The Illinois Inventory Paradox: Why 5.6% More Homes Doesn't Mean Lower Prices

Today is Wednesday, March 25, 2026. If you have been tracking the headlines lately, you might have noticed a specific number circulating through the national housing discourse: 5.6%. According to recent data, national housing inventory has seen a 5.6% year-over-year growth. On the surface, this sounds like a win for buyers and a cooling signal for a white-hot market.

However, as a mortgage strategist, I look beyond the surface level percentages. In Illinois, and specifically across the Chicago metropolitan area, this 5.6% increase is not the "inventory surge" many were hoping for. Instead, we are witnessing an inventory paradox.

The numbers are rising, but the options for high-quality, move-in-ready homes remain scarce. Prices remain high. Competition for well-priced assets remains fierce. Understanding why this is happening is the key to navigating the Illinois market as a Realtor, investor, or homeowner in 2026.

Understanding the Stagnation Trap

To understand the paradox, we must define the source of this "new" inventory.

Inventory Stagnation: This is a phenomenon where active listings increase not because of a wave of new homes entering the market, but because existing listings fail to sell and remain on the market for extended periods.

In a healthy market, inventory grows because of "new flow": more sellers putting signs in their yards. In the current Illinois climate, much of that 5.6% growth is coming from "stale flow." These are properties that are overpriced, in need of significant renovation, or stuck with sellers who are unwilling to accept the current reality of mortgage rates.

According to recent reports on the spring housing market and mortgage rates, rates are still exerting a heavy "lock-in" effect on potential sellers. Most Illinois homeowners are sitting on sub-4% rates. They aren't going to move unless they absolutely have to, which keeps the supply of "prime" homes at a historic low.

Realistic urban Chicago street view. Ebonie Beaco - Mortgage Strategist

The Seller Surplus Gap in Illinois

One of the primary reasons prices aren't dropping despite more homes being "available" is the Seller Surplus Gap.

Seller Surplus Gap: The percentage difference between the price a seller expects to receive and the price a buyer is actually willing or able to pay based on current financing costs.

In the Chicago market, this gap has hovered around 35.2% recently. Sellers have spent the last several years watching their equity explode. They have a specific number in their head. Buyers, meanwhile, are looking at their monthly debt-to-income (DTI) ratios and realizing they cannot afford those legacy prices at today’s rates.

Debt-to-Income (DTI) Ratio: A personal financial measure that compares an individual's monthly debt payments to their monthly gross income.

When the Seller Surplus Gap is high, homes sit. They contribute to the "5.6% growth" in inventory, but they don't contribute to a drop in price because the sellers are often willing to wait rather than take a haircut on their equity.

Why Illinois Prices Remain "Sticky"

If you are a Realtor or a wholesaler in Illinois, you know that "sticky prices" are the biggest hurdle to closing deals right now. Price stickiness occurs when prices do not adjust downward quickly, even when demand cools or supply increases.

Illinois has a unique set of challenges contributing to this:

When you are starting from such a deep deficit, a 5.6% increase is a drop in the bucket. It is like trying to fill a swimming pool with a garden hose while the drain is half-open. It doesn't create a buyer's market; it just creates a slightly less frantic seller's market.

Realistic suburban Illinois neighborhood. Ebonie Beaco - Mortgage Strategist

Strategic Financing for a Paradoxical Market

As a mortgage strategist, I work with investors and homeowners to find the path forward when the traditional "buy low, sell high" playbook feels broken. If you are a Real Estate Investor or a Wholesaler in Illinois, Alabama, or Florida, you need to look at non-traditional financing to bridge the gap between high prices and buyer affordability.

DSCR Loans for Landlords

If you are looking to acquire one of these "stagnant" properties that has been sitting on the market, a DSCR loan might be your strongest tool.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage program for investment properties that qualifies the borrower based on the property’s rental income rather than the borrower’s personal income or employment history.

Practical Application: If a property is sitting because a traditional buyer can't qualify due to their personal DTI, an investor can step in. If the projected rent covers the mortgage payment (a ratio of 1.0 or higher), the deal can close. This is a primary strategy for those building rental portfolios in Illinois and Georgia.

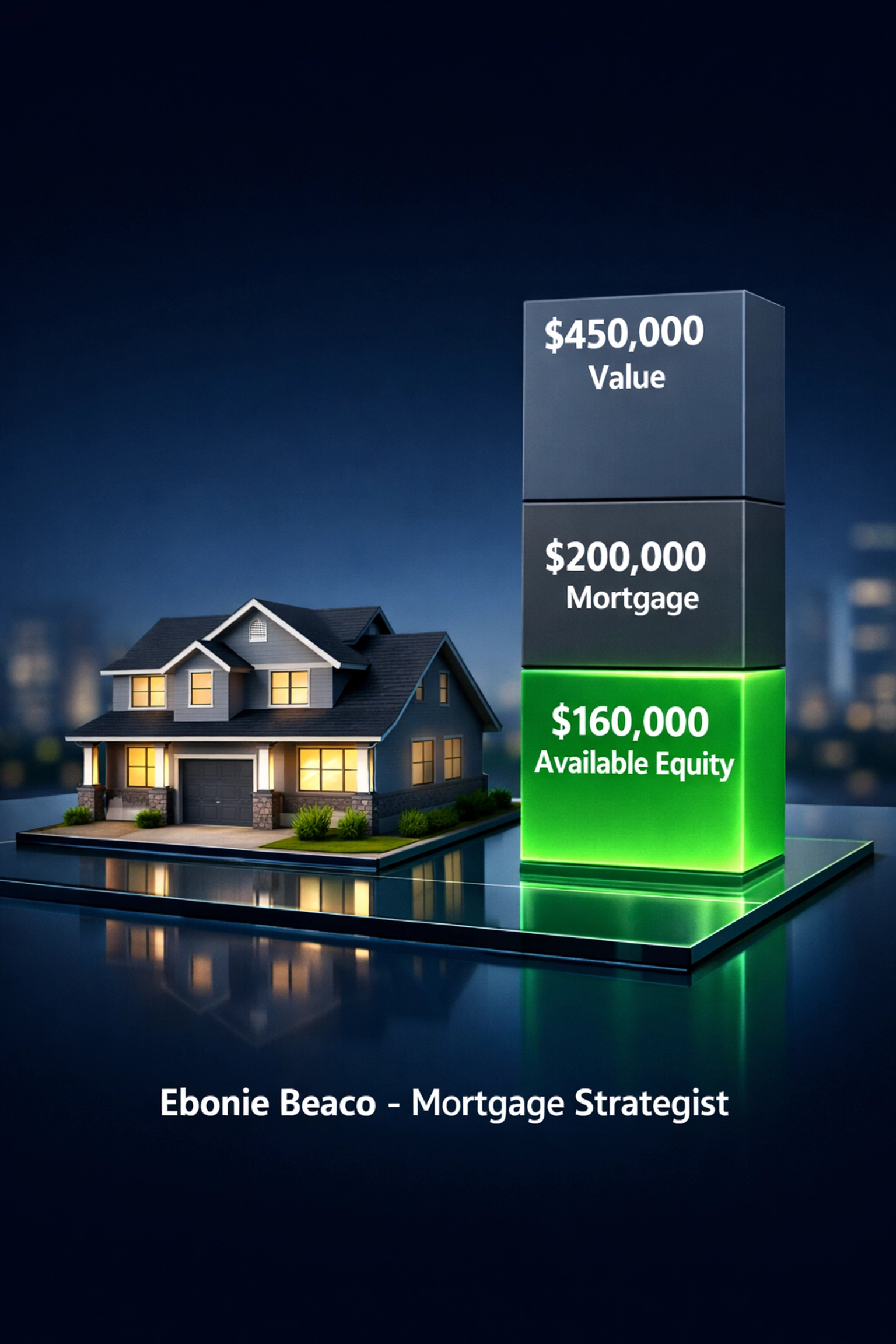

Cash-Out Refinance for Equity Access

For current homeowners in Illinois who are seeing their home values stay high despite the inventory creep, a cash out refinance is a way to leverage that "sticky" equity.

Cash-Out Refinance: A refinancing of an existing mortgage where the new mortgage loan is for a larger amount than the current loan, and the borrower gets the difference in a lump sum of cash.

Example:

This liquidity can be used to fund a fix and flip project or to purchase a short-term rental in high-demand markets like Michigan or Virginia.

Professional financial chart showing home equity calculations. Ebonie Beaco - Mortgage Strategist

Guidance for Illinois Realtors and Wholesalers

If you are representing sellers whose homes are contributing to the "stagnation" statistics, it is time to change the conversation. You aren't just selling a house; you are selling a financing scenario.

When a property sits for more than 45 days in Illinois, it becomes a prime candidate for creative financing. Explore options like:

Non-QM Mortgage: A loan that does not follow the standard federally backed mortgage guidelines, allowing for more flexible qualification criteria.

The Regional Outlook: Beyond Illinois

While the Illinois inventory paradox is distinct, many of these trends are mirroring what I see in the other states where we provide strategic financing.

In Florida and Georgia, we see higher migration patterns, which keeps the demand side of the equation even more pressurized. In Michigan and Indiana, the price points are lower, but the inventory scarcity is just as real. In Virginia and Missouri, the Seller Surplus Gap is starting to narrow, but buyers still need authoritative guidance to structure winning offers.

Whether you are an investor in Alabama, a wholesaler in Arkansas, or a homeowner in Kentucky, the strategy remains the same: data-driven decision making. Do not let a single "inventory growth" headline dictate your moves. Look at the quality of the inventory, the days on market, and the available financing levers.

Moving Stagnant Inventory

The 5.6% growth we are seeing is an opportunity for those who know how to solve the puzzle. For investors, it means more "tired" listings and potentially more motivated sellers if you know how to structure the deal. For Realtors, it means you must become a student of mortgage strategy to keep your deals from falling apart at the finish line.

The Illinois market isn't crashing. It is recalibrating. The paradox of rising inventory and stable prices will likely continue through the rest of 2026.

Explore your options. Compare the math. Access the equity you have built. If you are ready to navigate these numbers with a strategist who understands the local nuances of Illinois and the broader Southeast and Midwest markets, let's look at your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Providing strategic financing in AL, AR, CA, GA, FL, IL, IN, MI,MO, KY, MO, VA.