The Ultimate Guide to California Fix and Flip Loans: Everything You Need to Succeed

SEO Title: The Ultimate Guide to California Fix and Flip Loans: Everything You Need to Succeed

Meta Description: Master California fix and flip loans in 2026. Learn about hard money requirements, interest rates, and financing strategies to scale your CA real estate portfolio.

URL Slug: california-fix-and-flip-loans-guide

Featured Image Recommendation: A professional landscape photograph of a mid-century modern California home undergoing a high-end renovation with the URL www.REIVaultPro.com.

SEO Alt Text: Professional renovation of a California home representing fix and flip investment opportunities.

Social Media Excerpt: Ready to scale your house flipping business in California? 🌴 Our latest guide breaks down everything you need to know about fix and flip loans in 2026, from hard money requirements to real-world deal analysis. Dive in and start building your real estate empire! #RealEstateInvesting #CaliforniaRealEstate #FixAndFlip #REIVaultPro

SEO Tags: California real estate, fix and flip loans, hard money loans CA, real estate investment financing, house flipping 2026, REI Vault Pro, bridge loans California, property renovation funding

California remains one of the most dynamic real estate markets in the United States, offering significant opportunities for investors to acquire distressed properties, renovate them, and sell for a profit. However, the high barrier to entry and substantial capital requirements make specialized financing a necessity. Understanding the nuances of California fix and flip loans is essential for any investor looking to scale their business in 2026.

Navigating the landscape of asset-based lending requires a clear grasp of how lenders evaluate risk and how you can position your projects for approval. Whether you are targeting single-family homes in Los Angeles or multi-unit buildings in San Diego, the right financing strategy can be the difference between a successful exit and a stalled project.

Understanding California Fix and Flip Loans

Fix and flip loans are short-term, asset-based financing solutions designed specifically for real estate investors who purchase properties, perform renovations, and sell them within a 12 to 18-month window. Unlike traditional mortgages, these loans focus on the property's potential value rather than just its current condition.

Fix and Flip Loan: A short-term financing tool used to acquire and renovate a property for resale.

This allows you to leverage your capital across multiple projects rather than tying up all your liquidity in a single purchase.

After Repair Value (ARV): The estimated market value of a property after all planned renovations and improvements are completed.

Lenders use this figure to determine the maximum loan amount they are willing to provide.

Loan-to-Cost (LTC): The ratio of the loan amount to the total cost of the project, including purchase and rehab.

This metric helps you understand how much of your own cash you will need to contribute to the deal.

In California, where property values often exceed national averages, these loans provide the speed and flexibility needed to compete with all-cash buyers. By using an After Repair Value Justification Report, you can demonstrate to lenders that your projected exit price is backed by solid market data.

Types of Financing for California Real Estate Investors

Investors in the Golden State have several options when it comes to funding their flips. Each has its own set of advantages depending on your experience level and the specific needs of the project.

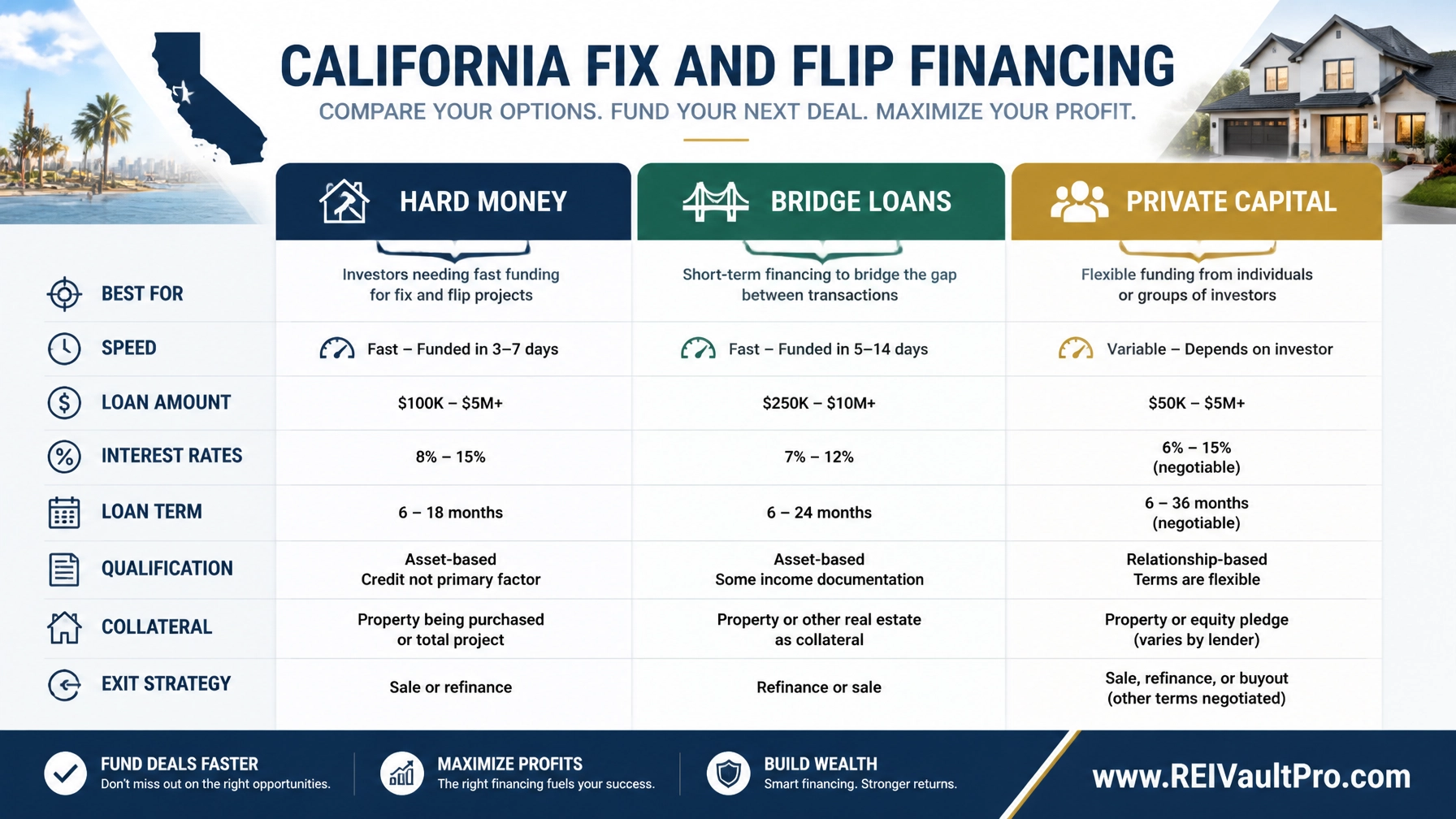

Hard Money Loans

Hard money is the most common choice for house flippers. These loans are provided by private lenders or investment firms and are secured by the real estate itself. They offer rapid funding, often closing in as little as 7 to 10 days, which is crucial in competitive markets like San Francisco or Orange County.

Bridge Loans

A bridge loan serves as a temporary financing solution to "bridge" the gap between the acquisition of a property and its eventual resale or long-term refinancing. These are often used when an investor needs to move quickly on a pre-foreclosure offer but plans to transition into a more permanent loan later.

Private Money Capital

Private money comes from individuals or small groups looking for a return on their capital. While terms can be more flexible, these lenders often require a high degree of trust and a professional Lender Package to move forward.

2026 Requirements for California Flip Loans

As we move through 2026, California lenders have refined their underwriting criteria to reflect current market conditions. While asset-based lending is more flexible than bank financing, there are still core benchmarks you should aim to meet.

- Credit Score: Most competitive programs in California look for a FICO score of 650 to 700+. Lower scores may be accepted but often result in higher interest rates or lower leverage.

- Experience: Lenders categorize investors by the number of completed flips in the last 24 to 36 months. Investors with 2+ successful exits typically access better terms, including lower points and higher LTC.

- Down Payment: Expect to bring 10% to 25% of the purchase price to the closing table. Highly experienced flippers can sometimes find "100% of rehab" funding if the purchase leverage is kept around 80-85%.

- Liquidity: You must show proof of funds for the down payment, closing costs, and at least 3 to 6 months of interest payments. A professional Proof of Funds Letter is often required during the bidding phase.

Financial Case Study: A California Fix and Flip Breakdown

To understand how these loans function in practice, let’s analyze a typical mid-range flip in a suburban California market.

In this scenario, an investor identifies a distressed property with the following profile:

- Purchase Price: $600,000

- Renovation Budget: $100,000

- Total Project Cost: $700,000

- Projected After Repair Value (ARV): $900,000

The lender offers a loan at 90% of the purchase price and 100% of the renovation costs, provided the total loan does not exceed 75% of the ARV.

- Loan for Purchase (90%): $540,000

- Loan for Rehab (100%): $100,000

- Total Loan Amount: $640,000

- Investor Cash In (Down Payment + Closing): $60,000 + ~$15,000 = $75,000

With an ARV of $900,000, the total loan of $640,000 represents a 71% LTV, which fits comfortably within the lender's guidelines. After paying back the $640,000 loan and accounting for $45,000 in interest and selling costs, the investor realizes a net profit of approximately $140,000. Using calculators to run these numbers before making an offer is vital to ensuring a project's viability.

How to Structure Your Deal for Maximum Profit

Success in California house flipping is not just about finding a good house; it is about structuring the financing to protect your margins. Many investors fail because they underestimate the "holding costs", the interest and fees paid while the property is being renovated and listed.

You should always have a clear Fix and Flip Exit Strategy Summary prepared. This document outlines how you intend to repay the loan, whether through a quick sale or a refinance into a long-term rental loan.

Leveraging AI Market Analysis can also help you identify which zip codes in California are seeing the fastest appreciation, allowing you to focus your efforts where the demand for renovated homes is highest.

The Step-by-Step Application Process

Securing a California fix and flip loan is a streamlined process compared to a conventional mortgage, but it requires thorough documentation.

- Entity Formation: Most lenders require you to close in the name of a business entity, such as an LLC or S-Corp.

- Project Submission: Provide the purchase contract, a detailed scope of work, and your Contractor Bid Comparison Sheet.

- Appraisal/Feasibility: The lender will order an "as-is" and "subject-to-completion" appraisal to verify the ARV.

- Underwriting: The lender reviews your experience, credit, and the property’s profit potential.

- Closing: Funds are escrowed for the purchase, and the rehab portion of the loan is typically held in a "draw account" to be released as work is completed.

Navigating the California Market in 2026

The California market in 2026 requires a surgical approach. While coastal cities like Santa Monica or La Jolla offer high exit prices, the competition for distressed inventory is fierce. Inland regions like the Central Valley or parts of the Inland Empire often provide more accessible entry points with strong demand from first-time homebuyers.

By focusing on "forced appreciation", adding value through square footage additions, ADUs (Accessory Dwelling Units), or high-end finishes, you can create a significant spread even in a stable price environment. Always ensure your projects align with the specific desires of the local demographic to ensure a quick sale.

Related REI Vault Pro Resources

- After Repair Value Justification Report: A critical tool for proving your project's potential value to lenders and investors. Access it here.

- Lender Package: Fix & Flip: A professional template to organize your financial and project data for quick loan approval. Get the template.

- Fix and Flip Exit Strategy Summary: Define your path to profit and repayment with this structured summary tool. Download now.

- Contractor Bid Comparison Sheet: Manage your renovation budget effectively by comparing multiple contractor quotes side-by-side. View resource.

- Proof of Funds Letter: Secure your next deal by showing sellers you have the backing to close quickly. Generate yours.

Scaling a real estate investment business in California requires a combination of local market knowledge and sophisticated financing strategies. By understanding how to leverage fix and flip loans, you can take on larger projects and build significant wealth through real estate. Explore your options and prepare your next deal with confidence.

Compare your financing options today and secure the capital you need for your next California project.

Join REI Vault Pro | Watch a Demo

FAQ Section

What is the average interest rate for a California fix and flip loan in 2026?

In 2026, interest rates for California fix and flip loans typically range between 9% and 13%. These are interest-only loans, meaning your monthly payments only cover the interest, with the principal due at the end of the term. Factors such as your credit score and previous flipping experience will determine your specific rate.

Do I need a high credit score for a fix and flip loan in California?

While these are asset-based loans, most lenders prefer a FICO score of at least 650. If you have significant experience and a high-equity deal, some lenders may approve scores as low as 620, though this often comes with higher points and lower leverage.

How much money do I need to flip a house in California?

Most California lenders require a down payment of 10% to 25% of the purchase price. Additionally, you should have enough cash to cover closing costs and approximately six months of interest payments. For a $600,000 property, you should expect to have at least $75,000 to $100,000 in liquid reserves.

Can I get a fix and flip loan as a first-time investor?

Yes, many lenders work with new investors. However, first-time flippers may be required to put down a larger down payment (often 20-25%) and may face slightly higher interest rates compared to seasoned professionals. Providing a detailed scope of work and using professional tools can help build lender confidence.

How long does it take to get funded for a fix and flip loan?

One of the primary benefits of these loans is speed. In California, many private and hard money lenders can fund a deal in 7 to 14 days, provided the title and appraisal are completed promptly. This is significantly faster than the 30-45 days required for a traditional bank loan.