The Investor’s Guide to Analyzing a Rental Property in 5 Minutes

Speed is a competitive advantage in the current real estate market. Whether you are looking at a duplex in Chicago, a single-family rental in Tampa, or a portfolio in Birmingham, the ability to filter out bad deals quickly is essential. You do not want to spend hours on a deep-dive analysis only to find out the property will not even break even.

This guide provides a structured framework to help you evaluate potential investments in minutes. By using simple screening rules and key financial metrics, you can identify which properties deserve a closer look and which ones you should pass on immediately.

The Power of Quick Screening Rules

When you first see a listing, your goal is not to calculate every penny. Your goal is to see if the property has the potential to produce income. Experienced investors in high-growth states like Florida, Georgia, and Virginia often use "rules of thumb" to narrow their search.

The 1% Rule The 1% rule is a baseline screening tool. It suggests that a property should rent for at least 1% of its total acquisition cost (purchase price plus immediate repairs).

Calculation: If a house in Indianapolis costs $200,000, it needs to rent for $2,000 per month to meet the 1% rule.

If the market rent in that area is only $1,400, the property fails the 1% rule. This does not mean it is a bad investment, but it indicates that achieving high monthly cash flow will be a challenge. You can learn more about different property types and their typical returns at https://www.homeloansnetwork.com/mortgage-basics.

The 2% Rule In lower-priced markets or distressed areas, some investors aim for the 2% rule. This is much harder to find in current market conditions but is often sought by those looking for extreme cash flow.

Calculation: A $100,000 property would need to generate $2,000 in monthly rent.

While these rules are helpful, they do not account for expenses like property taxes or insurance, which varies significantly between a state like Illinois and a state like Arkansas. This is why you must move to deeper metrics once a property passes the initial screen.

Understanding Net Operating Income (NOI)

Once a property passes the 1% test, you need to look at the Net Operating Income (NOI). This figure tells you how much income the property generates after all operating expenses are paid, but before you pay your mortgage.

Operating Expenses Operating expenses include:

- Property taxes

- Homeowners insurance

- Maintenance and repairs

- Property management fees

- Utilities (if paid by the landlord)

- Landscaping or snow removal

Calculation: Total Rental Income - Total Operating Expenses = NOI.

NOI is a vital figure because it helps you calculate the Cap Rate, which allows you to compare different properties regardless of how they are financed. You can find answers to common questions about expenses and income at https://www.homeloansnetwork.com/faq.

The Capitalization Rate (Cap Rate)

The Cap Rate is the rate of return on a real estate investment property based on the income that the property is expected to generate. It is used to estimate the investor's potential return on their investment.

Calculation: (NOI / Current Market Value) x 100 = Cap Rate.

For example, if a property in Virginia Beach has an NOI of $15,000 and is valued at $250,000, the Cap Rate is 6%.

In many markets, a Cap Rate between 5% and 10% is considered healthy. However, in high-demand areas like Southern California, Cap Rates may be lower because investors expect higher appreciation over time.

Analyzing Monthly Cash Flow

Cash flow is the most important metric for many landlords. It is the money that actually lands in your bank account at the end of every month. Unlike NOI, cash flow includes your debt service (mortgage payment).

To get an accurate cash flow projection, you need to know your financing terms. Many investors today use DSCR Investor Loans (Debt Service Coverage Ratio). These loans focus on the property's ability to cover the mortgage with its own rental income rather than relying solely on your personal income or tax returns.

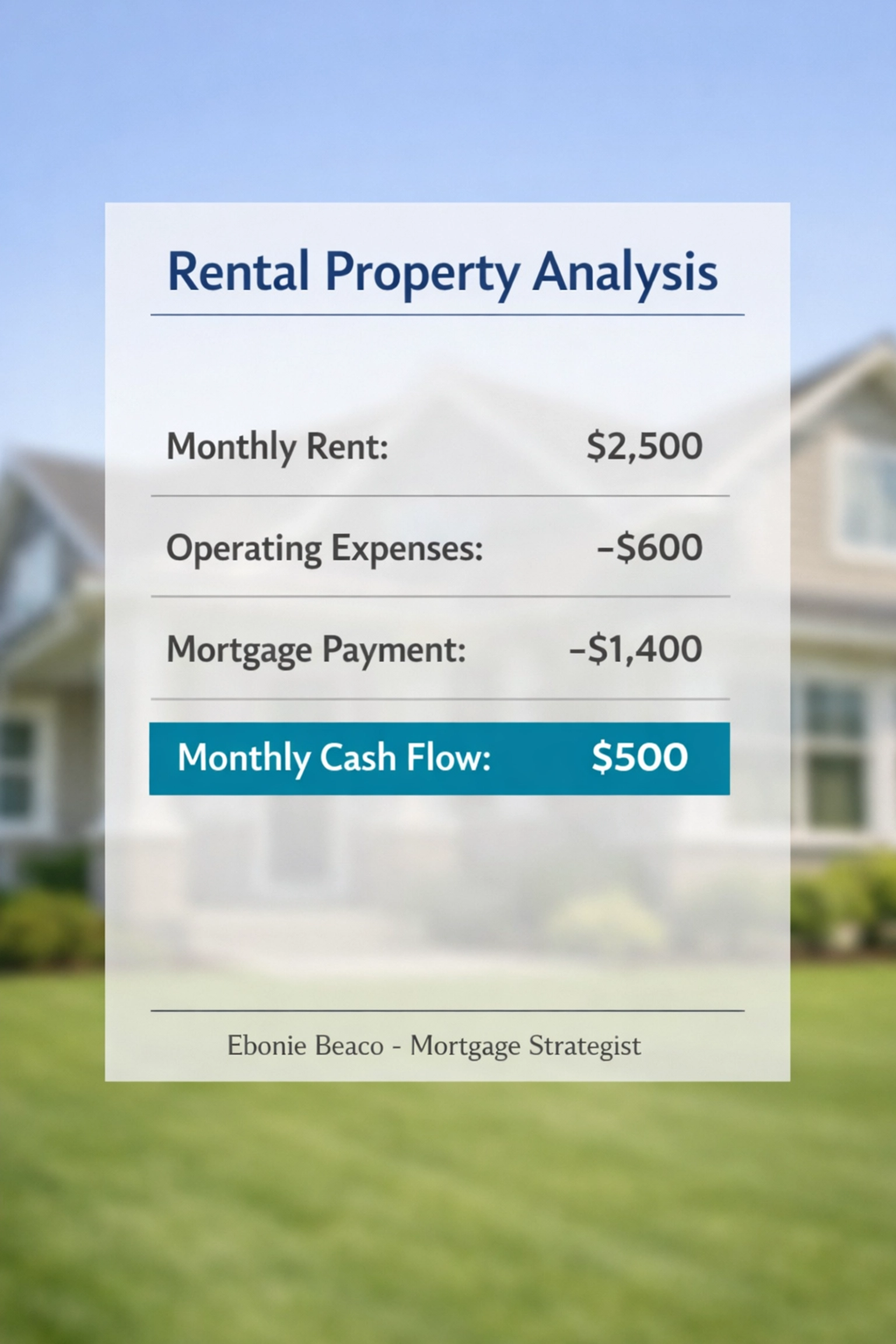

Let’s look at a real-world example of a rental property analysis for a home in a mid-sized market.

Monthly Cash Flow Calculation Example:

- Purchase Price: $250,000

- Monthly Rental Income: $2,500

- Operating Expenses: $600 (Taxes, Insurance, Repairs, Vacancy)

- Monthly Mortgage Payment (P&I): $1,400

- Total Monthly Outflow: $2,000 ($600 + $1,400)

- Monthly Cash Flow: $500

Visual Breakdown: Rental Property Analysis Table. Shows Gross Rent ($2,500) minus Expenses ($600) and Mortgage ($1,400) resulting in Monthly Cash Flow ($500). Title: "Rental Property Analysis". Bottom text: "Ebonie Beaco - Mortgage Loan Officer". No money or cash icons.

Visual Breakdown: Rental Property Analysis Table. Shows Gross Rent ($2,500) minus Expenses ($600) and Mortgage ($1,400) resulting in Monthly Cash Flow ($500). Title: "Rental Property Analysis". Bottom text: "Ebonie Beaco - Mortgage Loan Officer". No money or cash icons.

This $500 per month is your "mailbox money." If you are planning to scale a portfolio, understanding how your loan structure impacts this number is critical. You can explore different loan options and their impacts using the tools at https://www.homeloansnetwork.com/mortgage-calculators.

The 3-3-3 Rule for Market Analysis

If the numbers look good, spend the remaining few minutes of your five-minute analysis looking at the market trends. The 3-3-3 rule is a quick way to gauge the area's potential.

- 3 Years of Price Trends: Has the neighborhood seen steady growth over the last three years?

- 3 Future Years of Development: Are there new hospitals, schools, or tech hubs being built nearby?

- 3 Comparable Properties: Find three similar homes nearby that have sold or rented recently to confirm your estimates.

Analyzing markets like Atlanta or the suburbs of Chicago requires looking at local employment centers. Proximity to major transit and jobs is a huge factor in long-term vacancy rates. You can see how our clients have navigated these markets at https://www.homeloansnetwork.com/testimonials.

Financing Strategies for Modern Investors

Understanding how to analyze a deal is only half the battle. The other half is knowing how to fund it. Depending on your goals, you might use different strategies:

DSCR Loans These are excellent for landlords who want to scale quickly. Lenders look at the property’s rental income to ensure it covers the mortgage payment. This is a common choice for investors in California and Florida where property values are high.

Cash-Out Refinance If you already own a home with significant equity, a Cash-Out Refinance can provide the down payment for your next rental property. This is a popular way for current homeowners to transition into real estate investing. Learn more about the refinance process at https://www.homeloansnetwork.com/home-refinance.

Fix and Flip Loans For investors who prefer to buy distressed properties, renovate them, and sell them quickly, Fix and Flip Financing or Bridge Loans provide the necessary short-term capital. These loans often cover both the purchase price and the renovation costs.

Due Diligence and Physical Inspection

While you can run the numbers in five minutes, you should never skip the physical due diligence once a property is under contract. Check the age of the roof, the condition of the HVAC system, and any signs of foundation issues.

A $10,000 unexpected repair can wipe out two years of cash flow instantly. Always factor in a "Capital Expenditures" (CapEx) reserve in your long-term budget. This is money set aside specifically for big-ticket items that will eventually need replacement.

Putting It All Together

Analyzing a rental property does not have to be an overwhelming process. By following these steps, you can quickly determine if a deal is worth your time:

- Apply the 1% Rule for a quick sanity check.

- Calculate the NOI to see the property's raw earning power.

- Determine the Cash Flow based on current mortgage rates and loan programs like Non-QM Mortgage Loans.

- Assess the location using the 3-3-3 Rule.

If the property yields a positive monthly cash flow and sits in a growth market, it is time to take the next step. If you are a first-time investor, consider reviewing the steps of the loan process at https://www.homeloansnetwork.com/loan-process to see how to move from analysis to ownership.

Investing in real estate is one of the most proven ways to build wealth, but it requires a disciplined approach to the numbers. Whether you are looking for your first rental in Michigan or your tenth in Georgia, staying objective is your greatest asset.

Need help analyzing your next deal? Contact Ebonie Beaco for mentoring and financing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664