The Hidden Opportunity in Stagnant Prices: A Guide for Kentucky First-Time Buyers

Current market conditions in March 2026 present a unique paradox for the Kentucky housing landscape. While headline mortgage rates hover around the 6% mark, a critical shift has occurred in property valuations. Home price growth in Kentucky has cooled to a mere 0.9% year-over-year.

For the casual observer, 6% interest rates appear to be a barrier. For the strategic buyer, this stagnation in home prices represents an asymmetric advantage. When price appreciation slows to nearly zero, the frenzied bidding wars that defined the early 2020s vanish. This creates a window where buyers can negotiate terms, request seller concessions, and utilize specialized grant programs without the pressure of competing against twenty other offers.

Understanding the Asymmetric Advantage

In real estate finance, an asymmetric advantage refers to a situation where the potential upside of a transaction significantly outweighs the perceived risks or costs due to specific market imbalances.

In the current Kentucky market, high interest rates have sidelined the "emotional buyer." This leaves the field open for the "strategic buyer." You are no longer fighting over-ask prices. Instead, you are acquiring assets at stable valuations.

As noted in recent market analysis from Bankrate, while rates fluctuate, the stabilization of home prices is the real story for 2026. This stability allows you to plan your entry with precision rather than desperation.

Description: A realistic, bright, and modern suburban home interior with clean lines and natural light. Text overlay at the bottom: Ebonie Beaco - Mortgage Strategist

The $20,000 Catalyst: Welcome Home Grant Program

Timing is a core component of any mortgage strategy. On April 6, 2026, the Welcome Home Grant Program officially opens its doors. This is not just another loan; it is a significant capital injection for qualified buyers.

Welcome Home Grant: A specialized subsidy providing up to $20,000 in non-repayable funds to be used for down payments and closing costs.

Practical Application: This grant effectively eliminates the primary barrier to entry for many Kentucky residents, allowing you to preserve your personal liquidity while acquiring a primary residence.

Key details for the 2026 cycle:

- Grant Amount: Between $10,000 and $20,000.

- Accessibility: Funds are first-come, first-served. History suggests these funds are reserved within hours of the 8:00 a.m. ET launch.

- Eligibility: No first-time homebuyer requirement. Repeat buyers are welcome.

- Income Limit: Generally capped at 80% of the Area Median Income (AMI) by county.

- Requirement: A fully executed purchase contract must be in place before the funds are reserved.

If you are a homeowner in Kentucky or looking to move into the state from neighboring Illinois or Indiana, this grant is a cornerstone of a high-leverage entry strategy. Explore more about the loan process to ensure your file is ready before the April 6 deadline.

Analyzing the Numbers: A Strategy for First-Time Buyers

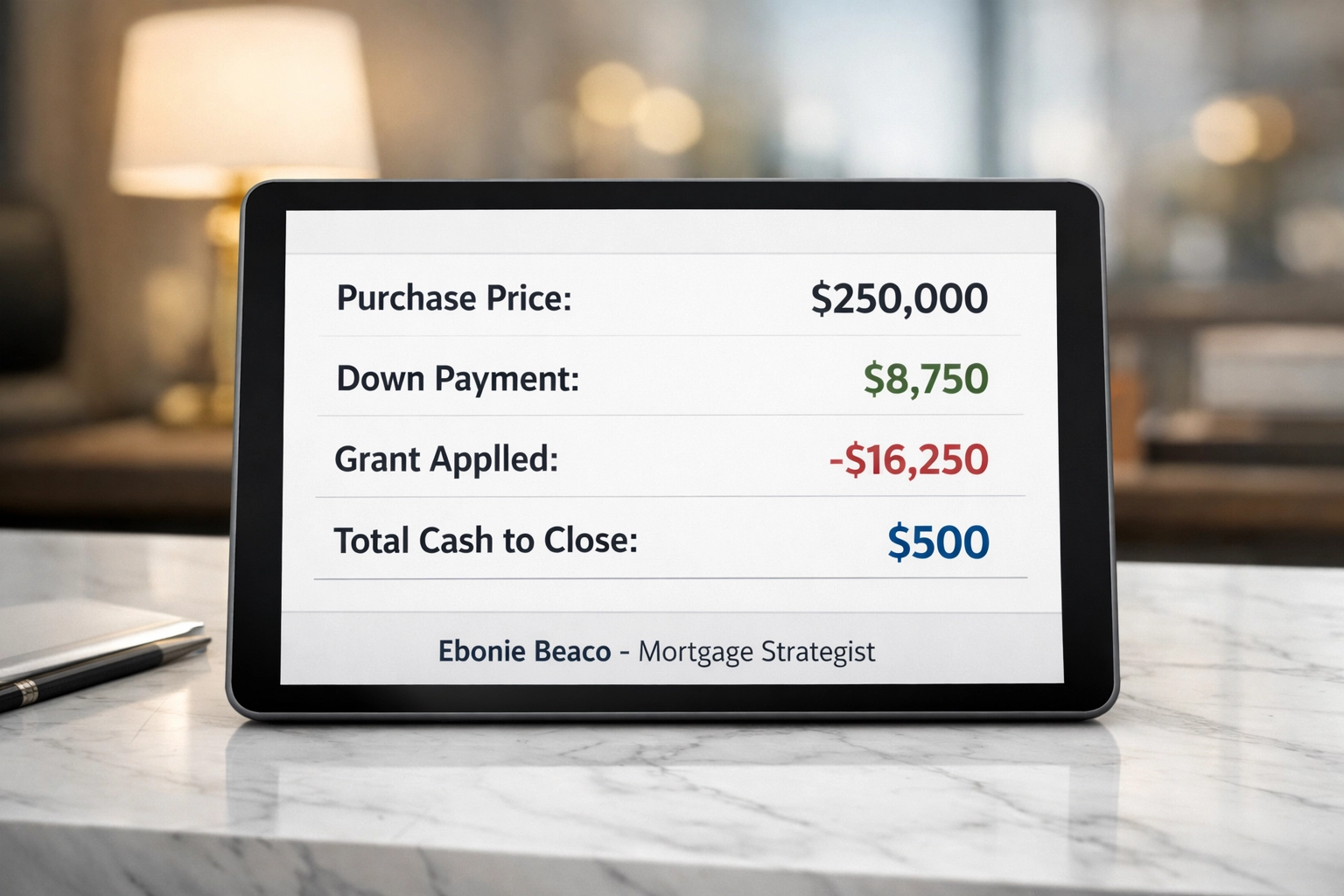

To understand how stagnant prices and high grants offset interest rates, let's look at a practical acquisition scenario.

Imagine you are purchasing a home in Lexington or Louisville for $250,000.

Scenario Breakdown:

- Purchase Price: $250,000

- Standard 3.5% Down Payment (FHA): $8,750

- Estimated Closing Costs: $7,500

- Total Cash Required: $16,250

- Welcome Home Grant Applied: -$16,250

- Out-of-Pocket Cost: $0 (Plus a required $500 borrower contribution per program rules).

In this scenario, the grant covers the entire entry cost. Even at a 6.5% interest rate, your "cash-on-cash" return is infinite because you have virtually no capital tied up in the initial acquisition. Compare this to 2022, when you might have had a 3% interest rate but had to pay $30,000 over the appraised value just to win the bid. Stagnant prices are your friend.

Description: A professional financial chart showing a deal breakdown: Purchase Price $250k, Down Payment $8,750, Grant -$16,250, Total Cash to Close $500. Text overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Leveraging Kentucky Housing Corporation (KHC) Programs

Beyond the temporary grants, the Kentucky Housing Corporation (KHC) provides year-round infrastructure for buyers. These programs are designed to lower the Monthly Debt-to-Income (DTI) ratio.

KHC Conventional Preferred: A mortgage product requiring only a 3% down payment and offering reduced Private Mortgage Insurance (PMI) rates.

Practical Application: By reducing the monthly PMI cost, you increase your purchasing power even if interest rates remain elevated.

KHC Secondary Funding: A down payment assistance loan of up to $12,500. This is structured as a second lien at a 4.75% interest rate over a 15-year term.

For residents in Missouri, Virginia, or Florida considering a move to Kentucky, these state-specific programs offer a level of support that is currently outperforming many other regions. You can review mortgage basics to see how these KHC tools compare to national standard products.

Strategic Guidance for Real Estate Investors and Wholesalers

If you are a Real Estate Investor or Wholesaler in Alabama, Georgia, or Michigan, the Kentucky market stagnation is a "buy" signal.

Wholesalers: Stagnant prices mean sellers are becoming more realistic. When houses sit on the market for 45 days instead of 4, sellers are more likely to entertain cash offers or creative financing structures.

Investors: Use DSCR (Debt Service Coverage Ratio) Loans to scale your portfolio.

Definition: A DSCR loan qualifies a borrower based on the cash flow of the property rather than personal income or tax returns.

Practical Application: In a market where prices aren't skyrocketing, you can accurately project your rental yields without fearing a sudden valuation bubble burst.

For those focusing on the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), the current lack of price growth means you must be diligent about your "After Repair Value" (ARV). However, it also means you aren't overpaying on the "Buy" phase. Access our mortgage calculators to run your numbers on potential rental acquisitions.

Government-Backed Safety Nets: FHA, VA, and USDA

While specialized Kentucky grants are powerful, the foundation of the industry remains government-backed lending.

- FHA Loans: Ideal for those with credit scores as low as 620 and a 3.5% down payment. In a stagnant price market, FHA buyers have more leverage to ask for "seller-paid closing costs."

- VA Loans: For veterans and active-duty members, the zero-down payment benefit remains the gold standard.

- USDA Loans: These are highly relevant in rural Kentucky. They offer 100% financing for properties located in designated rural areas.

Description: A realistic photo of a modern office desk with a laptop, a calculator, and a set of house keys, symbolizing a completed transaction. Text overlay at the bottom: Ebonie Beaco - Mortgage Strategist

Action Steps for the Kentucky Market

The window for the Welcome Home Grant is narrow. If you are a homeowner looking to upgrade or a first-time buyer ready to jump in, you must act with speed.

- Secure Pre-Approval: You cannot apply for grants without a verified pre-approval. Jump in and contact us to start your file.

- Identify Your Target Property: Work with your Realtor to find properties that have been on the market for 30+ days. This is where the most significant negotiation leverage exists.

- Execute the Contract: Ensure your purchase contract is signed and ready for submission before the April 6 deadline.

- Evaluate Your Equity: If you already own a home in Virginia, Florida, or Illinois and are looking to relocate, consider a cash-out refinance to fund your next move or investment.

The Role of a Mortgage Strategist

In a complex market, you don't just need a loan officer; you need a strategist. My role is to help you navigate the intersection of interest rates, grant availability, and property valuation. Whether you are a first-time buyer in Kentucky or a seasoned investor in Georgia or Michigan, the goal is the same: maximize leverage and minimize out-of-pocket costs.

The 0.9% price growth in Kentucky is not a sign of a weak market; it is a sign of a stable one. It is an opportunity to buy the "right" house at the "right" price without the noise of a bubble.

Compare your options, analyze the data, and position yourself for a successful closing.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664