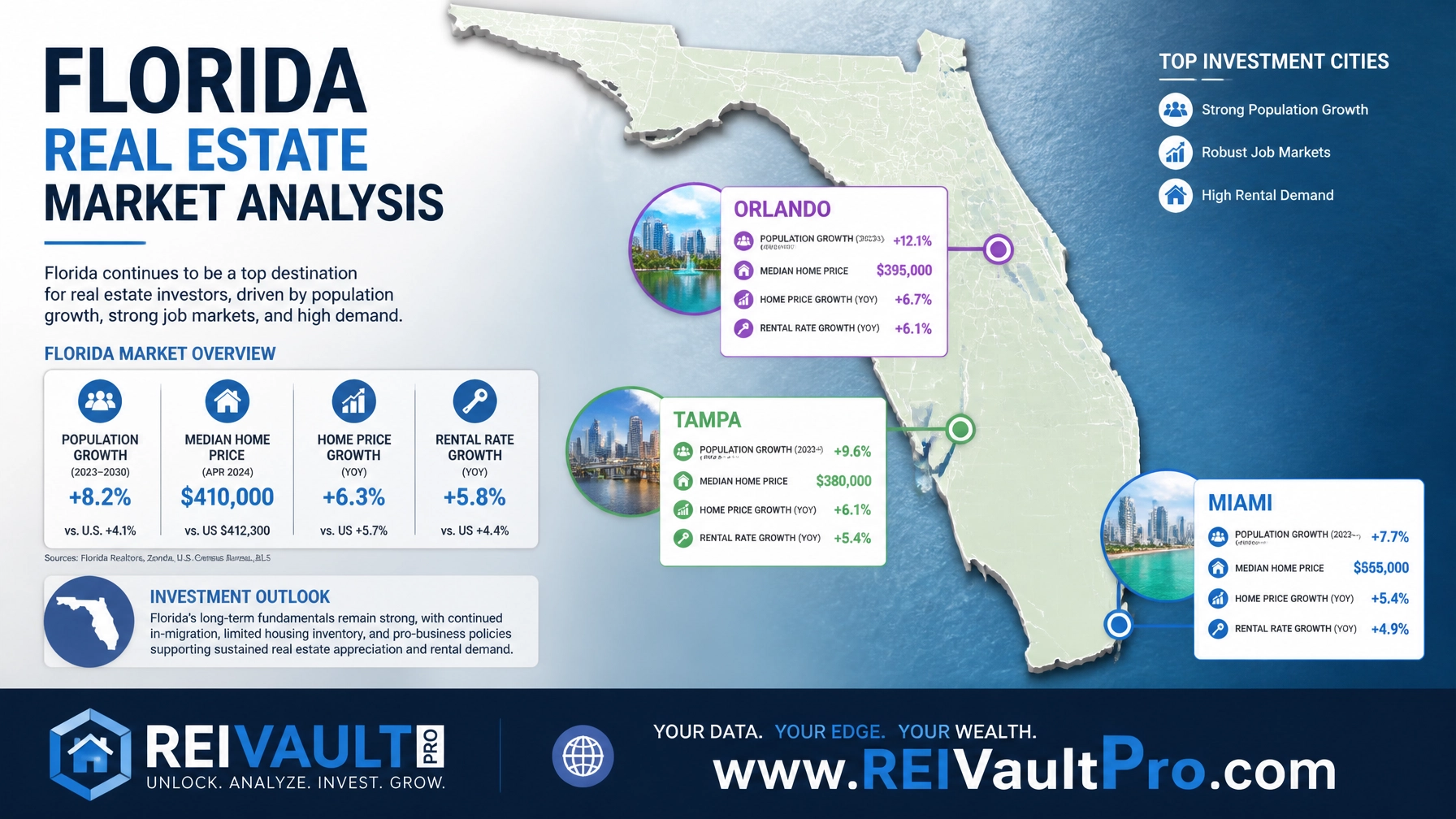

Florida Real Estate Market Trends in 2026

The Florida market is characterized by regional diversity. While Miami continues to see high demand for luxury condos and coastal villas, inland areas like Orlando benefit from a steady stream of tourism tied to major attractions. In 2026, we are seeing a shift toward "bleisure" travel, where guests combine business and leisure trips, leading to longer average stays in metropolitan hubs.

Investors are also looking at emerging markets in the Florida Panhandle and the Space Coast. These areas often offer lower entry prices while maintaining strong occupancy rates. Before committing to a location, it is wise to perform a deep dive using AI market analysis to identify which neighborhoods are trending upward in terms of daily rates and occupancy.

Fix and Flip Strategies for Short-Term Rentals

Some of the most profitable Florida Airbnbs began as distressed properties. By using a fix and flip or bridge loan, you can acquire a property that needs renovation, modernize it for the luxury rental market, and then refinance into a long-term DSCR loan once the work is complete.

This strategy, often referred to as the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method, allows you to build equity rapidly. When managing a renovation in Florida, cost control is critical. You should use a contractor bid comparison sheet to ensure you are getting fair pricing on high-end finishes that will attract Airbnb guests.

Modernizing a kitchen or adding a pool can significantly increase your nightly rate. High-quality visuals in your listing are what drive bookings, so the physical condition of the property is just as important as the financing structure.

Navigating Florida’s 2026 Short-Term Rental Regulations

Compliance is a non-negotiable part of your investment strategy. Florida state law provides a framework for vacation rentals, but local municipalities have the authority to implement stricter rules. For example, as of 2026, cities like Sarasota require mandatory registration and annual inspections for all STR operators.

Lenders are increasingly sensitive to these regulations. If a property is located in a zone where short-term rentals are restricted, a DSCR loan based on Airbnb income will likely be denied. You must verify that the property has the necessary licenses and that you are prepared to collect and remit the Florida sales tax and local tourist development taxes.

Jump in and research the specific zoning of any property before you sign a purchase agreement. Using professional calculators to factor in these additional regulatory costs and taxes will give you a more realistic view of your potential ROI.

How to Choose the Right Financing Option

Choosing between a DSCR loan and a bank statement loan depends on your specific financial profile and the property’s performance.

- Explore DSCR Loans if: Your property has a strong, proven track record of rental income and you want to keep your personal finances separate from your real estate business.

- Explore Bank Statement Loans if: You are self-employed with high bank deposits but your property’s rental history is new or highly seasonal.

- Explore Bridge Loans if: The property needs significant repairs before it can be listed on Airbnb.

Compare your options carefully. By aligning your financing with your long-term goals, you can build a sustainable and profitable real estate portfolio in Florida.

Related REI Vault Pro Resources

- DSCR Loan Pre-Qualification Worksheet: Use this tool to calculate your property’s potential ratio and see if you qualify for professional investor financing. This helps you approach lenders with confidence.

- AI Market Analysis: Access real-time data on Florida neighborhoods to identify the best areas for short-term rental growth and high occupancy rates.

- Rent Roll Template: A vital resource for tracking your current rental income across multiple platforms, which is essential for refinancing or expanding your portfolio.

- Contractor Bid Comparison Sheet: If you are renovating a Florida property to increase its Airbnb value, use this sheet to manage your rehab costs effectively.

- Real Estate Calculators: A comprehensive suite of tools to help you analyze ROI, cash flow, and the long-term profitability of any Florida investment deal.

Access the tools and guidance you need to dominate the Florida short-term rental market. Whether you are buying your first beachfront condo or scaling a multi-city portfolio, professional financing is the key to your success.

Watch a Demo to see how REI Vault Pro can streamline your investment strategy: https://reivaultpro.com/demo

Frequently Asked Questions

Can I use Airbnb income to qualify for a mortgage in Florida?

Yes. Through DSCR loan programs, lenders specifically use the gross income generated by platforms like Airbnb and Vrbo to qualify the property for financing. This often requires 12 months of history or a market rent analysis.

What is the minimum down payment for a Florida Airbnb loan?

Most DSCR and bank statement loans for investment properties require a minimum down payment of 20% to 25%. Some specialized programs may allow for lower down payments depending on your credit score and the property type.

Do I need a business license for an Airbnb in Florida?

Yes. Florida requires vacation rental dwellings to be licensed through the Department of Business and Professional Regulation (DBPR). Additionally, many cities and counties require local permits and the payment of tourist development taxes.

Can I get an Airbnb loan in an LLC?

Yes. Most DSCR lenders actually prefer or require that you hold the property in an LLC. This provides a layer of liability protection and is a common practice among professional real estate investors.

Are interest rates higher for Airbnb loans than for primary residences?

Generally, yes. Financing for investment properties typically carries a higher interest rate than a primary residence mortgage because lenders perceive a higher level of risk with rental properties.