Tax Benefits of Owning Rental Property: What You Need to Know

Investing in real estate is a proven path to building long-term wealth, but the actual profit often lies in what you keep after taxes rather than just the monthly rent check. Whether you are a landlord in Chicago, a short-term rental host in Florida, or a fix-and-flip investor in California, understanding the tax code is vital for your success. In 2026, the landscape for real estate investors has become even more favorable due to recent legislative updates.

Explore how these tax advantages can transform your investment strategy and help you scale your portfolio with confidence. Accessing these benefits requires a clear understanding of the IRS rules and how they apply to your specific loan types, such as DSCR investor loans or landlord loans.

The Foundation of Rental Property Deductions

When you own a rental property, the IRS views it as a business. This means you can deduct the ordinary and necessary expenses involved in managing, conserving, and maintaining the property. These deductions directly reduce your taxable rental income, which can keep more cash in your pocket for future acquisitions.

Standard Operating Expenses

The day-to-day costs of running a rental property are generally fully deductible. If you are managing a multifamily building in Alabama or a single-family home in Virginia, keep meticulous records of these items:

- Property Taxes: The annual taxes paid to local governments are deductible.

- Insurance Premiums: This includes homeowner’s insurance, flood insurance, and liability coverage.

- Property Management Fees: If you hire a professional to handle your tenants in Georgia, their fees are a write-off.

- Repairs and Maintenance: Routine work like fixing a leak, painting a room, or mowing the lawn.

- Utilities: If you cover the cost of water, gas, or electricity for your tenants.

- Advertising: Costs for listing your property on rental platforms or local media.

Under the "De Minimis Safe Harbor" rule, you can often immediately expense any single invoice under $2,500, such as a new water heater or a small appliance, rather than depreciating it over several years [2].

The Mortgage Interest Deduction

For most investors, the largest recurring deduction is mortgage interest. While you cannot deduct the portion of your payment that goes toward the principal (as that is building your equity), you can deduct the interest paid on loans used to acquire or improve the property.

This applies to various financing structures, including hard money loans, bridge loans, and traditional mortgage basics you might find at Home Loans Network Mortgage Basics. If you have a HELOC (Home Equity Line of Credit) used specifically for property improvements, that interest is typically deductible as well [6].

The Power of Depreciation: The "Paper Loss"

Depreciation is perhaps the most significant tax benefit available to real estate investors. It allows you to deduct the cost of the building over its "useful life," even if the property is actually increasing in market value. For residential rental properties, the IRS sets this period at 27.5 years [4].

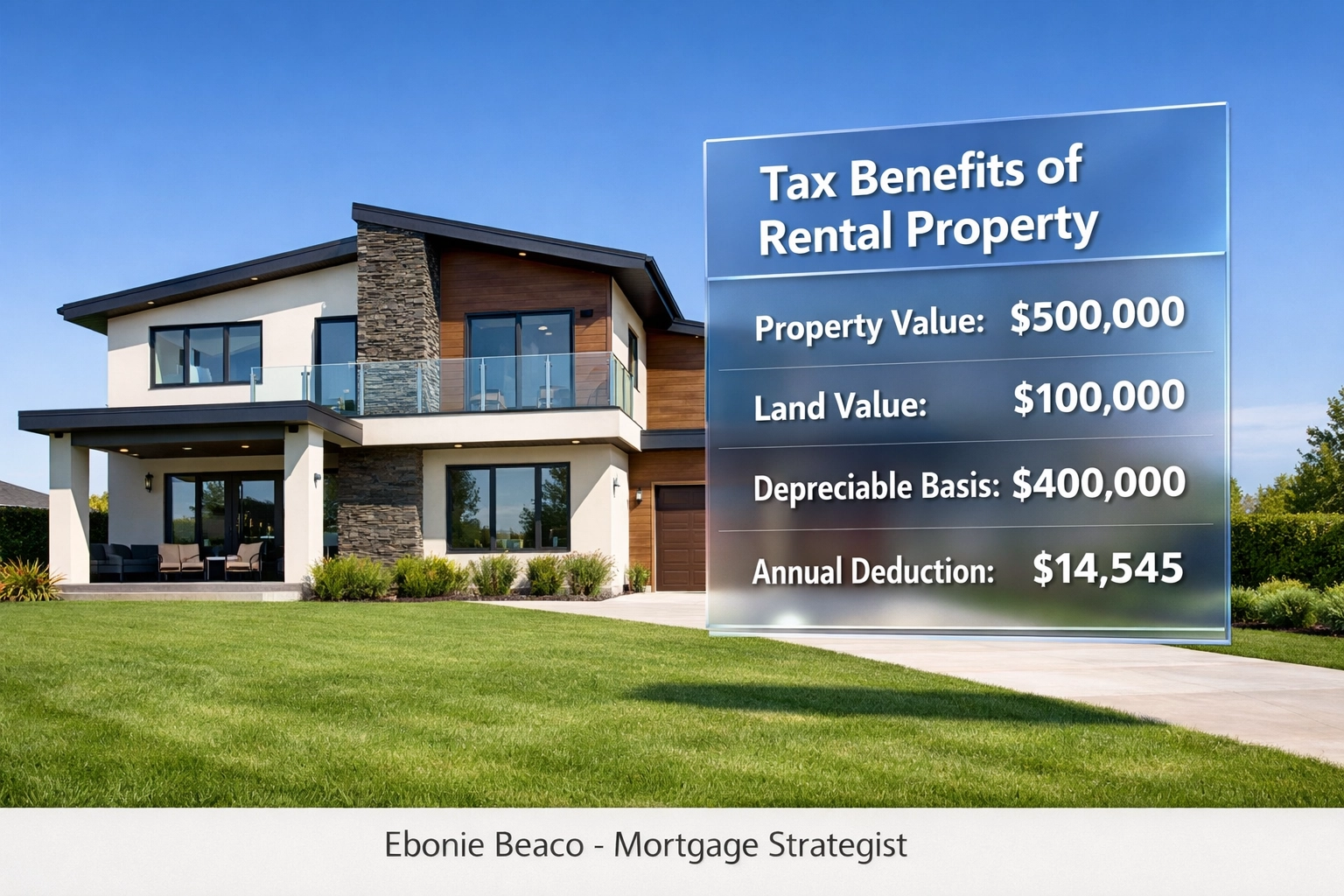

Calculating Your Depreciation Basis

To calculate depreciation, you must first separate the value of the building from the value of the land. Land does not wear out, so it cannot be depreciated.

Example Scenario: Imagine you purchase a rental property in Michigan for $500,000. An appraisal or tax record determines that the land is worth $100,000. This leaves you with a "depreciable basis" of $400,000.

- Purchase Price: $500,000

- Land Value: $100,000

- Depreciable Basis: $400,000

- Annual Deduction: $400,000 / 27.5 years = $14,545

Image Description: A clean financial breakdown chart showing Property Value: $500,000, Land Value: $100,000, Depreciable Basis: $400,000, and Annual Depreciation Deduction: $14,545. The text 'Tax Benefits of Rental Property' is at the top, and 'Ebonie Beaco - Mortgage Loan Officer' is at the bottom.

Image Description: A clean financial breakdown chart showing Property Value: $500,000, Land Value: $100,000, Depreciable Basis: $400,000, and Annual Depreciation Deduction: $14,545. The text 'Tax Benefits of Rental Property' is at the top, and 'Ebonie Beaco - Mortgage Loan Officer' is at the bottom.

This $14,545 is a "paper loss." You didn't actually spend that money this year, but you get to subtract it from your rental income. If your property generated $14,000 in net profit after other expenses, this depreciation deduction would result in a taxable income of zero.

2026 Strategic Advantages: The OBBBA

The current year, 2026, offers unique opportunities due to the One Big Beautiful Bill Act (OBBBA). This legislation has restored and enhanced several key provisions that benefit property owners and real estate investors.

100% Bonus Depreciation

The OBBBA has restored the ability to use 100% bonus depreciation for certain assets [7]. While the structural building is depreciated over 27.5 years, specific items within the property have shorter recovery periods. Investors can use a "cost segregation study" to identify these items and deduct their full cost in the first year.

Common items eligible for accelerated depreciation include:

- 5-Year Property: Appliances, carpeting, furniture, and window treatments.

- 15-Year Property: Fences, sidewalks, driveways, and landscaping.

Jump in and utilize this strategy if you are doing a fix and flip or setting up a new Airbnb in Florida. It can create a massive tax shield in your first year of ownership.

Qualified Business Income (QBI) Deduction

The QBI deduction, also known as Section 199A, allows eligible landlords to deduct up to 20% of their net rental income from their overall taxable income [1]. This deduction is a powerful tool for those who operate their rentals as a business, providing a significant reduction in the effective tax rate on rental profits.

How Financing Strategies Impact Your Taxes

The way you finance your property can change your tax outlook. Different loan programs offered by Home Loans Network cater to different investor needs.

DSCR Investor Loans

DSCR (Debt Service Coverage Ratio) loans are popular because they qualify you based on the property’s income rather than your personal debt-to-income ratio. From a tax perspective, the interest on these loans is a primary deduction. Because DSCR loans often have slightly higher interest rates than traditional owner-occupied loans, the interest deduction is even more substantial.

Cash-Out Refinance

Many investors use a cash-out refinance to pull equity from one property to buy another. The interest on the portion of the new loan used for business purposes (like buying a new rental in Indiana or Missouri) remains deductible. You can explore your options for this strategy at Home Loans Network Refinance.

Bank Statement Loans

For self-employed investors who have many write-offs, qualifying for a traditional loan can be difficult. Bank statement loans allow you to qualify based on deposits rather than tax returns. This is a great way to maintain your aggressive tax deductions while still accessing the capital you need to grow your portfolio.

The Catch: Depreciation Recapture

Transparency is key in real estate finance. While depreciation provides amazing benefits while you own the property, the IRS will want some of that back when you sell. This is known as "depreciation recapture."

The IRS taxes the total depreciation you claimed (or could have claimed) at a flat rate of 25% upon the sale of the property [1].

Example: If you claimed $50,000 in depreciation over five years, when you sell, you may owe $12,500 in recapture tax.

To defer this, many investors use a 1031 Exchange, which allows you to reinvest the proceeds from a sale into a "like-kind" property without immediately paying capital gains or recapture taxes. This is a common tactic for investors building large portfolios across Kentucky, Arkansas, and beyond.

Practical Steps to Maximize Your Benefits

To ensure you are getting every dollar you deserve, follow these simple guidelines:

- Keep Digital Records: Use apps or software to track every receipt, from a box of nails to a property management invoice.

- Request Amortization Schedules: Ask your lender for a full schedule so you can accurately separate interest from principal for your tax preparer. You can use our mortgage calculators to get an idea of these figures.

- Consult a Professional: Real estate tax law is complex. Always work with a CPA who specializes in real estate.

- Distinguish Repairs vs. Improvements: Repairs (fixing what is broken) are deducted immediately. Improvements (adding value or extending life) are depreciated over time.

Compare your current financing to see if a different structure could provide better tax or cash flow results. Whether you are a seasoned pro or just starting your journey, the right mortgage strategy is the engine that drives your investment vehicle.

Ready to Grow Your Portfolio?

The world of real estate finance is full of opportunities to save on taxes and increase your net worth. Navigating landlord loans, fix and flip financing, and DSCR rental property loans requires a strategist who understands the nuances of the market.

Contact Ebonie Beaco for mortgage advice or mentoring at www.homeloansnetwork.com.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664