The Paperwork Problem: What Contract Should You Actually Use for Wholesaling?

Navigating the legal landscape of wholesale real estate requires more than just a firm handshake and a motivated seller; it requires a robust, legally binding document that protects your interests while facilitating a smooth transaction. When you are wholesaling houses, you are not technically selling the physical property itself but rather the rights to a purchase agreement, which makes the specific language within that agreement absolutely critical for your success. Many new participants in real estate investing mistakenly believe that any standard purchase and sale agreement will suffice, yet these generic forms often lack the essential "and/or assigns" language that allows you to transfer your equitable interest to cash buyers. To maintain transparency throughout the process, you must ensure your contracts clearly outline your role as the principal buyer who intends to assign the contract for a fee. You can explore more about foundational concepts in our mortgage basics section to understand how these legal structures interact with broader property finance.

The most common instrument used in this industry is the Assignment of Contract, a streamlined method where you sign a purchase agreement with a seller and then legally transfer those rights to an end investor. For this to work effectively in off-market deals, the original contract must be fully assignable and include a specific clause stating that the buyer has the right to assign their position without further consent from the seller. You should also be mindful of the Earnest Money Deposit (EMD), which acts as a good-faith showing of intent and is typically held by a neutral third-party title company or attorney. In many scenarios, a wholesaler will use a simple one or two-page assignment addendum that identifies the original contract, the new buyer, and the assignment fee being paid for the right to step into the deal. Understanding the loan process is helpful here because your end buyer will often be using specialized financing like fix and flip loans or hard money to satisfy the purchase.

When profits on a single deal are significantly high or when a seller is uncomfortable with an assignment, a Double Closing, also known as a simultaneous closing, becomes the preferred alternative. This strategy involves two distinct transactions where you purchase the property from the seller (the A-to-B transaction) and immediately sell it to your end buyer (the B-to-C transaction) on the same day. This method requires two separate sets of contracts and usually involves transactional funding to cover the purchase price of the first leg of the deal. While this approach incurs double the closing costs, it provides the highest level of privacy regarding your profit margins and is often necessary when dealing with certain bank-owned properties or REOs. Investors frequently utilize home purchase resources to understand the closing mechanics required for these multi-stage settlements. By utilizing a double closing, you ensure that the end buyer does not see your specific fee, which can sometimes lead to friction during the final stages of a large transaction.

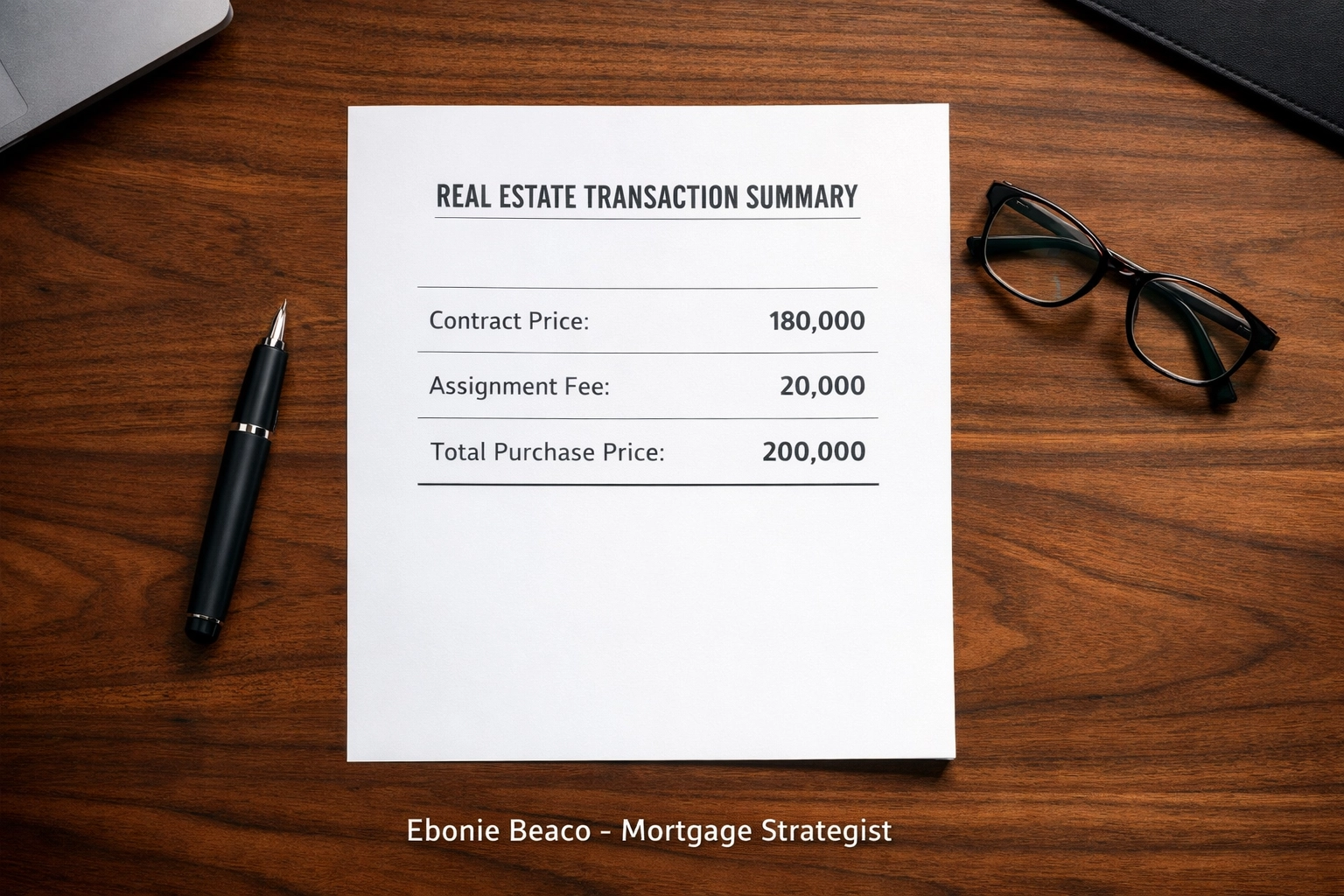

To illustrate how these figures translate into a real-world scenario, consider a typical wholesale deal breakdown in a market like Chicago or various cities in Florida. You might secure an off-market property under contract for a purchase price of $180,000 with a $2,000 earnest money deposit. After marketing the deal to your list of cash buyers, you find an investor willing to pay $200,000 for the property in its current condition. By using an assignment agreement, you would document an assignment fee of $20,000, which is paid to you by the end buyer at the time of closing. The final HUD-1 or settlement statement would show the $180,000 going to the original seller and the $20,000 assignment fee going to your business. This clear financial structure ensures that all parties are aware of the disbursement of funds while securing your profit for sourcing and vetting the investment opportunity.

Every wholesale contract must include an "as-is" clause to protect you from future liability regarding the physical condition of the property. Since wholesalers rarely perform renovations or even occupy the home, it is vital that the seller acknowledges the property is being sold without any warranties or guarantees. Furthermore, you should include a robust inspection contingency period that allows you a specific number of days to conduct due diligence and confirm the property's value with your contractors or partners. If the inspections reveal issues that make the deal unfeasible at the current price, this clause gives you the legal right to renegotiate or withdraw without losing your earnest money. Many seasoned investors refer to our FAQ to understand common hurdles encountered during the due diligence and financing phases of a deal. Ensuring these protections are in place prevents you from being forced into a purchase that does not meet your profit requirements.

Transparency is a core value at Home Loans Network, and this extends to how you handle title and escrow within your wholesaling contracts. You should always stipulate that the closing must occur at a title company or with a real estate attorney who is "investor-friendly" and understands the nuances of assignments and double closings. Not all title companies are equipped to handle these transactions, and using an inexperienced closer can lead to delays or even the collapse of your deal. Your contract should also specify that the buyer is responsible for obtaining a clear and marketable title, which protects the end investor and ensures the property can be refinanced or sold later. Investors looking to scale their portfolios often look into DSCR investor loans as a way to transition these wholesale acquisitions into long-term rental income. A clean title is the prerequisite for all such advanced financing strategies.

State-specific regulations in places like Illinois, Virginia, and California may require specific disclosures or even a real estate license if you engage in a certain number of transactions per year. For example, some jurisdictions have very strict rules regarding how you can market a contract, and failing to follow these guidelines can result in heavy fines or legal challenges. It is always advisable to have your specific contract templates reviewed by a local real estate attorney to ensure compliance with the latest state statutes. You can select a loan officer on our team to discuss how local market trends are impacting the types of deals currently being funded in your area. Staying informed on these regional shifts allows you to adapt your paperwork to remain both competitive and legally compliant.

Ultimately, the contract you choose to use is the blueprint for your entire business operation and should be treated with the highest level of professionalism. Whether you are using a standard state-approved form with an assignment addendum or a custom-drafted attorney agreement, the goal remains the same: clarity and protection for all parties involved. As you grow your real estate investing business, you will find that having a predictable and repeatable paperwork process allows you to close deals faster and build stronger relationships with your cash buyers. We invite you to contact us to explore how our various loan programs can support the end buyers in your wholesale network. By mastering the art of the contract, you position yourself as a sophisticated strategist in the ever-evolving world of real estate finance.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664