The 1% Rule: A Quick Way to Screen Rental Properties

If you are a real estate investor, you know that time is your most valuable asset. When you are looking at dozens of listings in markets like Chicago, Illinois, or Birmingham, Alabama, you cannot afford to spend hours running a full pro forma on every single house. You need a way to filter the "no-go" deals from the "maybe" deals in seconds.

Enter the 1% Rule.

This guideline is a favorite among landlords and real estate investors because it provides a baseline for potential cash flow without requiring a calculator and a spreadsheet. While it is not a final answer, it is a powerful first step in your home purchase journey.

What is the 1% Rule?

The 1% Rule is a diagnostic tool used to determine if the monthly rent of a property will exceed its monthly mortgage payment and basic operating costs.

Definition: The 1% Rule suggests that a rental property should generate at least 1% of its total acquisition cost in gross monthly rent.

Explore this concept as a speed-test for your investments. If a property costs $200,000, it needs to rent for at least $2,000 a month to pass the 1% test. If it only rents for $1,200, you likely have a property that will struggle to produce positive cash flow after you factor in taxes, insurance, and maintenance.

How to Calculate the 1% Rule

Calculating the 1% Rule is straightforward. You take the total price you paid for the property, including any immediate repairs needed to get it "rent ready," and multiply it by 0.01.

The Formula: (Purchase Price + Initial Renovation Costs) x 0.01 = Minimum Monthly Rent

Jump in with this real-world example: Imagine you find a distressed duplex in Gary, Indiana. You buy it for $120,000 and spend $30,000 on new flooring, paint, and updated kitchens. Your total investment is $150,000. To meet the 1% Rule, that duplex needs to bring in $1,500 in total monthly rent ($150,000 x 0.01).

Image Description: A professional infographic titled "The 1% Rule Explained" showing the calculation: Purchase Price ($150,000) + Repairs ($30,000) = Total Investment ($180,000). Total Investment x 1% = $1,800 Target Monthly Rent. Footer: Ebonie Beaco - Mortgage Loan Officer.

Image Description: A professional infographic titled "The 1% Rule Explained" showing the calculation: Purchase Price ($150,000) + Repairs ($30,000) = Total Investment ($180,000). Total Investment x 1% = $1,800 Target Monthly Rent. Footer: Ebonie Beaco - Mortgage Loan Officer.

Why Investors Use the 1% Rule for Screening

In competitive markets across Florida and Virginia, speed is essential. Wholesalers often blast out deals that disappear within hours. You do not always have time to call your insurance agent or check the specific property tax assessment for the current year.

Speed and Efficiency The rule allows you to scan a list of 50 properties and identify the five or six that warrant a closer look. It acts as a filter to remove properties that are priced too high relative to the local rental market.

Risk Mitigation By aiming for the 1% threshold, you create a "buffer." Since this rule only looks at gross rent, it assumes that the remaining 99% of the value (and the resulting rental income) will cover your mortgage basics, property management, and repairs.

Market Comparison You can use the rule to compare different regions. For instance, achieving the 1% Rule in parts of Michigan or Arkansas is often much easier than achieving it in high-priced coastal cities in California. This helps you decide where to deploy your capital for the best yield.

Market Realities: Where Does the Rule Work?

The 1% Rule is highly dependent on your geography. As a mortgage strategist, I see how different regions influence investor returns.

In the Midwest, specifically cities like Chicago or Detroit, investors often find properties that hit the 1% or even the 2% mark. These markets are known for lower acquisition costs and steady rental demand. If you are looking for cash-flow-heavy properties, these areas are often your best bet.

Conversely, if you are looking at properties in Orange County, California, or Arlington, Virginia, hitting the 1% Rule is extremely difficult. In these "appreciation markets," a $1 million home rarely rents for $10,000 a month. Investors in these areas often accept a "0.5% Rule" or lower because they are banking on the property value increasing over time rather than monthly cash flow.

Compare your options carefully. If your goal is to replace your 9-to-5 income, you likely need properties that meet or exceed the 1% Rule. If your goal is long-term wealth building and tax shelters, you might be okay with a property that falls short of the rule but is located in a high-growth area.

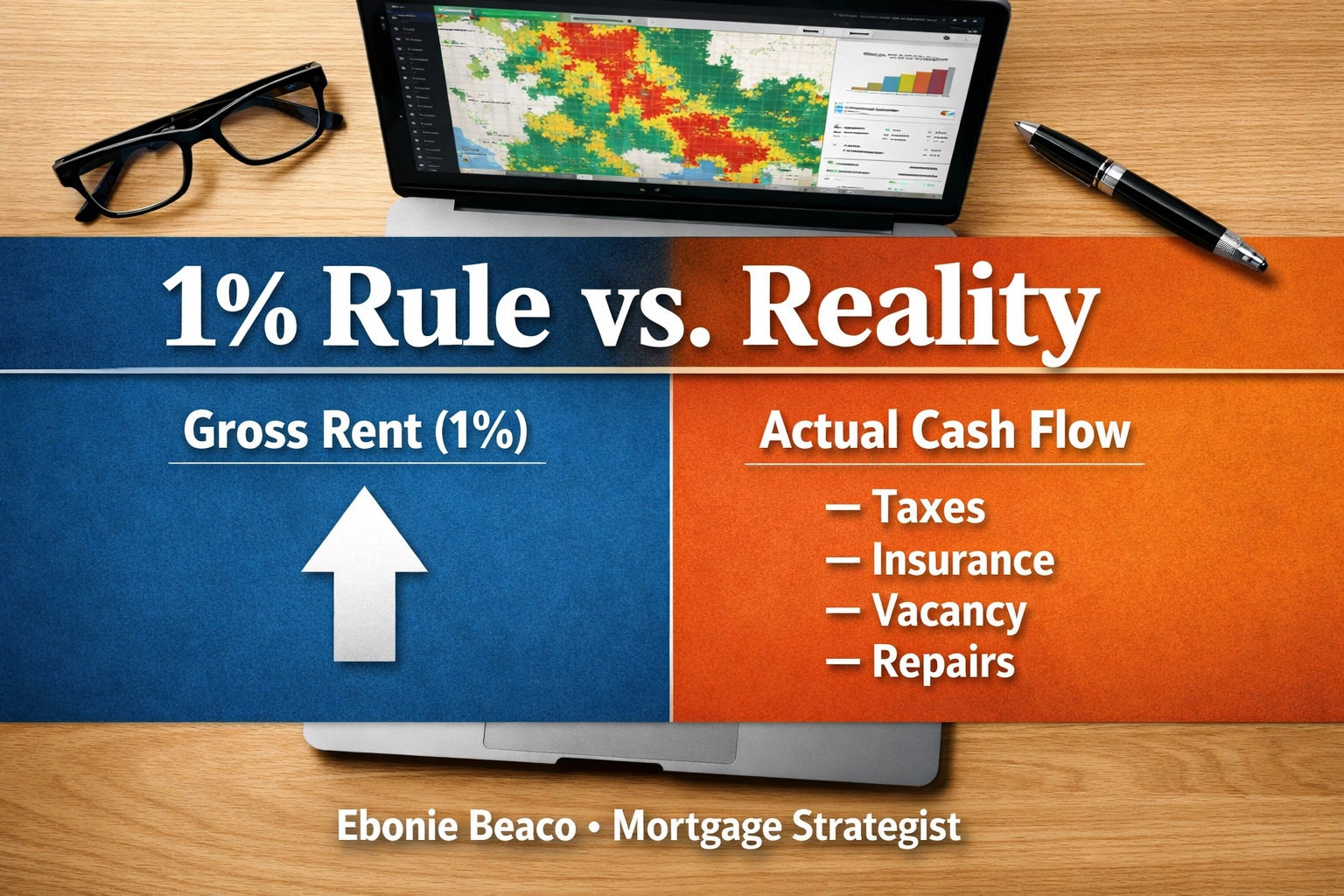

Limitations You Must Understand

While the 1% Rule is a great starting point, it is not a complete financial analysis. Using it in isolation can lead to poor investment choices. According to Investopedia, the rule does not account for the specific costs of owning a property, which vary wildly.

Operating Expenses The rule ignores property taxes. In some parts of Illinois, property taxes are significantly higher than in Florida. A property that meets the 1% Rule in a high-tax area might actually lose money every month, while a property that fails the rule in a low-tax state might be profitable.

Financing Costs The 1% Rule does not consider your interest rate or loan terms. If you are using a DSCR investor loan with a higher interest rate, your debt service will be higher. A property might pass the 1% test but fail to cover the actual mortgage payment if the financing is not structured correctly.

Maintenance and Capital Expenditures Older homes, common in parts of Virginia and Michigan, often require more maintenance. A 1% property that needs a new roof, a new HVAC system, and has lead pipe issues will quickly drain your bank account, regardless of the rental income.

Image Description: A comparison chart titled "1% Rule vs. Reality." Side A shows "Gross Rent (1%)" and Side B shows "Actual Cash Flow" after subtracting Taxes, Insurance, Vacancy, and Repairs. Footer: Ebonie Beaco - Mortgage Loan Officer.

Image Description: A comparison chart titled "1% Rule vs. Reality." Side A shows "Gross Rent (1%)" and Side B shows "Actual Cash Flow" after subtracting Taxes, Insurance, Vacancy, and Repairs. Footer: Ebonie Beaco - Mortgage Loan Officer.

Moving Beyond the 1% Rule: DSCR and Cash Flow

Once a property passes the 1% initial screen, it is time to look at the Debt Service Coverage Ratio (DSCR). This is a metric lenders use to qualify you for landlord loans without looking at your personal income.

DSCR Definition: A calculation that compares the property's annual net operating income to its annual debt insurance.

Lenders typically want to see a DSCR of 1.2 or higher. This means the property generates 20% more income than the cost of the mortgage. Many investors who use the 1% Rule find that their DSCR naturally falls into a healthy range, but it is always vital to verify the numbers with a mortgage calculator.

If you are a homeowner looking to transition into investing, you might consider a cash-out refinance on your primary residence. Accessing your equity can provide the down payment for a property that meets the 1% Rule, allowing you to scale your portfolio faster.

Strategies for BRRRR Investors and Flippers

For those using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, the 1% Rule applies to the post-renovation value.

- Buy: Purchase a distressed property below market value.

- Rehab: Fix it up to increase the value and the rent potential.

- Rent: Place a tenant at a rent price that hits the 1% mark of your total cost.

- Refinance: Use a bridge loan or hard money to finish the rehab, then move into a long-term conventional or DSCR loan.

If you are a fix-and-flip investor, the 1% Rule is less relevant to your daily work, but it is essential for your "Exit Strategy B." If the market shifts and you cannot sell the flip, you need to know if the property can work as a rental. If the house doesn't come close to the 1% Rule, you are taking a massive risk if you get stuck holding the property.

Final Thoughts for New Investors

Do not let a property that hits 0.8% or 0.9% scare you away if the location is prime and the expenses are low. Use the 1% Rule to narrow your search, but always perform a deep dive into the actual numbers before signing a contract.

Understanding how to leverage equity through a HELOC or a professional loan process can make the difference between a deal that barely breaks even and one that builds true wealth.

Access the tools you need to evaluate your next deal. Whether you are looking at a multi-unit building in Chicago or a short-term rental in Florida, the right financing structure is the key to success.

Does your deal meet the 1% rule? Contact Ebonie Beaco for financing and mentoring.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664