Sunday Market Pulse: Why This Week’s Rate Shifts Impact Your June Home Search

Ebonie Beaco - Mortgage Strategist

As we transition into June 2026, the mortgage market continues to present a landscape of both challenge and opportunity for proactive participants. This final Sunday of May has revealed a stabilized yet elevated rate environment, with the 30-year fixed mortgage settling between 6.3% and 6.6% for well-qualified borrowers. For individuals across Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia, understanding these subtle shifts is crucial for timing your next acquisition or refinance.

The Current Rate Environment

Today, May 31, 2026, the national average for a 30-year conforming loan is approximately 6.56%, reflecting a slight uptick from earlier in the spring. While rates have faced upward pressure due to persistent inflation data, the overall housing market is entering a "cooling phase" that may benefit buyers who felt priced out during previous bidding wars. Explore the current trends to see how these numbers align with your long-term financial objectives.

Ebonie Beaco - Mortgage Strategist

Jump in and compare the primary loan products available this week to determine which fits your profile:

- 30-Year Fixed Rate: A mortgage with a constant interest rate and monthly payment for the full three-decade term. This offers long-term predictability and protection against future rate hikes.

- 15-Year Fixed Rate: A loan that fully amortizes over 15 years, typically offering a lower interest rate than the 30-year counterpart. You can access rates between 5.8% and 6.0% today with this product.

- Adjustable-Rate Mortgage (ARM): A loan where the interest rate changes periodically after an initial fixed period. Approximately 10% of current applications are ARMs as borrowers seek lower initial payments in this high-rate climate.

Strategies for Homeowners and Investors

Homeowners in metropolitan areas like Chicago or Northern Virginia often utilize their property's equity to fuel further investments. A Cash-Out Refinance allows you to replace your existing mortgage with a new one for a larger amount than you owe, taking the difference in cash. This is a common strategy for funding major renovations or consolidating high-interest debt.

Accessing equity through a HELOC (Home Equity Line of Credit) provides a revolving credit line secured by your home's value. Unlike a one-time loan, a HELOC functions more like a credit card, allowing you to draw funds as needed for property improvements or down payments on new acquisitions. Compare these options with our mortgage calculators to see your potential borrowing power.

Ebonie Beaco - Mortgage Strategist

Real Estate Investment Analysis

For the real estate investor, the DSCR (Debt Service Coverage Ratio) Loan remains the gold standard for scaling portfolios without relying on personal income.

- DSCR Loan: A financing solution that qualifies borrowers based on the rental income generated by the property rather than personal W-2 earnings. It ensures the property's cash flow can comfortably cover its debt obligations.

- Fix and Flip Financing: Short-term bridge loans used to acquire and renovate distressed properties with the intent of a quick resale.

- Short-Term Rental (STR) Loans: Specifically designed for Airbnb or VRBO operators who need to leverage projected nightly rental income for qualification.

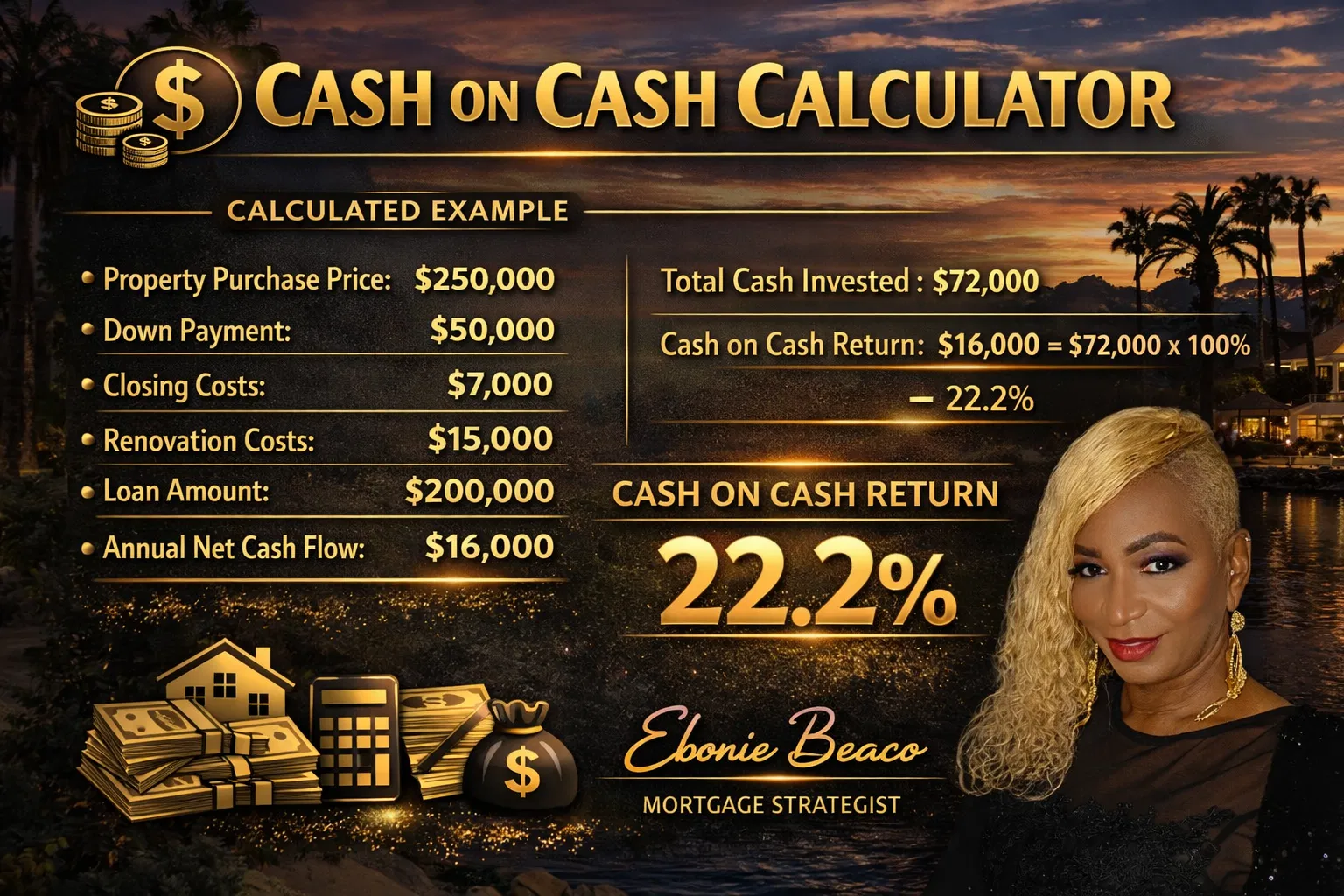

Consider a practical example in a market like Atlanta, Georgia. An investor identifies a duplex valued at $500,000 with a monthly rental income of $4,500. By applying a DSCR calculation, the lender analyzes if that $4,500 covers the principal, interest, taxes, insurance, and association fees (PITIA). If the ratio is 1.2 or higher, the deal is often viewed as a strong candidate for funding.

Ebonie Beaco - Mortgage Strategist

Regional Market Insights

The California market is currently seeing a "buyer-tilted" shift in several coastal metros, with price growth slowing to near-flat levels. This provides a rare window for buyers to negotiate seller concessions or repairs that were impossible a year ago. Conversely, Midwest markets in Indiana and Michigan remain remarkably stable due to their inherent affordability compared to the national average.

In Florida, investors are navigating higher insurance costs by prioritizing Non-QM (Non-Qualified Mortgage) products. These loans cater to self-employed borrowers or those with complex financial profiles who do not meet traditional agency guidelines. Explore our loan programs to find specialized solutions for unique property types, including mixed-use and commercial buildings.

Navigating the June Market

As you prepare for your June home search, remember that the "sticker price" of an interest rate is only one part of the equation. Strategic financing involves aligning your loan structure with your 5-year and 10-year wealth-building goals. Whether you are a first-time homebuyer in Alabama or a seasoned landlord in Missouri, clear guidance helps resolve the uncertainty of fluctuating markets.

We offer professional support for a wide range of scenarios, from ITIN loans for international investors to Bridge Loans for those buying a new home before selling their current one. Our commitment to education ensures you understand the "why" behind every recommendation.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664