The Truth About Hard Money Loans: Speed vs. Cost

If you are active in the real estate investing world, you have likely heard the term "hard money" thrown around at REIA meetings or on investor forums. To some, it sounds like a lifesaver; to others, it sounds like an expensive trap. The reality is that hard money is a specific tool designed for a specific job.

In the fast-moving markets of Chicago, Atlanta, and Miami, waiting 45 days for a traditional bank to approve a mortgage is a guaranteed way to lose a deal. This is where hard money enters the frame. It provides the fuel for fix-and-flip projects, bridge financing, and quick acquisitions that traditional lenders won't touch.

Understanding the balance between the speed of these loans and their actual cost is the difference between a profitable exit and a financial headache.

What is a Hard Money Loan?

A hard money loan is an asset-based financing option where the loan is secured by the value of the real estate rather than the personal creditworthiness of the borrower. While your credit score is still reviewed, the primary focus is the collateral.

Lenders in this space are typically private individuals or companies, not federally regulated banks. This lack of red tape allows for incredible flexibility. If you are looking at a distressed property in Detroit or a value-add multifamily building in Virginia, a hard money lender cares most about the "After Repair Value" (ARV) and your plan to execute the project.

You can learn more about how these differ from standard products by visiting our Mortgage Basics page.

The Superpower: Speed of Funding

In real estate investing, speed is often more valuable than a low interest rate. When a wholesaler in Birmingham, Alabama, sends out a "deal of the century" at 2:00 PM, it is usually under contract by 4:00 PM. Traditional banks simply cannot move that fast.

Closing in Days, Not Months

Hard money loans can often fund in as little as 5 to 10 days. Because the underwriting process is streamlined and focused on the property's equity, there is no need for the exhaustive documentation required by conventional lenders. You won't spend weeks digging up tax returns from three years ago or explaining a minor dip in your bank balance.

Competing with Cash Buyers

Using hard money effectively turns you into a cash buyer. Sellers love the certainty of a quick close. In competitive markets like Northern Virginia or the Florida coast, being able to guarantee a closing within two weeks gives you a massive advantage over buyers using traditional financing.

For a deeper look at how we move quickly, check out our loan process overview.

The Trade-Off: The High Cost of Capital

The speed and flexibility of hard money come with a premium price tag. You are essentially paying for the lender's risk and the convenience of rapid capital.

Higher Interest Rates

While a traditional mortgage might hover around 6% or 7% in the current market, hard money rates typically range from 10% to 15%. This might seem astronomical at first glance, but remember: these are short-term loans. You aren't supposed to keep this debt for 30 years.

Points and Fees

Most hard money lenders charge "points" at closing. One point equals 1% of the loan amount. It is common to see 2 to 4 points charged upfront. On a $200,000 loan, 3 points means $6,000 out of your pocket or equity on day one.

Short Repayment Windows

These loans usually have terms of 6 to 18 months. They are designed to get you through the purchase and renovation phase. If you don't sell or refinance within that window, you may face heavy extension fees or even foreclosure.

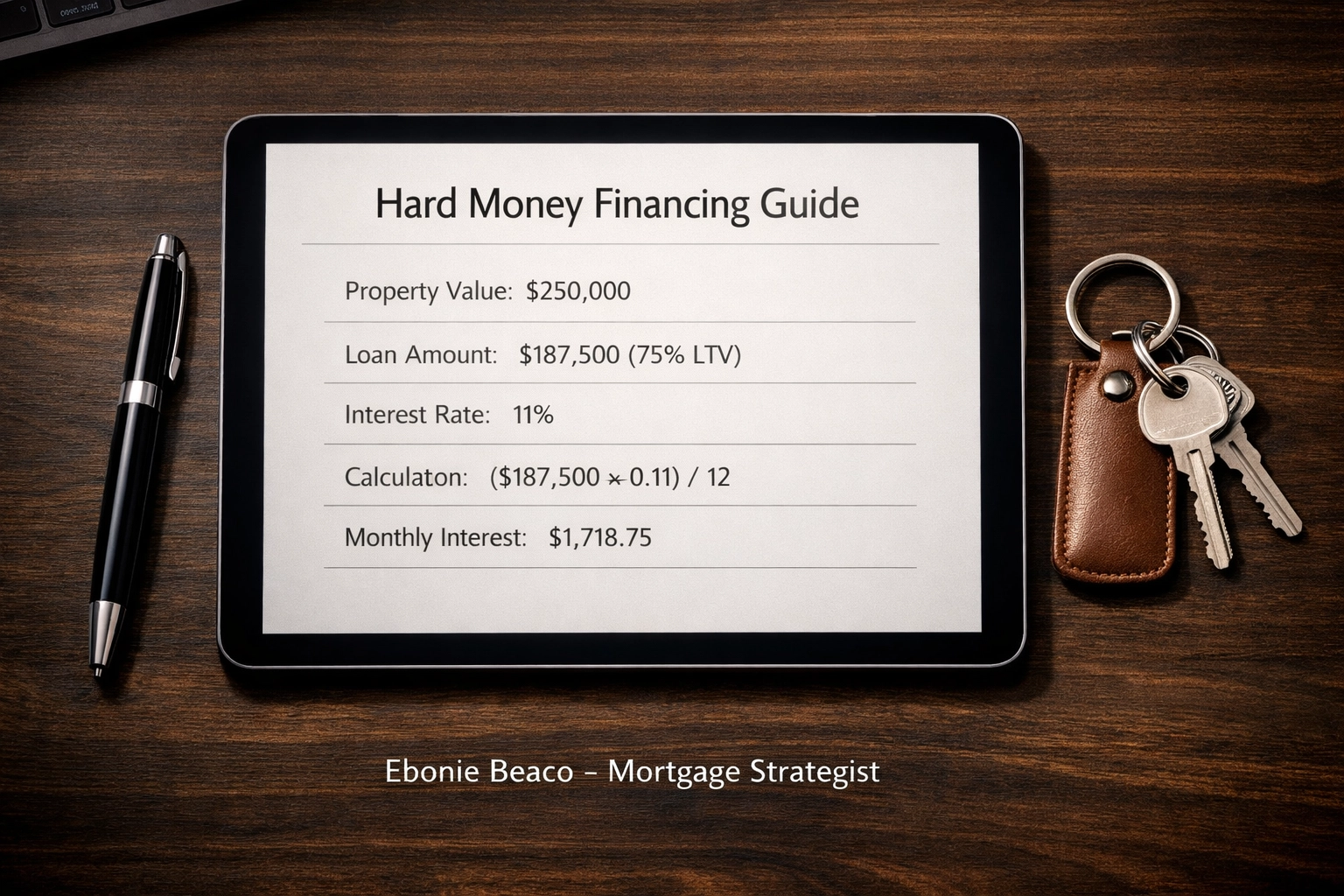

Instruction: Create an image titled "Hard Money Financing Guide". The image should show a clear calculation table. Property Value: $250,000. Loan Amount: $187,500 (75% LTV). Interest Rate: 11%. Calculation: ($187,500 x 0.11) / 12 months = $1,718.75 monthly interest-only payment. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. No money or cash images.

Instruction: Create an image titled "Hard Money Financing Guide". The image should show a clear calculation table. Property Value: $250,000. Loan Amount: $187,500 (75% LTV). Interest Rate: 11%. Calculation: ($187,500 x 0.11) / 12 months = $1,718.75 monthly interest-only payment. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. No money or cash images.

Breaking Down the Math: An Interest-Only Example

Most hard money loans are structured as interest-only payments. This helps keep your monthly overhead lower while you are busy managing contractors and permits.

Let’s look at a real-world scenario. Imagine you find a distressed property in Indianapolis for $150,000 that needs $50,000 in work. A hard money lender agrees to fund $160,000 of the project.

The Calculation:

- Loan Amount: $160,000

- Annual Interest Rate: 12%

- Annual Interest Cost: $160,000 x 0.12 = $19,200

- Monthly Interest Payment: $19,200 / 12 = $1,600

In this scenario, you are paying $1,600 a month to "rent" the $160,000. If your renovation takes four months and you sell the property in month five, your total interest cost was $8,000. If you make a $40,000 profit on the flip, that $8,000 was simply a necessary cost of doing business.

You can use our mortgage calculators to run different scenarios for your own deals.

Who Should Use Hard Money?

Hard money isn't for everyone. If you are buying a primary residence in a quiet suburb of St. Louis, you should stick to traditional financing. However, for the following groups, hard money is an essential tool:

- Fix-and-Flip Investors: Those buying distressed homes in places like Chicago or Atlanta who need to renovate and sell quickly.

- BRRRR Method Investors: Buy, Rehab, Rent, Refinance, Repeat. Hard money covers the "Buy" and "Rehab" phases before you move into a long-term DSCR loan.

- Real Estate Wholesalers: Sometimes wholesalers need to "double close" on a property. Hard money (specifically transactional funding) makes this possible.

- Borrowers with Credit Challenges: If you have a recent foreclosure or bankruptcy but found a killer deal in Florida, a hard money lender will often look past your credit score if the equity is there.

The Risks: What You Need to Know

Transparency is key in this industry. Hard money carries risks that you must manage.

The Balloon Payment

Most of these loans do not amortize. This means your monthly payments only cover the interest. At the end of the term, the entire original loan balance is due in one "balloon" payment. You must have an exit strategy: either selling the property or refinancing into a traditional or DSCR loan.

Lower Loan-to-Value (LTV)

Banks might give you 95% or 97% financing for a home. Hard money lenders rarely go above 75% or 80% of the purchase price or ARV. You will need to bring some of your own skin into the game.

The "Hold" Cost

Every day you own a property financed with hard money, it is costing you. Delays in permits or contractor issues can quickly eat into your profit margins. Efficiency is your best friend when using private capital.

Geographic Market Nuances

The way hard money is utilized varies by region.

- In Florida and Georgia: The market is highly competitive. Speed is the primary reason investors use hard money here to beat out out-of-state buyers.

- In Michigan and Indiana: Purchase prices are often lower, making the "points" and fees a larger percentage of the deal. Investors here have to be very precise with their math to ensure profitability.

- In California: The high property values mean the interest-only payments are significant. Investors often use bridge loans to stay liquid while waiting for high-end flips to sell.

If you have questions about how these loans apply to your specific state, feel free to check our contact page.

Transitioning from Hard Money to Long-Term Wealth

The most successful investors use hard money as a bridge, not a destination. Once the property is renovated and a tenant is in place, they refinance out of the high-interest hard money loan and into a long-term Landlord Loan or DSCR (Debt Service Coverage Ratio) loan.

This strategy allows you to pull your initial capital back out and move on to the next deal while securing a lower, fixed interest rate for the long haul. You can explore home refinance options to see how the transition works.

Final Thoughts on Speed vs. Cost

Hard money is expensive, but the cost of a missed opportunity is often higher. If a loan costs you $10,000 in interest but allows you to make $50,000 in profit on a deal you otherwise couldn't fund, the choice is clear.

Be honest about your timeline, be precise with your renovation budget, and always have a "Plan B" for your exit strategy. When used correctly, hard money is the ultimate accelerant for your real estate portfolio.

Need quick cash for a deal? Contact Ebonie Beaco for hard money financing and mentoring.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664