The Ultimate Guide to California Hard Money: Everything You Need to Close Fast and Succeed

In the world of real estate investing, speed is often the difference between a winning bid and a missed opportunity. Whether you are eyeing a distressed property in Los Angeles, a bungalow in Miami, or a multi unit building in Chicago, traditional bank financing usually takes too long. By the time a big bank finishes their mountain of paperwork, another investor has already closed the deal with cash or a hard money loan.

If you want to compete in high demand markets like California, Florida, or Georgia, you need to understand how hard money works. This guide breaks down the mechanics of asset based lending and how you can use it to scale your portfolio.

What is California Hard Money?

Hard Money Loan: A short term, asset based loan secured by real estate. Unlike traditional mortgages that focus on the borrower’s credit score and income, hard money lenders focus primarily on the value of the property and its potential after renovation.

In California, where property values are high and the market moves at lightning speed, hard money is the engine behind most fix and flip projects. Investors use these loans to bridge the gap between purchase and permanent financing or resale.

Why Investors Choose Hard Money over Banks

Traditional lenders are risk averse. They want to see years of tax returns, high credit scores, and properties that are already in perfect condition. Hard money lenders look at things differently. They see the potential in a "fixer upper" that a bank wouldn't touch.

- Speed: Closings often happen in 3 to 7 days.

- Flexibility: Terms can be customized to fit the project timeline.

- Asset Focused: The property is the primary collateral, making it accessible for investors with unique financial profiles.

The Mechanics of California Fix and Flip Loans

When you are looking for California fix and flip loans, you need to understand the three most important numbers: Purchase Price, Renovation Budget, and After Repair Value (ARV).

After Repair Value (ARV): The estimated market value of a property after all planned renovations and improvements are completed.

Lenders typically lend based on a percentage of the ARV, usually around 70% to 75%. This ensures there is enough equity in the deal to protect the lender while giving the investor the capital needed to complete the project.

Interest Rates and Points

Hard money is more expensive than a 30 year fixed mortgage. You are paying for speed and convenience.

- Interest Rates: Generally range from 8.5% to 12% depending on experience.

- Points: Upfront fees (origination) typically between 1 and 3 points.

- Loan Term: Usually 6 to 18 months.

Scaling Your Strategy in Florida and Chicago

While this guide focuses on California, the principles of hard money apply across the country. If you are looking for Florida fix and flip loans or Chicago fix and flip loans, the process remains remarkably consistent.

In Florida, investors often target short term rental properties (Airbnb) or rapid flips in growing coastal markets. In Chicago, the focus is often on multi unit properties where investors can add value through structural renovations.

Regardless of the location, the goal is the same: Get in, fix it, and get out.

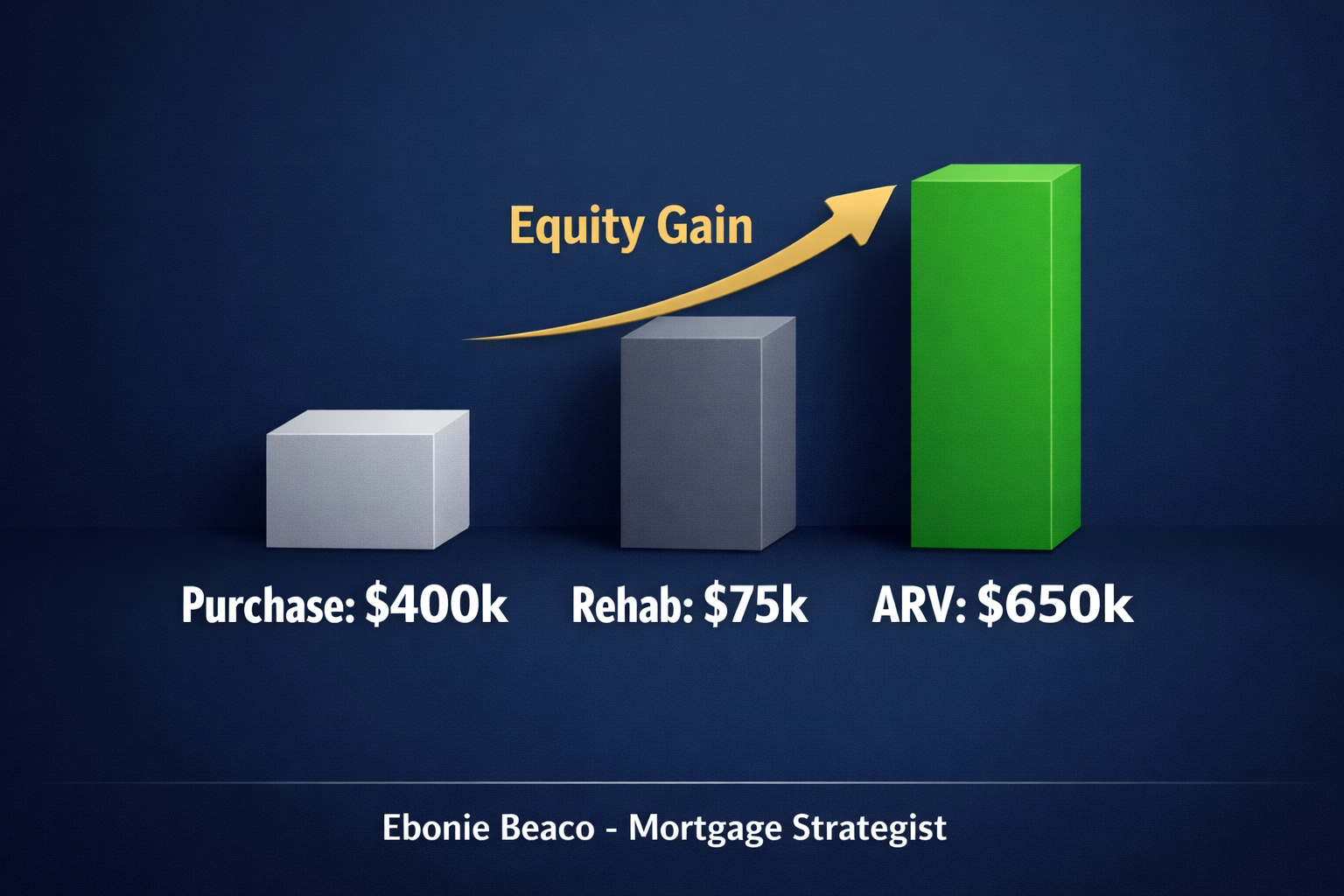

Real World Scenario: The $500k Fix and Flip

Let’s look at how the numbers actually work in a real life transaction. Imagine you find a distressed single family home in a solid California neighborhood.

- Purchase Price: $400,000

- Renovation Budget: $75,000

- Closing/Holding Costs: $25,000

- Total Project Cost: $500,000

- Projected ARV: $650,000

In this scenario, a hard money lender might offer a loan covering 90% of the purchase price and 100% of the renovation costs.

- Loan Amount: $360,000 (Purchase) + $75,000 (Renovation) = $435,000

- Investor Down Payment: $40,000 (plus closing costs)

By using a hard money loan, you are only putting up a small fraction of the total project cost. This allows you to keep your cash liquid for other deals or unexpected expenses during the renovation.

How to Qualify for Hard Money

Because these loans are asset based, the qualification process is much more streamlined than a traditional mortgage. However, you still need to bring a solid plan to the table.

1. The Property Appraisal

The lender will order an appraisal to verify the current value and the ARV. They want to make sure the "comps" (comparable properties) in the area support your projected sale price.

2. Experience Matters

If you are a first time flipper, you might pay a slightly higher interest rate. As you build a track record and successfully close deals, lenders will often lower your rates and increase your leverage.

3. Exit Strategy

A lender wants to know how they are going to get their money back. Are you selling the property? Are you refinancing it into a long term DSCR investor loan? Having a clear exit strategy is crucial.

DSCR Loan: A Debt Service Coverage Ratio loan is a long term financing option for rental properties that qualifies the borrower based on the property’s rental income rather than personal income.

Common Myths About Hard Money

There are many misconceptions about this type of lending. Let’s clear a few up.

Myth: Hard money is only for people with bad credit. Reality: While hard money is a great option for those with lower credit scores, many high net worth investors with perfect credit use hard money solely for the speed and the ability to leverage their capital across multiple projects.

Myth: It’s "Loan Sharking." Reality: Hard money is a regulated and professional industry. In California, lenders must comply with the California Financing Law (CFL) and hold proper licensing through the DRE or NMLS.

Myth: You don't need any money down. Reality: While "100% financing" deals exist, most reputable lenders want the investor to have some "skin in the game," usually 10% to 20% of the purchase price.

Transitioning from Flip to Rental: The BRRRR Method

Many investors use hard money as the first step in the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

- Buy: Use hard money to acquire a distressed property.

- Rehab: Use the renovation draws to fix the property.

- Rent: Place a tenant to generate cash flow.

- Refinance: Move from the high interest hard money loan into a long term, lower interest DSCR rental property loan.

- Repeat: Take the cash out from the refinance and use it as a down payment for your next hard money deal.

This strategy allows you to build a massive portfolio of rental properties with very little of your own money left in the deals once they are refinanced.

Closing Fast: What You Need to Get Started

If you have a deal under contract and need to close in a matter of days, here is what you should have ready:

- The Executed Purchase Contract: The signed agreement between you and the seller.

- The Scope of Work: A detailed list of renovations and cost estimates.

- Entity Documents: Most hard money loans are made to LLCs or Corporations rather than individuals.

- Proof of Funds: Showing you have enough cash for the down payment and initial holding costs.

Conclusion

California hard money is a powerful tool for any real estate investor looking to compete in today's market. It provides the speed of cash with the benefit of leverage. Whether you are focused on California fix and flip loans, Florida fix and flip loans, or expanding into the Midwest with Chicago fix and flip loans, understanding the nuances of asset based lending will set you apart from the competition.

The key to success is working with a strategist who understands the numbers and can help you navigate the transition from acquisition to exit. Don't let a great deal slip away because you are waiting on a bank.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664