The Simple Trick to Fund Your Renovation Right Now Without Losing Your Low Mortgage Rate

You are sitting on a goldmine, but you feel like you can’t touch it.

If you bought or refinanced your home between 2020 and 2022, you likely have a mortgage rate somewhere between 2.5% and 3.5%. That is essentially "free money" by today's standards. However, your kitchen is dated, your primary bathroom needs a refresh, or maybe you need that basement finished for a growing family.

The dilemma is real: Do you refinance your entire mortgage to get cash out for renovations and jump your interest rate up to 6.5% or 7%?

The answer is a loud "No."

There is a simple trick that savvy homeowners in Indiana, Kentucky, and across the Southeast are using to unlock their equity without disturbing their low-interest primary mortgage. It is the strategy of using a Home Equity Line of Credit (HELOC) or a Closed-End Home Equity Loan.

The Problem With the Traditional Cash-Out Refinance

For years, the standard way to get money for a home project was a cash-out refinance.

Cash-Out Refinance: A new mortgage that replaces your current one for a higher amount than you owe, with the difference paid to you in cash.

Practical Application: You trade your old loan for a brand-new one at current market rates.

In a low-rate environment, this makes sense. But in today’s market, if you have a $300,000 mortgage at 3% and you need $50,000 for renovations, a cash-out refinance would force your entire $350,000 balance into a 7% rate. The increased interest cost on the original $300,000 would be massive. This is why many homeowners feel "locked in" to their current homes, even if those homes no longer fit their needs.

The "Simple Trick": The HELOC Strategy

The trick is to leave your first mortgage alone. Keep that 3% rate. Instead, you layer a second loan on top of it. This is where a HELOC becomes your best friend.

HELOC (Home Equity Line of Credit): A revolving line of credit, similar to a credit card, secured by the equity in your home.

Practical Application: You only borrow what you need, when you need it, and you only pay interest on the amount you actually spend.

As a leading Indiana HELOC lender, we see homeowners using this tool to fund renovations in stages. If you are doing a $60,000 kitchen remodel that takes six months, you don’t need the full $60,000 on day one. With a HELOC, you can draw $10,000 for demolition, then $20,000 for cabinets later, keeping your interest payments as low as possible during the construction phase.

Why This Strategy Is Winning in 2026

Home values across Alabama, Arkansas, Florida, Georgia, Illinois, Michigan, Missouri, and Virginia have seen significant growth over the last few years. This means you likely have more equity than you realize.

When you work with a Kentucky HELOC lender, you are looking at your "Combined Loan-to-Value" or CLTV.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property (first mortgage + HELOC) compared to the home’s appraised value.

Practical Application: Lenders typically allow you to go up to 80% or 85% CLTV, giving you access to a large pool of cash while keeping your primary low-rate loan intact.

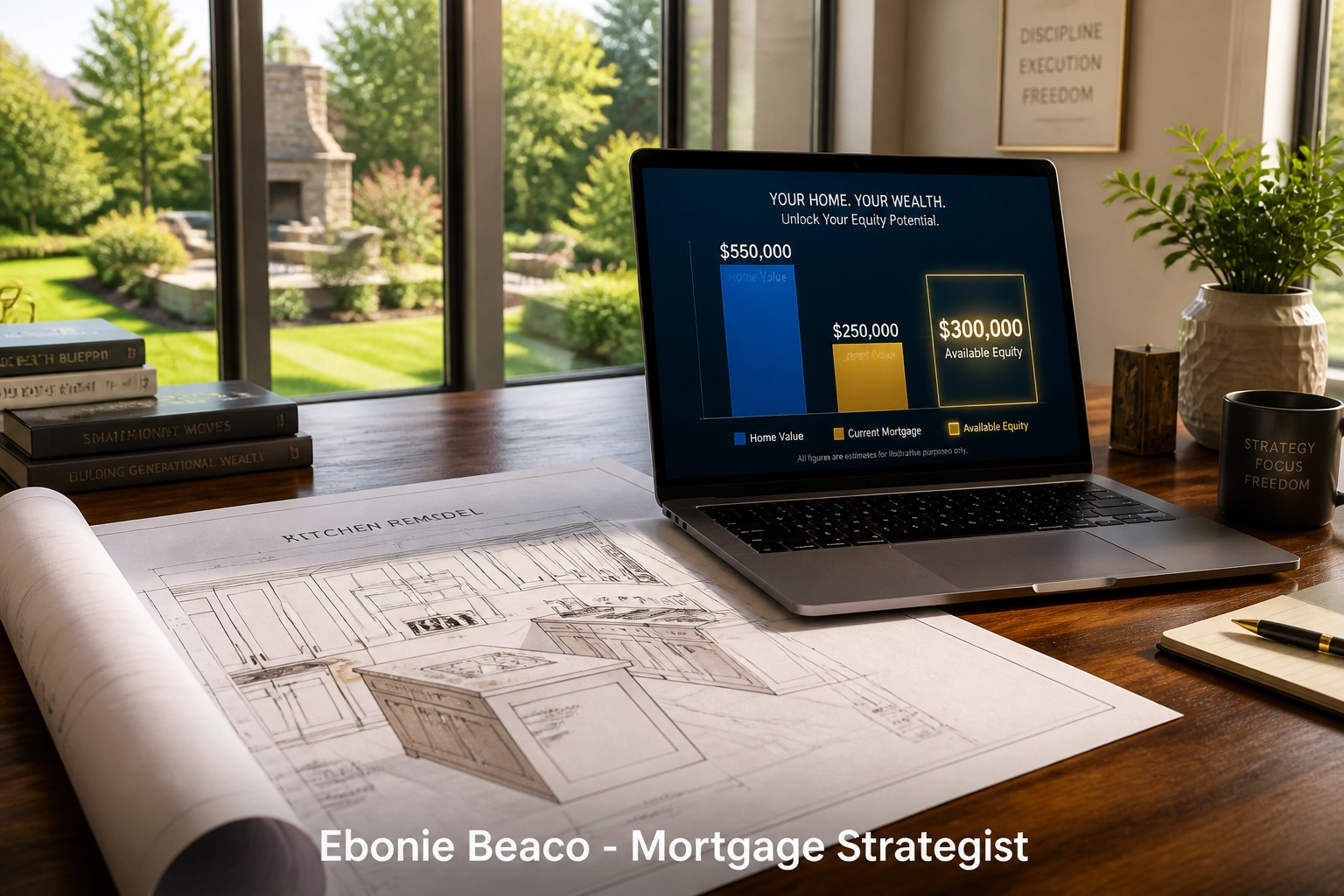

Let’s Look at the Numbers (A Real Scenario)

Imagine you own a home in a suburb like Carmel, Indiana, or Louisville, Kentucky.

- Current Home Value: $500,000

- Current Mortgage Balance: $280,000 (at 3.25%)

- Max CLTV (85%): $425,000

- Available Equity for a HELOC: $145,000

In this scenario, you could open a HELOC for $100,000. Your original $280,000 mortgage stays exactly where it is: at that beautiful 3.25% rate. You now have a $100,000 credit line available for your renovation. If you spend $50,000 on the project, you only owe interest on that $50,000.

Comparing Your Options: HELOC vs. Closed-End Home Equity Loan

While the HELOC is the most flexible, some homeowners prefer the "Closed-End" version.

Closed-End Home Equity Loan: A second mortgage that provides a one-time lump sum of cash with a fixed interest rate and set monthly payments.

Practical Application: Best for homeowners who know exactly how much their renovation will cost and want the stability of a fixed payment.

If you are the type of person who wants to know exactly what your bill will be every month for the next ten years, the closed-end loan is the way to go. If you want flexibility and the ability to reuse the credit line as you pay it down, the HELOC is the winner.

Explore our mortgage calculators to see how these different payments might look for your specific budget.

Regional Benefits for Homeowners

Home Loans Network serves a wide range of markets, and the renovation trend is hitting each one differently:

- Indiana & Kentucky: We are seeing a surge in "basement transformations" and outdoor living spaces. As a specialized Indiana HELOC lender and Kentucky HELOC lender, we help residents navigate local appraisal trends to maximize their draw amount.

- Florida & Georgia: With the influx of new residents, older homes are being gutted and modernized. Using equity for these upgrades often results in a massive jump in property value.

- Virginia & Maryland: High property values in the D.C. metro area mean even a small percentage of equity can equate to a six-figure renovation budget.

- Illinois & Michigan: Strategic renovations in markets like Chicago or Detroit are helping homeowners build long-term wealth by staying in their homes longer while enjoying modern amenities.

The Step-by-Step Process to Renovation Funding

- Check Your Equity: You can start by looking at recent sales in your neighborhood or using our online forms to get a preliminary idea of your home's current value.

- Determine Your Budget: Get quotes from contractors. Always add a 10-15% buffer for the "surprises" that come with older homes.

- Consult a Mortgage Strategist: This is where we come in. We don't just "give you a loan." We look at your total financial picture. If you have high-interest credit card debt, we might suggest a HELOC large enough to fund the renovation and wipe out those 24% interest rate cards.

- The Appraisal: The lender will need to verify the value of your home. You can learn more about this process on our appraisals info page.

- Access Your Funds: Once approved, your HELOC functions like a checking account. You can write checks or transfer funds directly to your contractor.

Common Misconceptions About HELOCs

Some people worry that having a second mortgage is "risky." However, when used for home improvements, you aren't just spending money: you are reinvesting it into your most significant asset.

Another common fear is the variable interest rate. While HELOC rates can fluctuate, many programs offer a "Fixed-Rate Lock" option. This allows you to draw a chunk of money and lock it into a fixed rate for a set period, giving you the best of both worlds: flexibility and predictability.

If you are worried about the technicalities, jump in and read our FAQ for quick answers to the most common equity questions.

Why Now Is the Time to Act

Wait times for contractors are beginning to stabilize, and home values remain strong in our core states of AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA. By securing your financing now, you position yourself to finish your projects before the next seasonal rush.

Don't let your low mortgage rate stop you from living in the home you actually want. You worked hard to get that 3% rate: don't give it up. Use the equity you've built to create the space you've been dreaming of.

Whether you are looking for an Indiana HELOC lender to fix up a classic home in Indianapolis or a Kentucky HELOC lender for a ranch in Lexington, the strategy remains the same: Keep the first, leverage the second, and build your wealth.

Access your home's hidden potential today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664