The 70% Rule in House Flipping: Is it Still Relevant?

If you have spent more than five minutes researching real estate investing, you have encountered the 70% Rule. It is often treated as the "Golden Rule" for fix-and-flip investors from Chicago to Miami. But as we navigate the housing market in 2026, many investors are asking if this old-school math still holds up.

Let's break down what this rule is, how it functions in today’s market, and whether you should rely on it when securing Fix and Flip Loans.

What Exactly is the 70% Rule?

The 70% Rule is a quick screening tool used by investors to determine the maximum price they should pay for a distressed property.

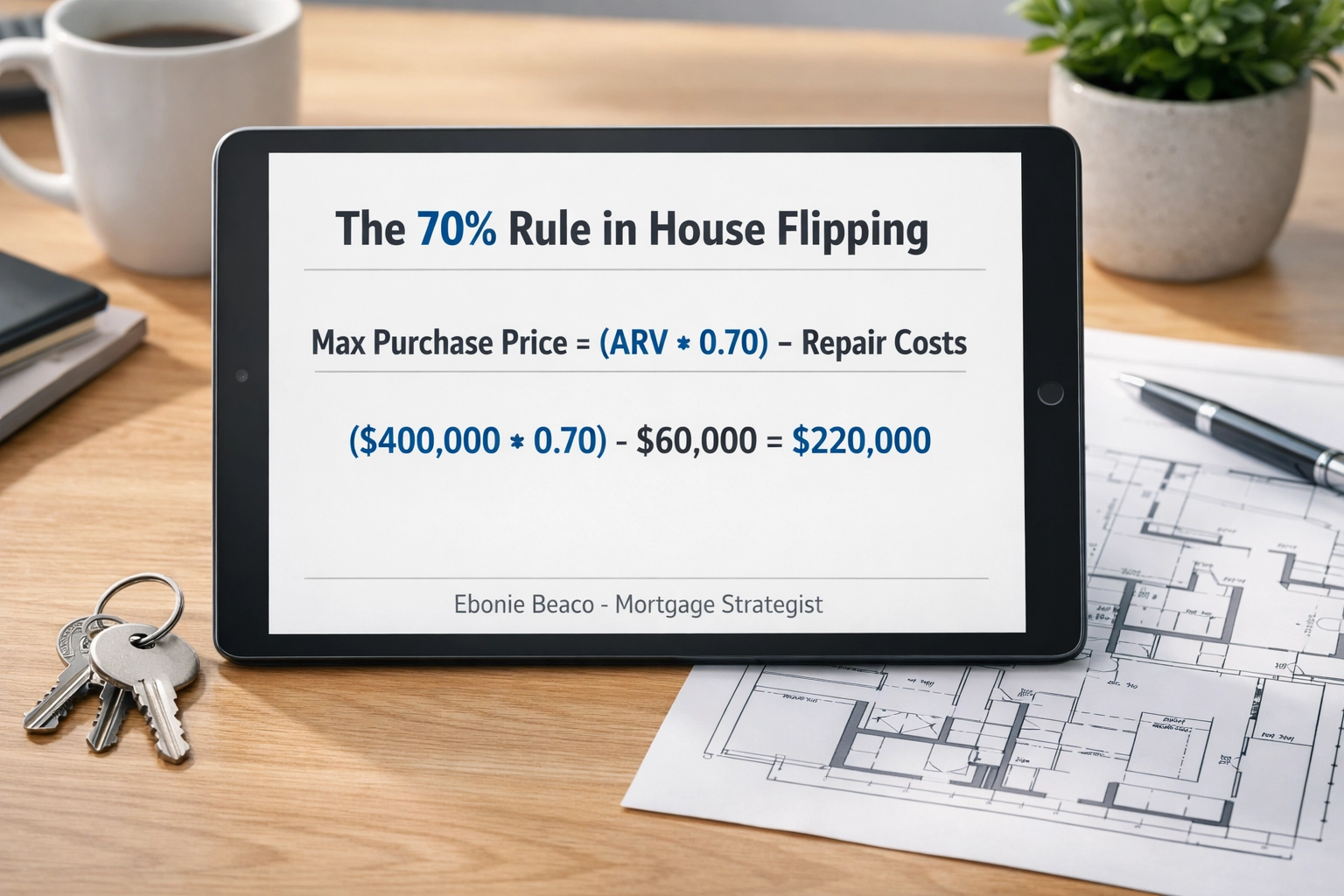

The logic is simple. You take the After Repair Value (ARV): which is what the home will be worth once it’s fully renovated: and multiply it by 70%. Then, you subtract the estimated repair costs.

The resulting number is your Maximum Allowable Offer (MAO).

Defining the Components

After Repair Value (ARV): The estimated market value of a property after all necessary repairs and upgrades are completed. This is based on comparable sales (comps) in the immediate area.

Repair Costs: The total budget needed to bring the property from its current condition to "retail ready" status. This includes materials, labor, permits, and a contingency fund.

The 30% Buffer: This covers your closing costs, holding costs (taxes, insurance, utilities), financing costs (interest on your Bridge Loans or Hard Money Loans), selling costs (realtor commissions), and, most importantly, your profit.

Doing the Math: A Real-World Scenario

Let’s look at a practical example. Imagine you find a distressed single-family home in a suburb of Indianapolis or a neighborhood in Virginia.

- Estimated ARV: $400,000

- Estimated Repairs: $60,000

- The Calculation: ($400,000 x 0.70) - $60,000 = $220,000

In this scenario, your Max Purchase Price is $220,000.

Visual Breakdown: Title: 'The 70% Rule in House Flipping'. Image shows: Max Purchase Price = (ARV * 0.70) - Repair Costs. Calculation: ($400,000 * 0.70) - $60,000 = $220,000. Bottom Text: Ebonie Beaco - Mortgage Loan Officer.

Visual Breakdown: Title: 'The 70% Rule in House Flipping'. Image shows: Max Purchase Price = (ARV * 0.70) - Repair Costs. Calculation: ($400,000 * 0.70) - $60,000 = $220,000. Bottom Text: Ebonie Beaco - Mortgage Loan Officer.

If you can buy the house for $220,000 and spend $60,000 on repairs, you are "all-in" for $280,000. If you sell it for $400,000, that $120,000 spread covers all your fees and leaves a healthy profit. You can use our mortgage calculators to help run these numbers on your own deals.

Is 70% Still Realistic in 2026?

In a perfect world, every investor would buy at 70% of ARV. However, the reality of the 2026 market often looks different.

High-Cost Markets vs. Emerging Markets

In high-demand areas like Southern California or certain parts of Florida, finding a deal at 70% of ARV is incredibly difficult. Competition from other investors and a lack of inventory often push purchase prices higher.

In these "hot" markets, investors often adjust the rule to the 75% or 80% Rule.

If you are flipping a luxury home in a high-price-point area, your profit margin might be smaller as a percentage, but the raw dollar amount is still significant enough to justify the risk.

Conversely, in markets like Arkansas or parts of Michigan where entry prices are lower, sticking to the 70% rule is often safer. When the total dollar amount is smaller, there is less room for error if repair costs spike.

The Impact of Financing Costs

The interest rates on Fix and Flip Financing play a massive role in whether the 70% rule works for you.

When interest rates are higher, your "holding costs" increase every month the property sits under renovation. If you are using a loan process that involves high-leverage hard money, that 30% buffer disappears faster than you might think.

When to Bend the Rule

The 70% rule is a guide, not a law. There are specific situations where you might choose to pay more.

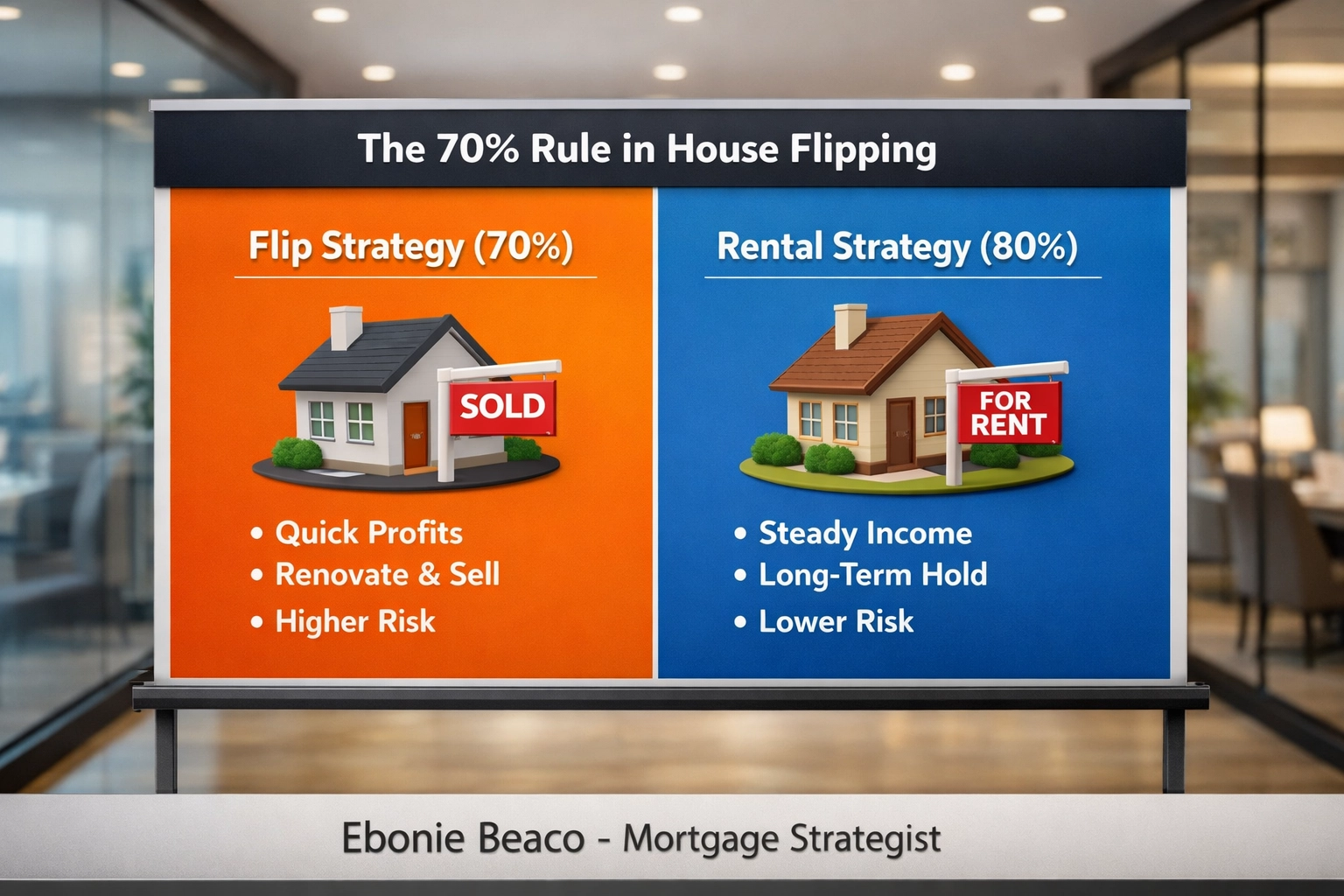

The Buy and Hold Strategy (BRRRR)

If you aren't planning to sell the house immediately, you might be able to pay more than 70%. Landlords using the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) often look at DSCR Investor Loans for their long-term financing.

Because a landlord's goal is long-term cash flow and appreciation rather than a quick flip profit, they might be comfortable buying at 75% or 80% of ARV. If the rental income covers the mortgage and expenses, the initial purchase price is less restrictive. You can read more about this in our FAQ section.

High Confidence in ARV

If you are a seasoned pro in a specific neighborhood in Chicago or Atlanta and you know the "comps" better than anyone, you might feel comfortable squeezing your margins. If you know for a fact that the house will sell in three days for a premium, you can afford to pay a bit more on the front end.

Visual: A comparison chart showing "Flip Strategy (70%)" vs. "Rental Strategy (80%)". Title: 'The 70% Rule in House Flipping'. Bottom Text: Ebonie Beaco - Mortgage Loan Officer.

Visual: A comparison chart showing "Flip Strategy (70%)" vs. "Rental Strategy (80%)". Title: 'The 70% Rule in House Flipping'. Bottom Text: Ebonie Beaco - Mortgage Loan Officer.

Common Mistakes When Using the Rule

Even the best formulas fail if the data you put into them is wrong.

Underestimating Repairs: This is the number one reason flips fail. Investors often forget to account for permits, unexpected structural issues, or the rising cost of materials in 2026.

Inaccurate Comps: Just because a house down the street sold for $500,000 doesn't mean yours will. You must compare apples to apples: same square footage, same level of finish, and same location.

Ignoring Holding Costs: Many new investors forget to account for the monthly interest payments on their Bridge Loans, the cost of builder's risk insurance, and property taxes during the six months the house is under construction.

How Financing Supports Your Strategy

Whether you are sticking strictly to the 70% rule or adjusting for a specific market, having the right financing in place is crucial.

At Home Loans Network, we work with investors to structure deals that make sense.

- Fix and Flip Loans: Short-term funding designed to cover both the purchase and the renovation costs.

- DSCR Rental Property Loans: Financing based on the property’s income rather than your personal income, perfect for landlords.

- Cash-Out Refinance: A way for current homeowners or investors to pull equity out of one property to fund the down payment on the next flip.

If you're unsure how a specific property fits into your portfolio, exploring about us can give you insight into how we guide our clients through these complex decisions.

The Role of Mentoring in Modern Flipping

The math is easy; the execution is hard. This is why many investors seek out mentoring.

A mentor helps you look past the formula to see the "hidden" aspects of a deal. They can help you vet contractors, verify ARV, and choose the right loan product. Sometimes, the best deal you ever do is the one you walk away from because the 70% rule told you the numbers didn't work.

If you are looking for more than just a loan, you need a strategist who understands the nuances of the markets in Georgia, Virginia, and beyond.

Final Thoughts: The Verdict on 70%

Is the 70% rule still relevant? Yes.

It remains the best way to quickly "stress test" a deal. If a property doesn't come close to the 70% mark, you know immediately that you need to take a much closer look at the margins before proceeding.

However, you should treat it as a starting point, not the finish line. In 2026, flexibility is the key to scaling a real estate business.

If you have a deal on the table and you want a professional eye to help you analyze the numbers: or if you're ready to secure funding for your next project: let's talk. We provide the tools and the capital to help you navigate these markets with confidence.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664