The 7:00 PM Mortgage News Recap: June 5 Market Shifts Explained in Under 3 Minutes

Today is Friday, June 5, 2026, and the financial markets have delivered a series of significant updates that directly impact how homeowners and investors approach real estate financing. While the headline figures suggest a cooling labor market, the underlying bond market activity tells a more complex story regarding the cost of borrowing. This evening recap provides the essential data points you need to navigate the current landscape in Alabama, Florida, Illinois, and beyond.

The most notable shift today occurred in the bond market, where the 30-year Treasury yield surged to approximately 5.12%. This movement is critical because mortgage lenders often benchmark their pricing against long-term government bond yields. When yields rise, mortgage interest rates typically follow, creating a direct connection between federal debt markets and the monthly payment on a single-family home or a multi-unit investment property.

Treasury Yields and the 6% Benchmark

The 30-year Treasury yield is the interest rate the U.S. government pays to borrow money for three decades. It serves as a foundational "risk-free" rate that influences nearly all other long-term lending. For mortgage strategists and investors, watching this figure is more informative than tracking the Federal Funds Rate alone, as it more accurately reflects the market's long-term inflation expectations.

Mortgage rates today are hovering in the mid-6% range, specifically between 6.48% and 6.51% for standard conventional loans. This represents a modest pullback from earlier highs, yet remains elevated compared to the historical lows seen in previous years. For real estate investors in high-growth markets like Atlanta, Georgia, or Tampa, Florida, these rates require a more precise approach to deal analysis and cash flow projections.

Explore our Mortgage Basics to understand how these bond market fluctuations impact your specific loan scenario.

The Labor Market: "Low Fire, Low Hire"

The June 5 jobs report revealed a "steady but not strong" labor market with an unemployment rate holding at 4.3%. Economists are currently describing this dynamic as "low fire, low hire," meaning companies are retaining their current staff but are hesitant to expand aggressively. For the housing market, a stable labor force is generally positive as it supports consistent demand, but the lack of explosive growth may keep the Federal Reserve from cutting rates as quickly as some had hoped.

Inflation remains a persistent factor, with recent data showing a 3.8% year-over-year increase in consumer prices. This persistent inflation prevents the "pivot" to lower rates that many first-time homebuyers in Michigan and Indiana have been waiting for. When inflation stays above the Fed's 2% target, the cost of capital remains high, which reinforces the importance of using specialized financing strategies like DSCR loans or HELOCs to access liquidity.

DSCR (Debt Service Coverage Ratio): A mortgage technical term defined as a calculation used by lenders to determine if a property's rental income can cover its monthly debt obligations. In practical application, real estate investors use DSCR loans to qualify for financing based on the property’s performance rather than their personal income or DTI.

Regional Market Snapshots: Illinois to California

The housing inventory gap continues to define the market across several key states. In Chicago, Illinois, and surrounding suburbs, the "listing income alignment score" shows that current household incomes can only afford about 75% of the available inventory. This mismatch means that while more homes are hitting the market, they are often priced above what the average local buyer can comfortably finance.

In California and Virginia, the demand for short-term rental financing remains high despite elevated rates. Investors are increasingly looking toward Airbnb and STR (Short-Term Rental) properties to offset higher borrowing costs with higher nightly revenue. We are seeing a significant trend where investors use bridge loans to acquire distressed properties, renovate them, and then transition into long-term DSCR or Non-QM financing once the property is stabilized.

Jump in and review our Chicago Neighborhood Market Reports for local insights on inventory and pricing shifts.

Strategic Equity Access: Cash-Out Refinance vs. HELOC

As property values in states like Florida and Alabama remain resilient, homeowners are sitting on record levels of tappable equity. Accessing this wealth requires a strategic choice between a cash-out refinance or a Home Equity Line of Credit (HELOC). Each serves a different purpose depending on your current primary mortgage rate and your long-term financial goals.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows a homeowner to borrow against their equity as needed, typically with a variable interest rate. This is an ideal tool for homeowners who want to keep their low-rate first mortgage while still having access to funds for renovations or new investments.

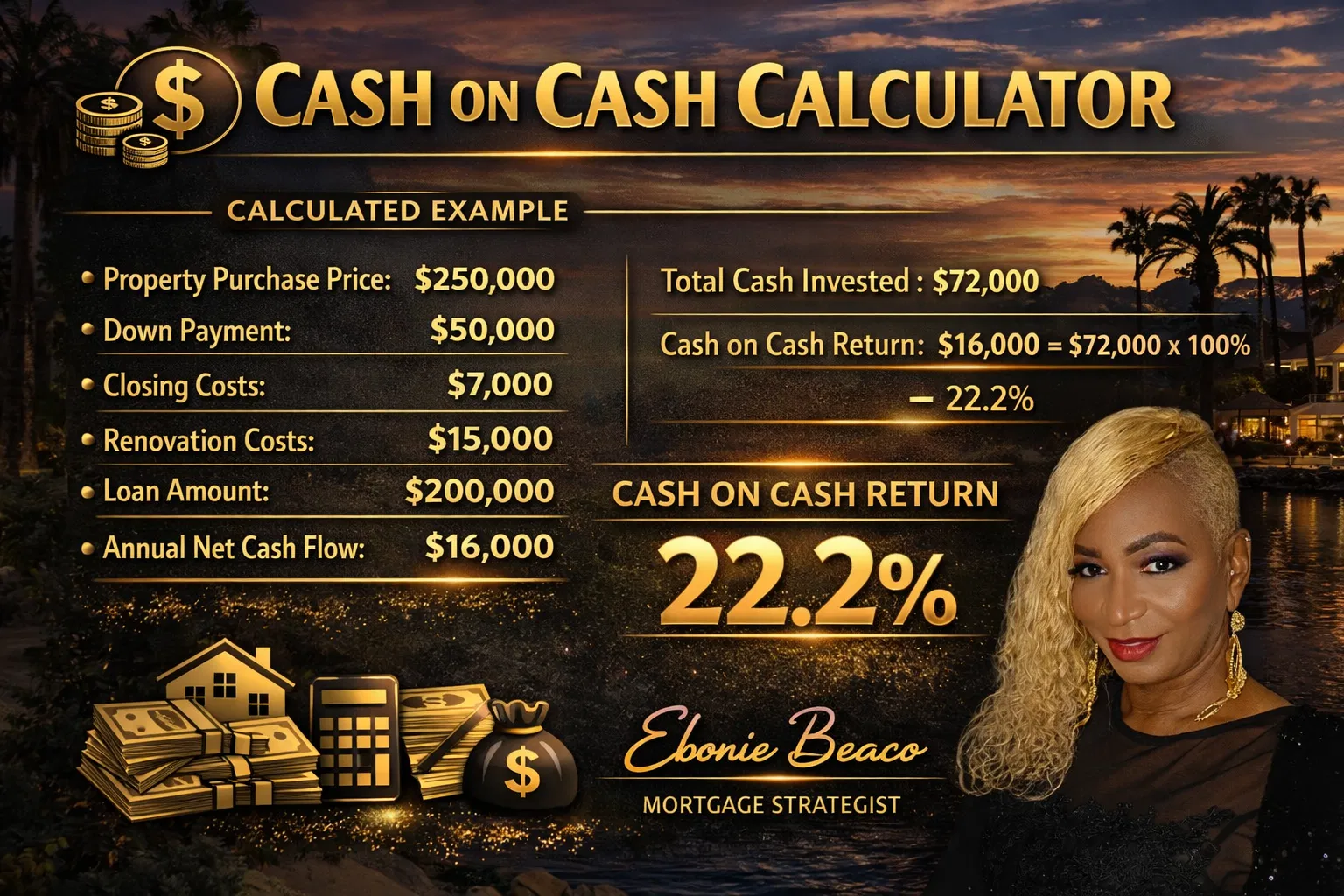

Consider a homeowner in Virginia with a property valued at $600,000 and an existing mortgage balance of $300,000. If the lender allows for an 80% combined loan-to-value (CLTV), the homeowner could potentially access $180,000 in equity.

Calculation Example:

- Property Value: $600,000

- Max Loan (80% CLTV): $480,000

- Existing Mortgage: $300,000

- Available Equity: $180,000

Access our Mortgage Calculators to run these numbers for your own property and see how much equity you can put to work.

Investor Focus: The BRRRR Strategy in 2026

For real estate investors, the current environment of mid-6% rates makes the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy more challenging but still highly effective when executed with precision. Today's market rewards those who find off-market deals or distressed properties in states like Missouri and Kentucky, where entry prices remain relatively accessible.

The key to success in 2026 is the "Refinance" step. With many analysts predicting that rates will remain in the 6% range for the foreseeable future, investors must ensure their "All-In" costs (purchase + rehab) allow for a refinance that still produces positive cash flow. Using a Hard Money or Fix-and-Flip loan for the initial acquisition allows for a quick close, which is often necessary to secure the best deals in a competitive environment.

DTI (Debt-to-Income Ratio): A dictionary-style definition identifies this as the percentage of a borrower's gross monthly income that goes toward paying monthly debt payments. For self-employed borrowers in California or Florida, using Bank Statement Loans can be a better path to financing because these programs calculate income based on deposits rather than taxable income shown on tax returns.

Summary of Today's Market Moves

The June 5 market shifts highlight a transition toward a "higher for longer" interest rate environment. While the slight dip in mortgage rates to 6.48% is a welcome sign for some, the spike in Treasury yields suggests that a significant drop below 6% is unlikely in the immediate future.

- Mortgage Rates: Trending in the mid-6% range (approx. 6.5%).

- Treasury Yields: 30-year yield at 5.12%, maintaining upward pressure on rates.

- Employment: 4.3% unemployment indicates a stable but cautious economy.

- Strategy: Investors should focus on DSCR and equity-access tools (HELOC/Cash-out) to maintain momentum.

Reference link: The Mortgage Note - Morning Roundup June 5

Whether you are a first-time homebuyer in Arkansas or a seasoned multi-unit investor in Chicago, understanding these daily shifts allows you to make informed decisions rather than reacting to headlines. The goal is to align your financing strategy with your long-term wealth-building objectives, regardless of short-term market volatility.

Compare your options by reviewing our Loan Programs to see which solution fits your current portfolio needs.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664