The Florida Investor's Gold Mine: Why DSCR is the ONLY Way to Build Your Real Estate Empire in 2026

Florida’s real estate market in 2026 is no longer the Wild West it was a few years ago. We have entered a phase of calculated stability, where the "fast money" has left and the "smart money" is doubling down. If you are looking to scale a portfolio in the Sunshine State today, you have likely realized that the old ways of financing properties: clinging to W-2 income and tax returns: are holding you back.

The truth is, for high-velocity growth, the Florida DSCR loan lender landscape has become the primary engine for success. In a state where insurance costs fluctuate and condo regulations are tighter than ever, understanding the Debt Service Coverage Ratio (DSCR) is your competitive advantage.

The 2026 Florida Market Reality: Where the Opportunities Hide

The Florida market has bifurcated into very specific regional plays. While the statewide median price has found a steady rhythm, the story on the ground in Orlando, Miami, and Tampa is vastly different.

Miami’s Condo 'Reckoning' (SIRS)

In Miami, we are witnessing the impact of the Structural Integrity Reserve Study (SIRS) legislation. Older coastal buildings are finally being forced to fund their reserves fully. This has led to a "reckoning" for condo owners: higher HOA fees and occasional special assessments. For the savvy investor, this creates a window to buy into buildings that have already completed their milestone inspections and structural remediations. When you use a Miami DSCR loan, the lender focuses on the property's ability to cover these new, higher carrying costs through its rental income.

Orlando’s Supply Shift

Orlando is currently digesting a massive wave of new multifamily deliveries. This means competition for tenants is real. However, single-family homes in top-tier school zones remain a high-demand asset. Investors are shifting away from generic "buy and hold" toward highly specialized Orlando investment property financing strategies that target these resilient pockets of the market.

Tampa’s Stability

Tampa continues to lead the state in job growth and in-migration. While the inventory has balanced out to nearly five months of supply, the demand for well-located rental housing hasn't flinched. The key to winning in Tampa in 2026 is ensuring your financing allows for quick execution before the best deals are scooped up by institutional players.

Why W-2s are a Trap for Florida Scaling Investors

Many investors start their journey using conventional financing. They provide pay stubs, W-2s, and two years of tax returns. This works for the first two or three properties, but then you hit the wall.

Traditional debt-to-income (DTI) calculations do not favor the entrepreneur. If you are a self-employed investor in Florida, your tax professional likely works hard to legally minimize your taxable income. While this is great for your IRS bill, it is devastating for your ability to qualify for a traditional mortgage.

A Florida investment property loans strategy based on DSCR ignores your personal income entirely. We don't care about your W-2. We care about the property's performance. This allows you to keep your personal debt separate from your business growth, ensuring your ability to borrow isn't capped by your personal salary.

DSCR Deep Dive: Mastering the Math

To win in the 2026 market, you must understand the math that lenders use to approve your deals. The Debt Service Coverage Ratio is the ultimate benchmark of a property's health.

The Formula: Gross Rent vs. PITIA

The calculation is straightforward: Gross Monthly Rent / Monthly PITIA (Principal, Interest, Taxes, Insurance, and Association fees).

The 1.25x 'Sweet Spot'

While some "no-ratio" programs exist for investors with high equity, the "Sweet Spot" for the most competitive rates is typically a DSCR of 1.25x. This means for every $1,000 in mortgage and carrying costs, the property generates $1,250 in rent.

Lenders view this 25% buffer as a safety net. It accounts for vacancy, minor repairs, and the inevitable "Florida factor": the volatility in property taxes and insurance premiums. You can explore how these numbers impact your specific scenario using our mortgage calculators.

Short-Term Rental (STR) Supremacy in Florida

Florida remains the global capital for vacation rentals. Whether it is a Disney-adjacent villa in Kissimmee, a beachfront escape in Destin, or a luxury pad in Miami, the STR market is where the highest yields are found.

Leveraging AirDNA Data

Traditional banks struggle to understand Airbnb income. They want to see 12-month leases. However, we specialize in Florida Airbnb financing loans that utilize AirDNA data. We look at the "market projections" for your specific zip code to qualify the loan.

If a property in Kissimmee can generate $6,000 a month in high-season vacation stays but would only rent for $3,000 as a long-term rental, a DSCR lender can use the higher figure to justify the loan. This is how investors are acquiring high-cash-flow assets that would never qualify under standard bank rules. This specialized Florida short term rental mortgage approach is essential for anyone operating in tourism-heavy markets.

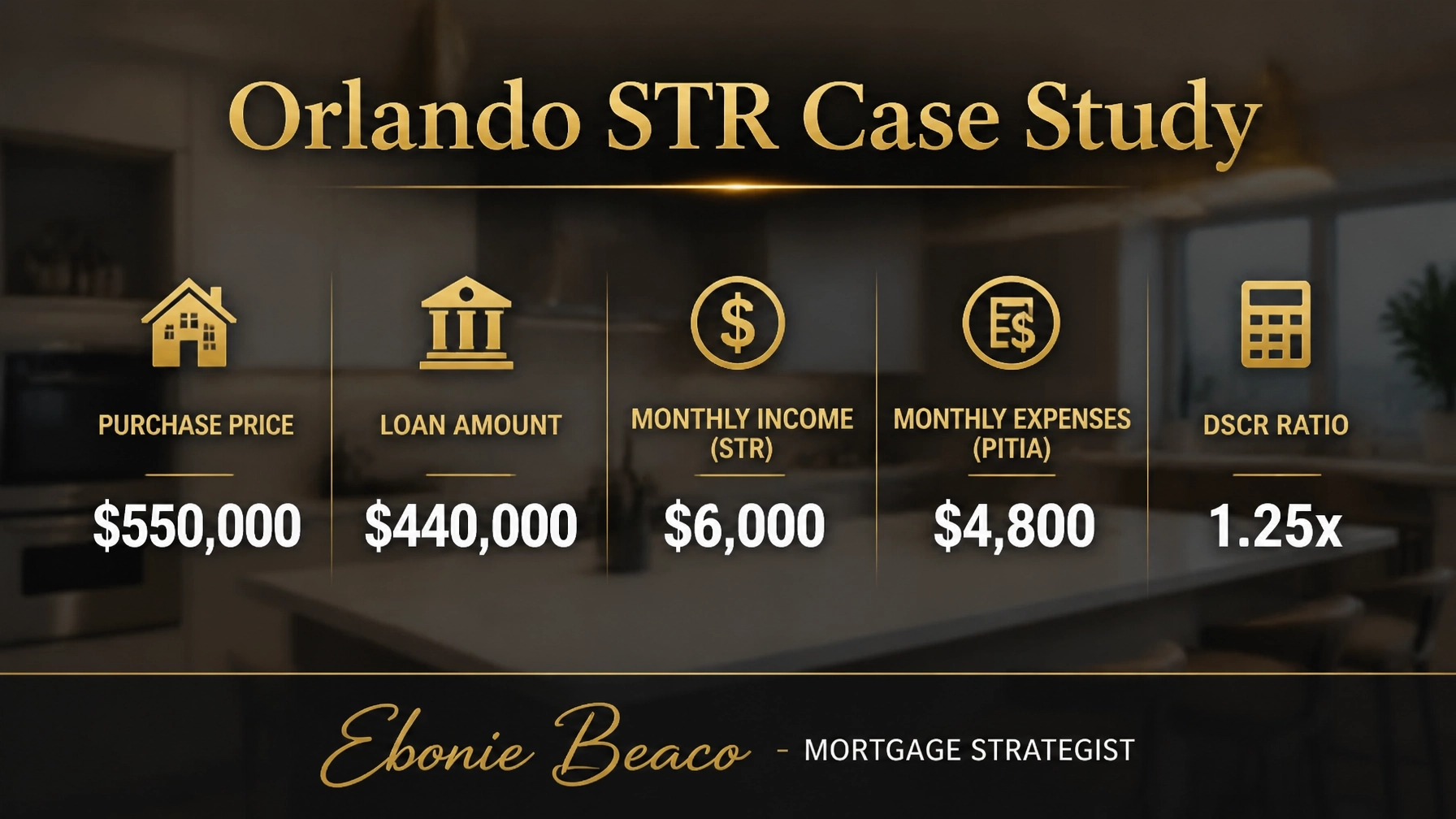

Orlando STR Case Study: A 2026 Breakdown

Let’s look at a real-world example of how these numbers "pencil out" in today’s market.

In this scenario, even with higher 2026 interest rates and the increased cost of insurance, the property still hits the 1.25x DSCR target. This is because the short-term rental income significantly outpaces the carrying costs. This is the "gold mine" that many investors miss when they only look at long-term lease averages.

The 2026 Insurance Factor: Facing the Crisis Head-On

You cannot talk about Florida rental property financing without talking about insurance. The Florida insurance crisis is a reality that every investor must navigate. Premiums in coastal areas like St. Petersburg or Miami have seen dramatic shifts over the last 24 months.

How DSCR Lenders Factor in Rising Premiums

In 2026, lenders have become more conservative with their "stress tests." When we underwrite your deal, we aren't just looking at last year's insurance bill. We are looking at current quotes from multiple carriers, including Citizens where necessary.

Every extra $1,000 in annual insurance costs reduces your property’s Net Operating Income (NOI). Because the DSCR ratio is sensitive to these costs, an insurance spike can actually reduce your maximum loan amount. This is why working with an expert strategist is vital: we help you structure the deal with enough of a buffer so that a 10% jump in premiums doesn't sink your investment.

Portfolio Scaling: Breaking the 10-Property Ceiling

If you use conventional loans, you are usually capped at 10 financed properties. For an empire builder, 10 properties is just the beginning.

Closing in an LLC

Asset protection is a non-negotiable for serious landlords. Conventional loans require you to close in your personal name. DSCR loans, however, allow: and often encourage: you to close in the name of an LLC. This separates your personal liability from your real estate holdings.

No Limits on Growth

With Florida investment property loans, there is no arbitrary cap on the number of properties you can finance. As long as each property "stands on its own two feet" by meeting the DSCR requirements, you can continue to acquire assets. This is the "infinite scale" model used by the top 1% of Florida investors. You can learn more about how we help investors grow in our about us section.

Compare Your Options and Jump In

The 2026 market belongs to those who act on data rather than fear. Florida continues to be a magnet for wealth, and housing remains the most reliable vehicle for capturing that growth. Whether you are targeting a multifamily building in Tampa or a vacation rental in Destin, the right financing strategy is the difference between a "good idea" and a "closed deal."

Explore the different loan programs available to you and see how we can align your financing with your 2026 wealth goals. Our loan process is designed to move at the speed of your business, ensuring you never miss a golden opportunity because of slow bank bureaucracy.

Access your custom DSCR scenario today and find out how much equity you can leverage to build your Florida empire.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664