The 70% Rule: Is This Classic Wholesale Real Estate Strategy Still Relevant?

Meta Title: The 70% Rule in 2026: Still Relevant for Wholesale Real Estate? Meta Description: Learn how the 70% rule works in wholesale real estate today. See calculation examples and discover if this classic strategy still secures profitable deals.

Entering the world of wholesale real estate often feels like learning a brand-new language filled with acronyms, contract jargon, and complex financial formulas. Among these, the 70% rule stands out as perhaps the most famous guideline used by real estate investing professionals to quickly vet a potential deal. Historically, this rule has served as a protective shield for investors, helping them avoid overpaying for distressed properties that require significant renovation. As we navigate the housing market in 2026, many new wholesalers wonder if this classic formula still holds weight or if it has become an outdated relic of a different economic era. Understanding the nuances of this rule is the difference between securing a lucrative assignment fee and getting stuck with a contract that no cash buyer wants to touch.

To understand why this rule is so prevalent, we first have to look at its core purpose: risk mitigation for the end buyer. In a typical wholesale real estate transaction, you are looking for a property that you can put under contract and then assign to a fix-and-flip investor or a long-term landlord. These cash buyers are taking on the heavy lifting of construction, carrying costs, and market risk, so they require a significant profit margin to justify the investment. The 70% rule is designed to bake that profit into the purchase price from day one, ensuring there is enough "meat on the bone" for everyone involved in the transaction. If you bring a deal to an investor that follows this formula, you are essentially speaking their language and demonstrating that you understand the financial mechanics of a successful flip.

Defining the Core Components of the Formula

Before we dive into the math, we need to establish clear definitions for the variables that make up the 70% rule. The most critical piece of the puzzle is the After Repair Value (ARV), which is the estimated market value of the property once it has been fully renovated to modern standards. ARV is not a guess; it is derived from looking at comparable sales: properties of similar size and style that have sold within a half-mile radius in the last six months. Following the ARV, you must accurately estimate the Rehab Costs, which include everything from roof repairs and HVAC systems to cosmetic upgrades like flooring and paint. Finally, the Wholesale Fee is your profit, which must be accounted for within the 70% threshold if you want the deal to remain attractive to your buyer list.

Visual: A realistic modern suburban house. Overlay text: ARV $300,000 | 70% Rule | Max Offer $170,000. Footer: Ebonie Beaco - Mortgage Strategist.

Visual: A realistic modern suburban house. Overlay text: ARV $300,000 | 70% Rule | Max Offer $170,000. Footer: Ebonie Beaco - Mortgage Strategist.

The Math in Action: A Real-World Calculation Example

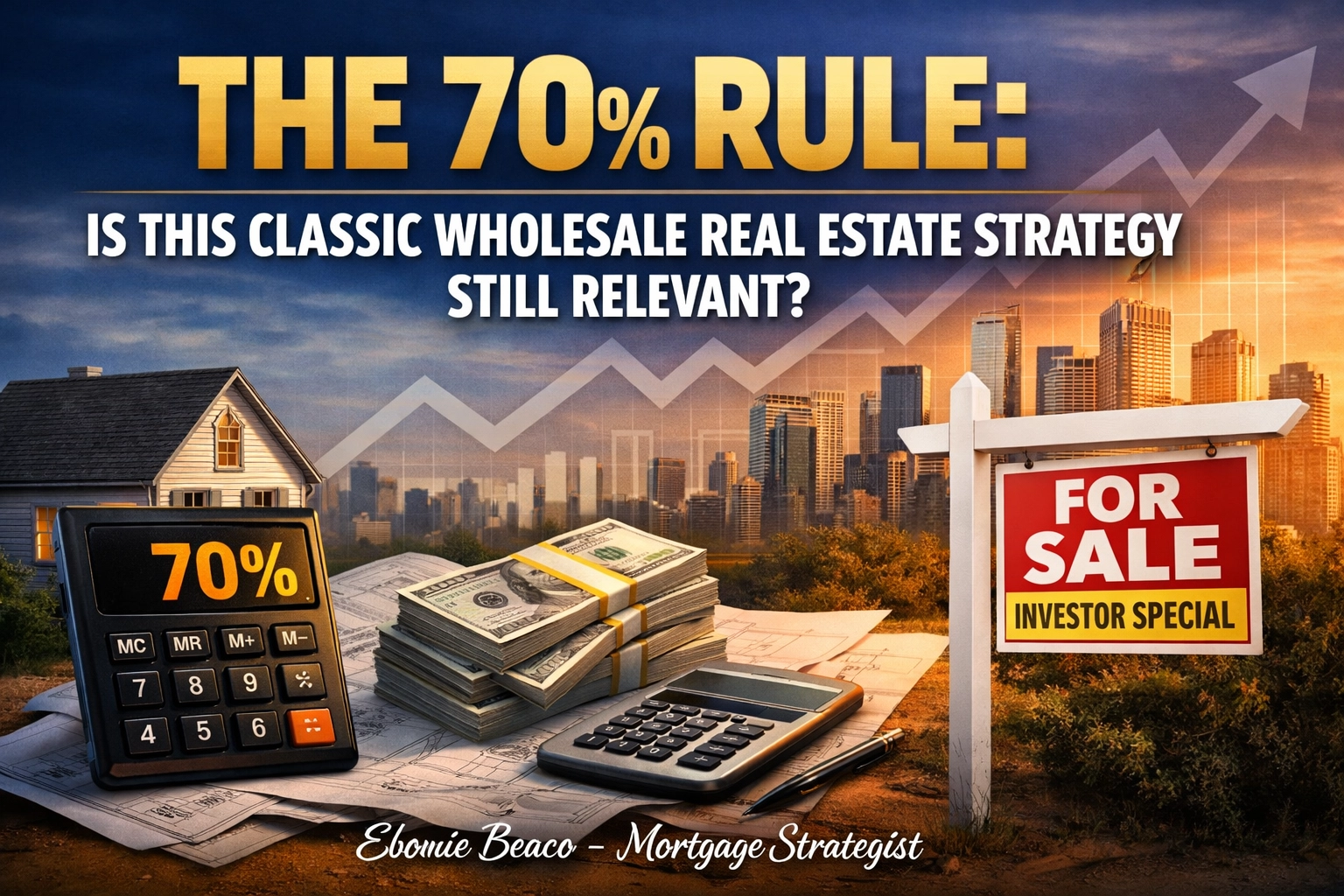

Let’s look at a practical breakdown to see how the numbers actually function when you are standing in front of a motivated seller. Imagine you find a distressed property in a neighborhood where fully renovated homes are selling for $300,000; this figure is your ARV. According to the 70% rule, you would multiply $300,000 by 0.70, which gives you a base starting point of $210,000. From that $210,000, you must subtract the estimated costs of the repairs needed to bring the home up to that top-tier market value. If the house needs $40,000 in work, your Maximum Allowable Offer (MAO) to the seller would be $170,000, assuming you want to leave room for the investor's profit.

- After Repair Value (ARV): $300,000

- 70% Multiplier: $300,000 x 0.70 = $210,000

- Estimated Rehab: $40,000

- Max Offer to Seller: $170,000

If you manage to get the property under contract for $160,000, you can assign it to a buyer for $170,000 and walk away with a $10,000 wholesale fee. This ensures that the end buyer is still purchasing the property at or below the 70% threshold, keeping their profit margins intact even after paying your fee. You can use our mortgage calculators to help your buyers understand their potential carrying costs if they choose to finance the acquisition. This level of transparency builds incredible trust with your buyer list and sets you apart from wholesalers who just "guess" at the numbers.

Adapting the Rule for Different Markets

While the 70% rule is a fantastic starting point, it is important to acknowledge that real estate is hyper-local and varies significantly by region. In high-demand markets like parts of California, Florida, or the Chicago metro area, competition is so fierce that many cash buyers are willing to "pay up" for a deal. In these scenarios, you might see investors using a 75% or even an 80% rule because the sheer volume of appreciation or the high price point allows for a smaller percentage margin while still yielding a large dollar-amount profit. Conversely, in rural areas or slower markets in states like Arkansas or Alabama, a more conservative 65% rule might be necessary to account for longer holding times and lower demand. Successful wholesalers learn to adjust the slider based on the specific zip code they are targeting.

The rule also serves as a quick "litmus test" when you are evaluating off-market deals during your initial lead intake process. If a seller is asking $250,000 for a home that only has an ARV of $280,000, you immediately know that the 70% rule (which would put the offer around $196,000 minus repairs) is nowhere near their asking price. This allows you to quickly pivot your strategy, perhaps looking into creative financing or simply moving on to a more motivated lead. You can learn more about how we help structure these transitions in our loan process guide. Knowing when to walk away from a deal that doesn't fit the math is just as important as knowing when to sign a contract.

Why Financing Strategies Matter for Your Buyers

As a wholesaler, your job doesn't end when the contract is signed; you need to ensure your buyer can actually close the deal. Many real estate investing pros rely on specialized financing like fix and flip loans, hard money, or bridge loans to fund their acquisitions and renovations. If you understand how these loan programs work, you can better explain to a seller why your buyer is a "sure thing" despite not using traditional bank financing. Providing your buyers with a direct line to a mortgage strategist like Ebonie Beaco can help them secure the funding they need to take your wholesale deal across the finish line. We often see investors use a cash-out refinance on their existing properties to fund the purchase of your next wholesale assignment.

Furthermore, once the renovation is complete, many investors choose to keep the property as a rental using DSCR investor loans. These loans qualify based on the property’s rental income rather than the borrower’s personal income, making them a favorite for those scaling a portfolio through the BRRRR method. By understanding the full lifecycle of the investment, you can market your wholesale deals more effectively to specific types of buyers. If you know a house would make a perfect long-term rental, you can highlight the projected rental income and the ease of getting a DSCR loan once the repairs are done. This holistic approach to wholesaling houses transforms you from a simple "middleman" into a valuable consultant for your investment partners.

Common Pitfalls and How to Avoid Them

The most common reason a wholesale deal fails is not the formula itself, but the data entered into it. Overestimating the ARV is a frequent mistake made by beginners who want a deal to look better than it actually is. If you tell a buyer a house is worth $300,000 but the highest comparable sale is only $270,000, the 70% rule breaks down instantly, and your credibility takes a hit. Similarly, underestimating rehab costs can lead to a "thin" deal where the buyer ends up losing money once they uncover hidden issues like mold or structural damage. Always leave a buffer in your repair estimates to account for the unexpected problems that inevitably arise in distressed real estate.

Another pitfall is ignoring the "fixed costs" that the 70% rule is meant to cover. This 30% gap between the purchase price and the ARV isn't just pure profit for the buyer; it covers closing costs, property taxes, insurance, loan interest, and real estate commissions when they eventually sell the home. If an investor is using a jumbo loan or high-interest bridge financing, their "holding costs" will be significantly higher than a buyer using all cash. Being mindful of these expenses allows you to speak intelligently with seasoned pros who are looking at the bottom line. If you can provide a clear breakdown of why the numbers work, you will find that finding cash buyers becomes the easiest part of your business.

Conclusion: Mastering the Fundamentals

Ultimately, the 70% rule remains a cornerstone of the industry because it provides a standardized framework for evaluating risk and reward. While you should certainly adapt the percentage to fit your local market conditions, the underlying logic of leaving room for profit, repairs, and expenses is timeless. As you grow your business in wholesale real estate, you will find that the most successful investors are the ones who remain disciplined and trust the math over their emotions. Whether you are working in the bustling streets of Chicago or the growing suburbs of Virginia, the numbers will always tell the true story of a deal. Stay focused, do your due diligence, and never be afraid to ask for professional guidance when structuring your transactions.

📞 Work With Ebonie Beaco

If you are a wholesaler looking to:

- Close more deals

- Connect your buyers with financing

- Structure deals that actually get approved

- Learn how to grow into a real estate investor

I can help you every step of the way.

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954

📱 Phone: 312-392-0664 📧 Schedule a 1 on 1: https://calendly.com/homeloansnetwork 🌐 Website: HomeLoansNetwork.com/contact-us

👉 Whether you need lending, deal structuring, or mentorship, reach out today.