The 7:00 AM Mortgage News Update: Today’s Market Movements Explained in Under 3 Minutes

Welcome to your Monday morning briefing. As the sun rises across the Chicago skyline and reaches the coastlines of Florida and California, the mortgage market is already in motion. Staying ahead of rate fluctuations is essential for anyone managing a real estate portfolio or planning a home purchase.

The current landscape reflects a delicate balance between stabilizing inflation and a resilient labor market. While we have moved away from the peak volatility seen in previous quarters, the "higher for longer" narrative remains a central theme for the Federal Reserve. This update breaks down the critical data points you need to navigate the market today.

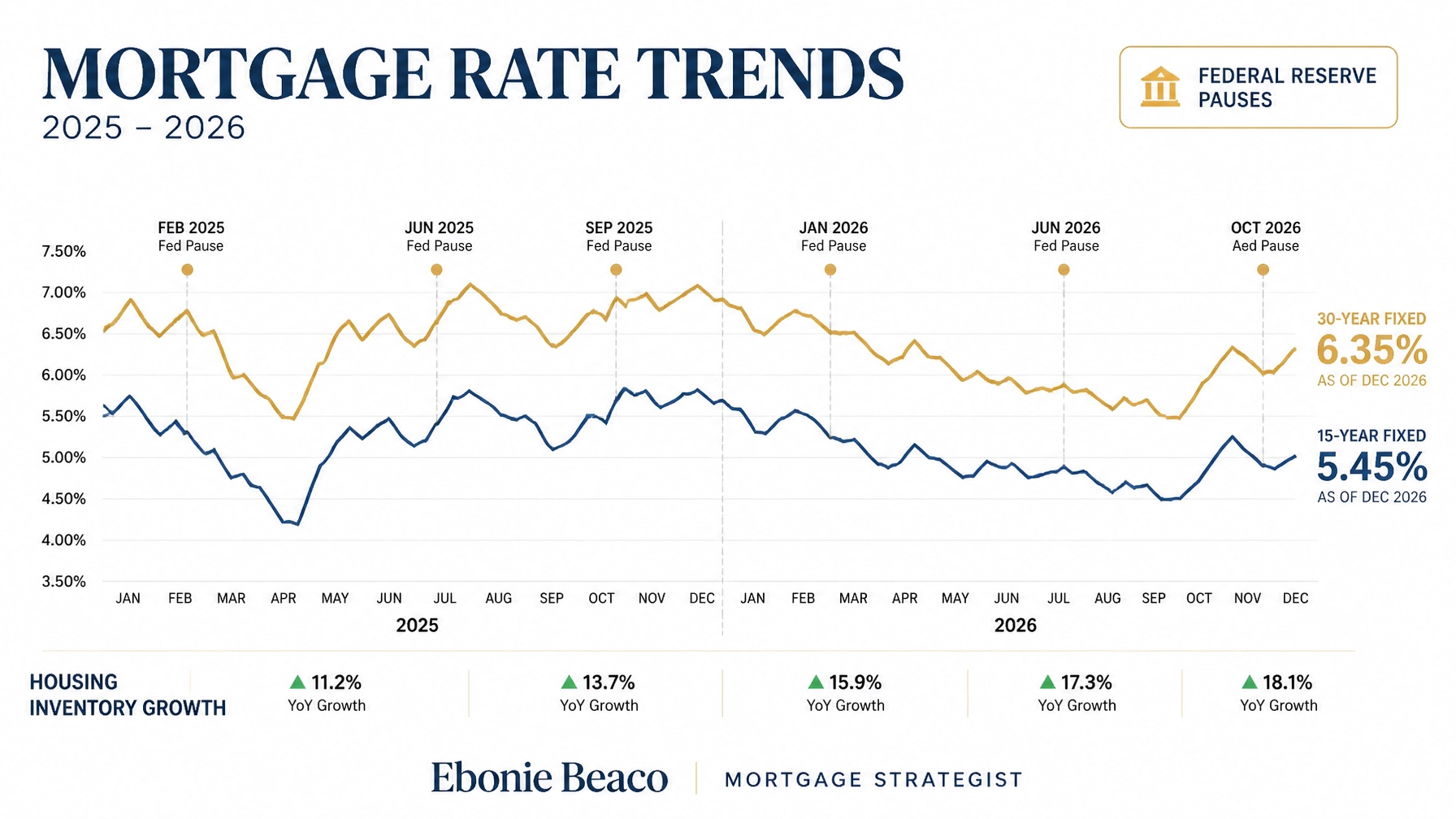

Current Mortgage Rate Averages: Where We Stand Today

As of this morning, the national average for a 30-year fixed-rate mortgage is hovering near 6.85%. This represents a slight downward drift from the highs of late 2024, but it remains elevated compared to historical averages from the previous decade. Borrowers looking at shorter durations will find the 15-year fixed-rate averaging approximately 6.04%, providing a lower interest cost for those who can manage the higher monthly payments.

The 5/1 Adjustable-Rate Mortgage (ARM) is currently positioned near 6.04%. While ARMs were once viewed with skepticism, many investors in markets like Virginia and Georgia are utilizing them as a short-term bridge strategy. They bet on refinancing when the Federal Reserve eventually pivots toward a more aggressive easing cycle.

Breaking Down the Daily Market Indices

To better understand how these figures impact your buying power, it is helpful to look at the daily movements. The 10-year Treasury yield, which mortgage rates track closely, is currently stabilized around 4.3%. Any significant shift in this yield typically precedes a change in consumer mortgage pricing within 24 to 48 hours.

Explore current trends by visiting our home purchase guide to see how these rates align with your specific property goals.

The Federal Reserve and the "Waiting Game" for Rate Cuts

The Federal Reserve’s recent commentary suggests a cautious approach toward lowering the federal funds rate. Market expectations for 2025 and early 2026 have shifted from multiple cuts to potentially only one or zero, depending on core inflation data. Inflation remains "sticky," particularly in the service sector and housing components, which prevents the Fed from declaring a total victory.

For homeowners in Michigan and Indiana, this means the window for a significant rate-term refinance has not fully opened yet. However, the strong labor market: with unemployment holding steady around 4.0%: ensures that buyer demand remains robust. A healthy job market provides the financial stability required for consumers to sustain homeownership even at current rate levels.

Housing Inventory: The Supply Squeeze Across Target States

Inventory levels continue to be a primary driver of home prices in states like Alabama, Arkansas, and Missouri. While active listings have seen a modest seasonal increase, the overall supply remains approximately 30% below pre-pandemic norms. This scarcity creates a competitive environment for buyers, often leading to multiple-offer scenarios in desirable neighborhoods.

New construction is currently filling the gap left by the "lock-in effect," where homeowners with 3% mortgage rates are reluctant to sell. Builders in growing metros across Virginia and Florida are offering aggressive incentives, including rate buy-downs, to attract buyers. This has made new homes a more viable path for many first-time buyers who are struggling with limited resale options.

Regional Market Activity Highlights

- Illinois and Chicago: Strong demand for multi-unit buildings as investors seek to hedge against inflation.

- Florida: Continued migration is supporting price appreciation despite higher insurance costs.

- California: High-equity markets are seeing a surge in cash-out refinance activity for property improvements.

- Georgia: A hot spot for Airbnb and short-term rental investors looking for yield.

Compare these regional shifts using our mortgage calculators to analyze potential monthly payments in your local area.

Key Mortgage Terms Defined for Today’s Market

Understanding the technical language of real estate finance is the first step toward making an informed decision. Here are the core concepts driving today’s headlines:

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments with its own rental income.

- Application: This allows real estate investors to qualify for a loan based on the property's cash flow rather than their personal W-2 income or tax returns.

HELOC (Home Equity Line of Credit): A revolving credit line that uses the equity in your home as collateral.

- Application: You can access funds as needed for renovations, investment down payments, or emergency expenses, paying interest only on what you draw.

Cash-Out Refinance: A mortgage refinancing option where the new loan is for a larger amount than the current mortgage, and the difference is paid to the borrower in cash.

- Application: This is a powerful strategy for extracting equity to fund the purchase of additional rental properties or to renovate a primary residence to increase its value.

Non-QM (Non-Qualified Mortgage): A loan that does not meet the standard criteria of a traditional mortgage, often used for self-employed borrowers or those with unique financial profiles.

- Application: It provides a path to homeownership for entrepreneurs and investors who may have high bank statement deposits but significant tax deductions.

Strategic Financing: How Investors are Using Equity Right Now

In a market where rates are not at record lows, the focus has shifted from "lowest rate" to "highest return on equity." Savvy investors are tapping into their existing property value to scale their portfolios. One of the most popular tools currently is the HELOC, which allows for flexibility without disturbing a low-rate first mortgage.

For example, a homeowner in Virginia with significant equity might use a HELOC to fund a fix-and-flip project or a down payment on a DSCR rental property. This allows them to keep their 3% or 4% primary mortgage intact while still accessing capital at a competitive variable rate.

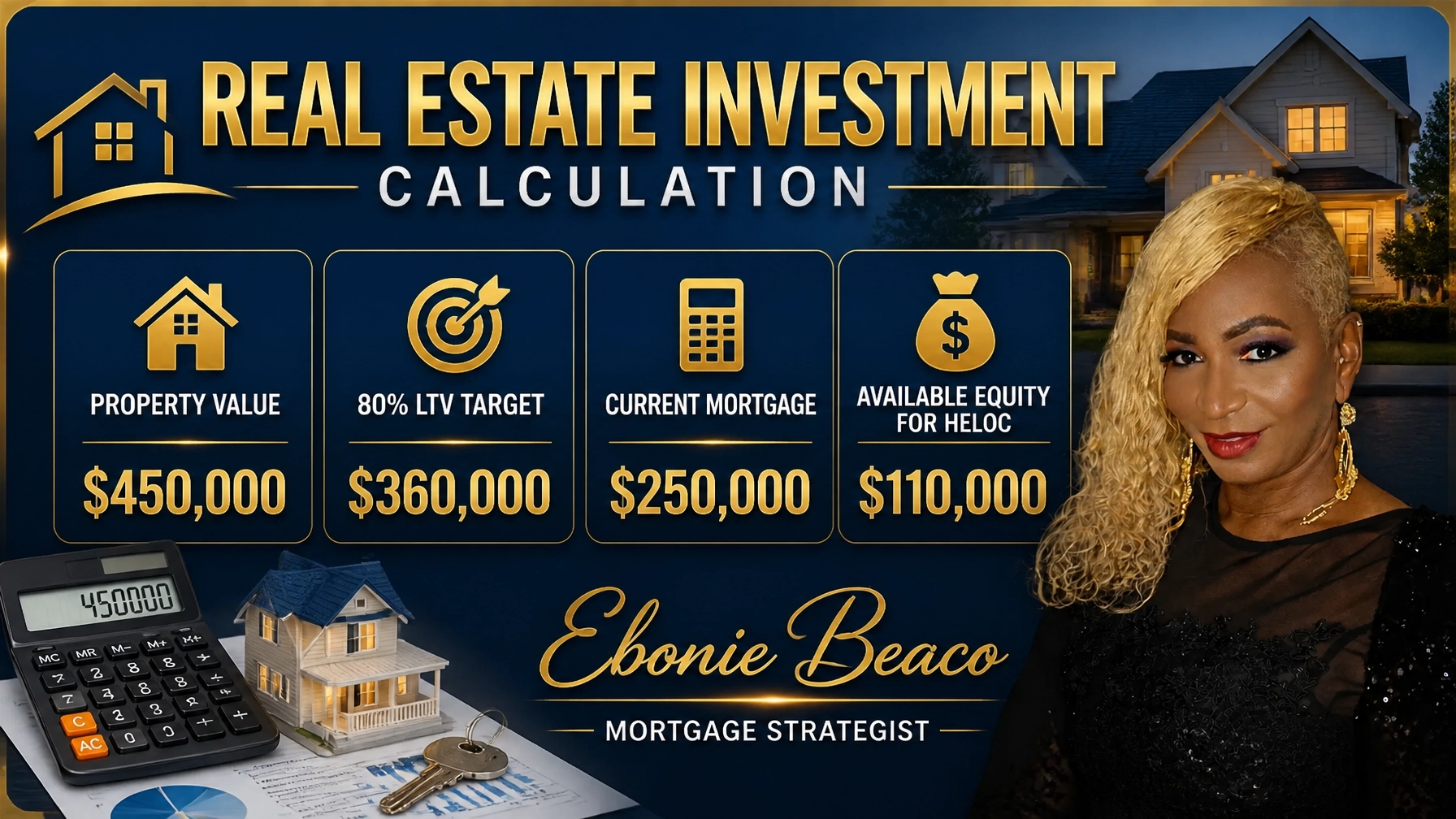

A Practical Equity Access Example

Consider a homeowner with the following financial profile:

- Current Property Value: $450,000

- Current Mortgage Balance: $250,000

- Lender LTV Limit: 80% (Maximum total debt allowed: $360,000)

- Available Equity for HELOC: $110,000 ($360,000 max minus $250,000 existing)

By securing a $110,000 line of credit, this homeowner could potentially fund two down payments on investment properties in more affordable markets like Arkansas or Kentucky. This strategy transforms a stagnant asset into a wealth-building engine.

Access more details on these strategies in our loan programs overview.

The Rise of DSCR Loans for Landlords

For investors looking to bypass the hurdles of traditional bank financing, the DSCR Investor Loan is becoming the standard. Because these loans focus on the property’s income, they are ideal for scaling a portfolio quickly. Lenders typically look for a ratio of 1.0 or higher, meaning the rental income covers the mortgage, taxes, insurance, and HOA fees.

In high-rent markets like Chicago or Atlanta, many properties easily meet these requirements. This allows investors to close on multiple properties simultaneously without being limited by the "ten-property rule" often found in conventional lending. Whether you are looking at a single-family home or a small multi-unit building, DSCR loans offer a streamlined path to closing.

Short-Term Rental Financing: The Airbnb Pivot

While some markets have seen a "cool down" in short-term rental performance, experienced operators are still finding success by focusing on high-demand vacation destinations in Florida and coastal Virginia. Financing for these properties requires a lender who understands the nuances of seasonal income and platform-based revenue (like Airbnb and VRBO).

Non-QM lenders often offer programs specifically designed for these types of investments. They may allow the use of projected "AirDNA" data to qualify the property’s income potential. This is a game-changer for investors buying in areas where traditional long-term rents might not support a standard mortgage payment.

Commercial and Multi-Unit Opportunities

Beyond single-family homes, there is a growing interest in commercial multi-unit properties. Apartment buildings with 5 or more units fall under commercial lending guidelines, which often offer different terms and structures than residential loans. Financing a 12-unit building in Michigan or a mixed-use property in Kentucky requires a deep understanding of capitalization rates and net operating income (NOI).

Why Commercial Financing is Attractive Today:

- Scalability: Managing one 10-unit building is often more efficient than 10 individual houses.

- Valuation: Commercial property value is driven by income, not just comparable sales.

- Portfolio Diversification: Adding different property types protects against local market shifts.

Final Market Outlook: What to Watch This Week

As we move through this week, keep a close eye on the Thursday unemployment claims and any upcoming inflation data releases. These reports will dictate the short-term direction of mortgage bonds. If data comes in "hotter" than expected, we could see rates move back toward the 7% mark. Conversely, any sign of economic cooling could provide a brief window for lower pricing.

For realtors and investors, the key is to stay prepared. Ensure your pre-approvals are updated and your "deal analyzer" tools are ready. The most successful participants in today's market are those who act with speed and certainty once a property fits their financial criteria.

Jump in and explore your options today. Access our full suite of educational resources to stay informed as the market evolves.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Reference Links: