The 4:00 PM Wrap-Up: Today’s Mortgage Rate Trends Explained in Under 3 Minutes

Navigating the mortgage market requires a sharp eye on daily shifts, especially when economic indicators flash new signals every afternoon. As of Friday, May 22, 2026, the lending landscape reflects a complex mix of domestic inflation concerns and global geopolitical shifts. For homeowners and investors alike, understanding these movements is the first step toward securing a strategy that protects your wealth. Explore the details below to see how today’s closing numbers influence your next real estate transaction.

Today’s Key Rate Benchmarks

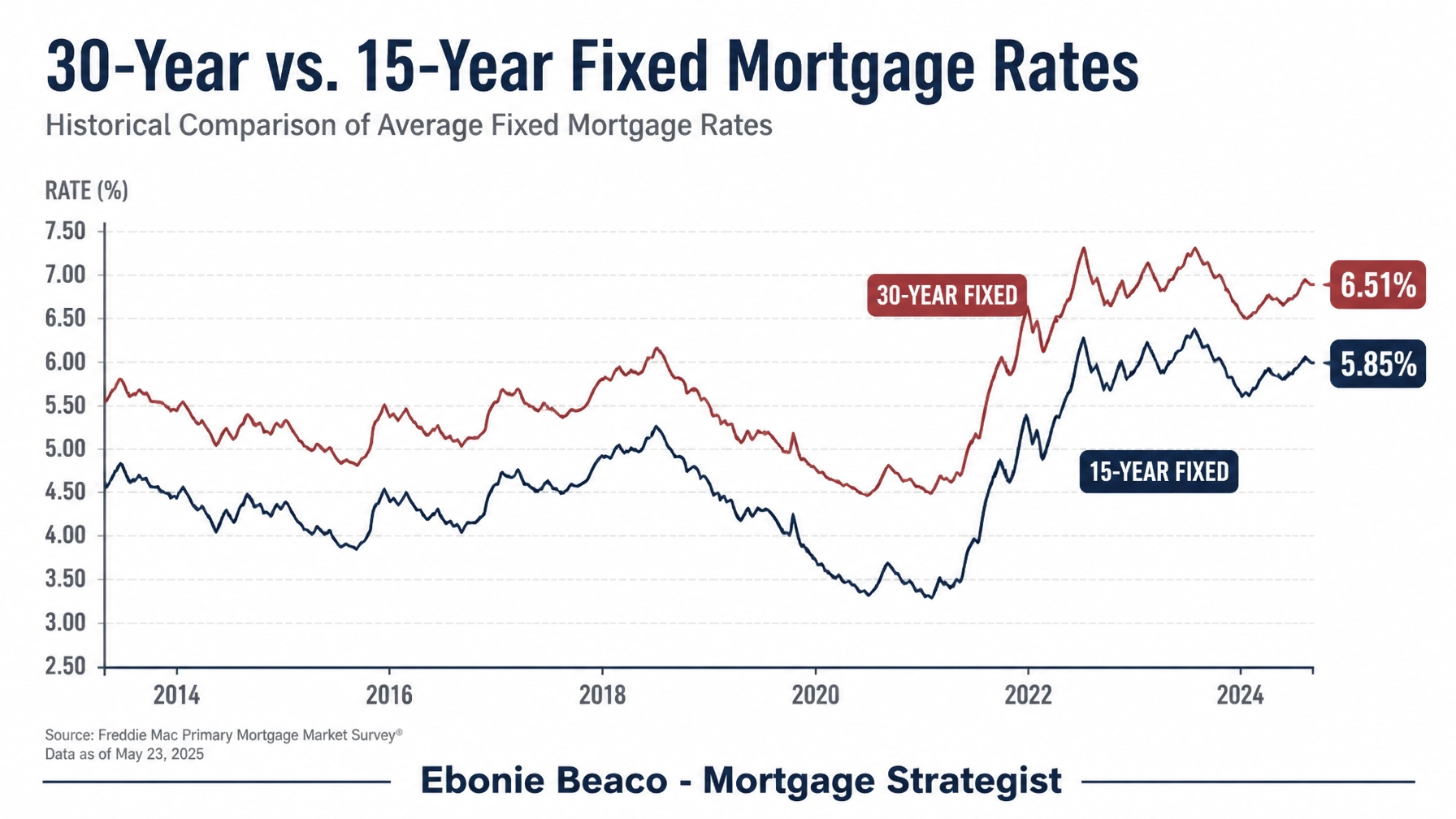

The national averages for mortgage products have shown significant movement as we close out the week. According to the Freddie Mac Primary Mortgage Market Survey, the 30-year fixed-rate mortgage now sits at an average of 6.51%, a notable increase from the previous week. Meanwhile, the 15-year fixed-rate mortgage has adjusted to 5.85%, offering a lower-cost alternative for those prioritizing faster equity build-up. These levels represent the highest rates observed in nearly nine months, reflecting a tighter borrowing environment than we saw earlier this spring.

Why Rates Are Moving: The Economic Drivers

Several factors converged this week to push yields higher and increase the cost of home financing. Rising inflation data and a sudden spike in oil prices have forced investors to move capital out of bonds, which inversely drives up the 10-year Treasury yield. Because mortgage rates closely follow the 10-year Treasury, this sell-off in the bond market directly translates to higher monthly payments for new borrowers. Additionally, ongoing geopolitical risks, including tensions in the Middle East, continue to create a "risk-off" sentiment that adds volatility to the mortgage basics you see in daily quotes.

Understanding the Terms

To better navigate these updates, it helps to define the core concepts influencing your loan programs today:

- Basis Points (BPS): A unit of measure used in finance to describe the percentage change in the value or rate of a financial instrument; one basis point is equal to 0.01%.

- Treasury Yield: The return on investment, expressed as a percentage, on the U.S. government's debt obligations; this acts as the primary benchmark for fixed mortgage rates.

- Inflation Hedge: An investment intended to protect the investor against a decrease in the purchasing power of money; real estate is traditionally viewed as a strong hedge.

Strategies for Real Estate Investors: The DSCR Advantage

For investors in markets like Chicago, Illinois, or the growing suburbs of Virginia and Georgia, today’s rate hike emphasizes the importance of cash-flow analysis. While traditional financing may feel more expensive, DSCR (Debt Service Coverage Ratio) Loans remain a powerful tool for scaling portfolios because they focus on the property’s income rather than your personal DTI. Explore how an investor might analyze a potential acquisition even in a higher-rate environment. By focusing on properties with strong rental yields, you can often offset the increased cost of debt through consistent monthly cash flow.

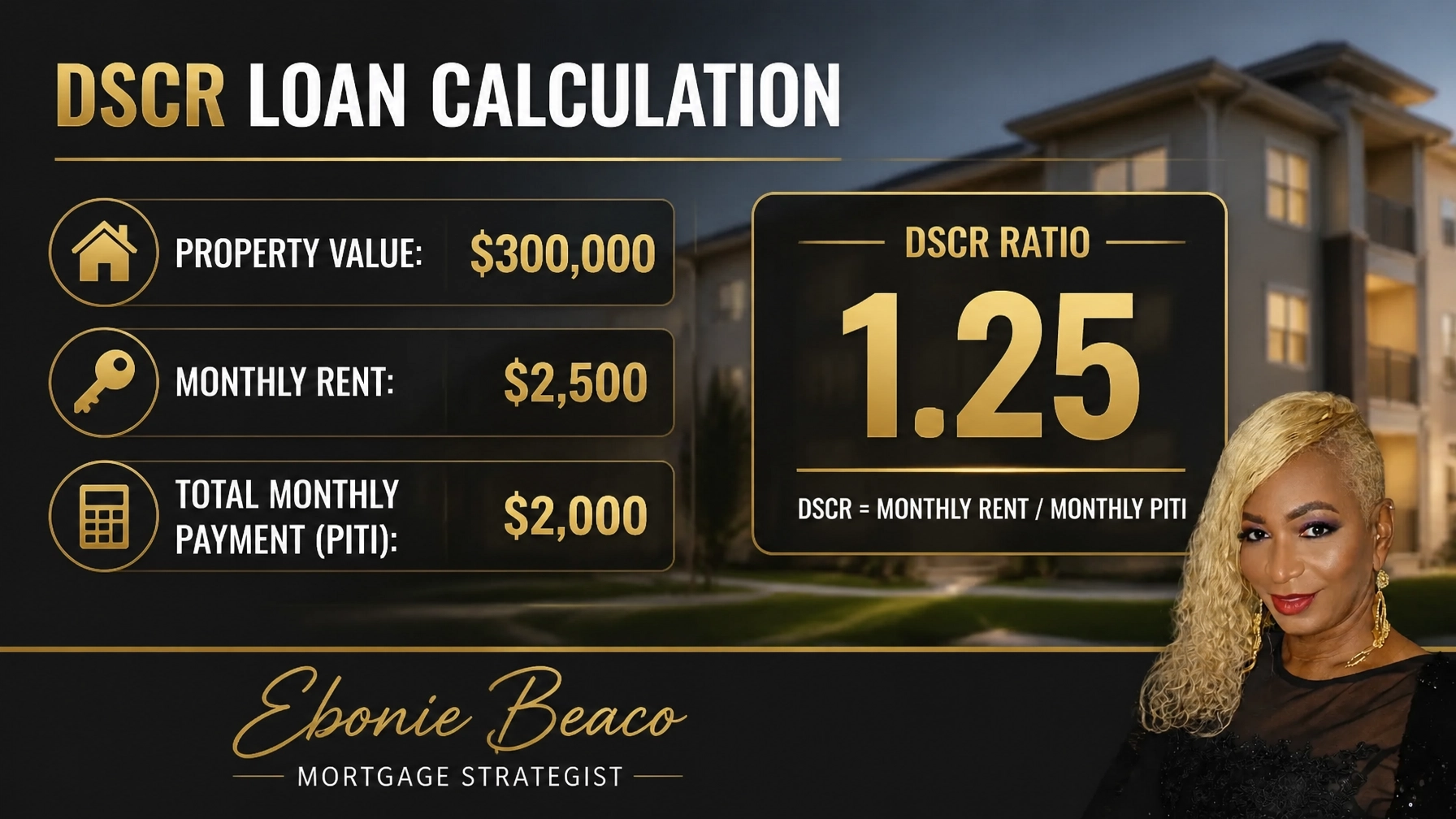

Example: DSCR Calculation for a Rental Property

If you are looking at a multi-unit building in a market like Florida or Michigan, the math must work regardless of the national average. Imagine a property valued at $300,000 that generates a monthly rent of $2,500. If the total monthly payment: including principal, interest, taxes, and insurance (PITI): is $2,000, your DSCR ratio is 1.25. Lenders typically look for a ratio of 1.20 or higher, meaning this scenario comfortably qualifies for financing. Accessing these types of mortgage borrower loans allows you to continue building your portfolio without the constraints of traditional W-2 verification.

Homeowner Insights: Leveraging Equity with HELOCs

Current homeowners who purchased or refinanced during the record-low periods of 2021 may be hesitant to engage in a full home refinance today. However, your home has likely gained significant value over the last few years, creating a massive pool of untapped wealth. A HELOC (Home Equity Line of Credit) allows you to access this equity for renovations, debt consolidation, or a down payment on an investment property without touching your existing low-interest first mortgage. Jump in and see how much equity you might have available based on current market valuations.

Example: Accessing Equity via a HELOC

Suppose your home in California or Indiana is currently valued at $500,000, and your existing mortgage balance is $280,000. Many lenders will allow you to borrow up to 85% of your home’s value, which in this case totals $425,000. By subtracting your existing $280,000 mortgage from that $425,000 limit, you are left with $145,000 in available equity. This line of credit gives you the flexibility to fund your goals while keeping your primary mortgage rate intact. Compare your options by visiting our mortgage calculators to run your specific numbers.

Regional Market Activity: State-by-State Focus

While national trends provide a broad view, real estate is inherently local, and activity varies across the states we serve. In Alabama and Arkansas, we see consistent demand for affordable single-family homes, even as rates tick upward. In California and Florida, the market remains competitive due to low inventory levels, though higher rates have led to more room for negotiation on the buyer's side. Kentucky, Missouri, and Indiana continue to be hotspots for investors looking for lower entry points and higher rental yields. Understanding the local nuances in Michigan and Georgia can help you time your entry or exit perfectly.

Actionable Steps for Today’s Market

The current trend suggests that waiting for a significant drop in rates may result in missing out on current property opportunities. Instead, focus on structuring deals that make sense with today's numbers, knowing that you can always look at a rate-term refinance if the market shifts in the future. Evaluate your current financial profile and property goals to determine which home purchase or investment strategy aligns with your long-term objectives. Our team is here to guide you clearly and confidently through these fluctuations, ensuring you have the data needed to make informed decisions.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664