Sunday Market Brief: Mortgage Rate Trends Explained in Under 3 Minutes (May 31 Edition)

As we wrap up the final day of May 2026, the mortgage market continues to display a high degree of sensitivity to shifting economic data and geopolitical tensions. For homeowners, realtors, and investors across states like Alabama, Florida, and Illinois, staying informed is the first step in making sound financial decisions. The current landscape is defined by a slight upward pressure that has pushed rates away from the local lows we saw earlier this year. This brief provides a clear snapshot of where we stand today and how these trends impact your purchasing power or investment strategy. You can explore our specific loan programs to see how these current figures translate into real-world monthly payments.

The National Average and Current Mortgage Figures

The 30-year fixed-rate mortgage remains the most popular choice for homebuyers and currently averages approximately 6.56 percent as of this morning. This figure represents a minor increase from four weeks ago when rates were hovering closer to 6.37 percent. Meanwhile, the 15-year fixed-rate mortgage is holding steady around 5.84 percent, offering a lower interest cost for those who can manage a higher monthly payment. These shifts are largely attributed to sticky inflation reports and rising oil prices that have kept the Federal Reserve in a cautious stance. While some had hoped for a return to the 5 percent range by mid-year, most economists now expect rates to stabilize in this mid-6 percent zone for the foreseeable future.

Regional Realities Across the Housing Market

While national averages provide a useful baseline, real estate activity is deeply localized in markets like Chicago, Atlanta, and various cities throughout California. In high-demand areas of Florida and Virginia, inventory remains tight, which often counteracts the cooling effect of higher interest rates. Investors in Arkansas and Indiana are seeing a steady demand for rental units, making the cost of financing a secondary consideration to the overall yield of the property. For those in Michigan or Missouri, the current rate environment makes it essential to work with a strategist who understands how to navigate conventional loans and alternative products. Understanding your local market dynamics allows you to adjust your offer strategies and stay competitive even when the broader headlines seem challenging.

Strategic Moves for Real Estate Investors

Real estate investors, particularly those operating Airbnb or short-term rental portfolios, are increasingly turning toward DSCR Investor Loans. These loans focus on the cash flow of the property itself rather than the personal income of the borrower, which is a major advantage for scaling a portfolio quickly. In states like Georgia and Alabama, where vacation rentals and long-term holds are thriving, the Debt Service Coverage Ratio is a critical metric for qualification. By using the rental income to cover the mortgage debt, you can continue to acquire properties without being limited by your personal debt-to-income ratio. If you are a fix and flip investor or a wholesaler in the California market, these specialized lending products provide the flexibility needed to close deals fast.

The Power of Equity and Strategic Refinancing

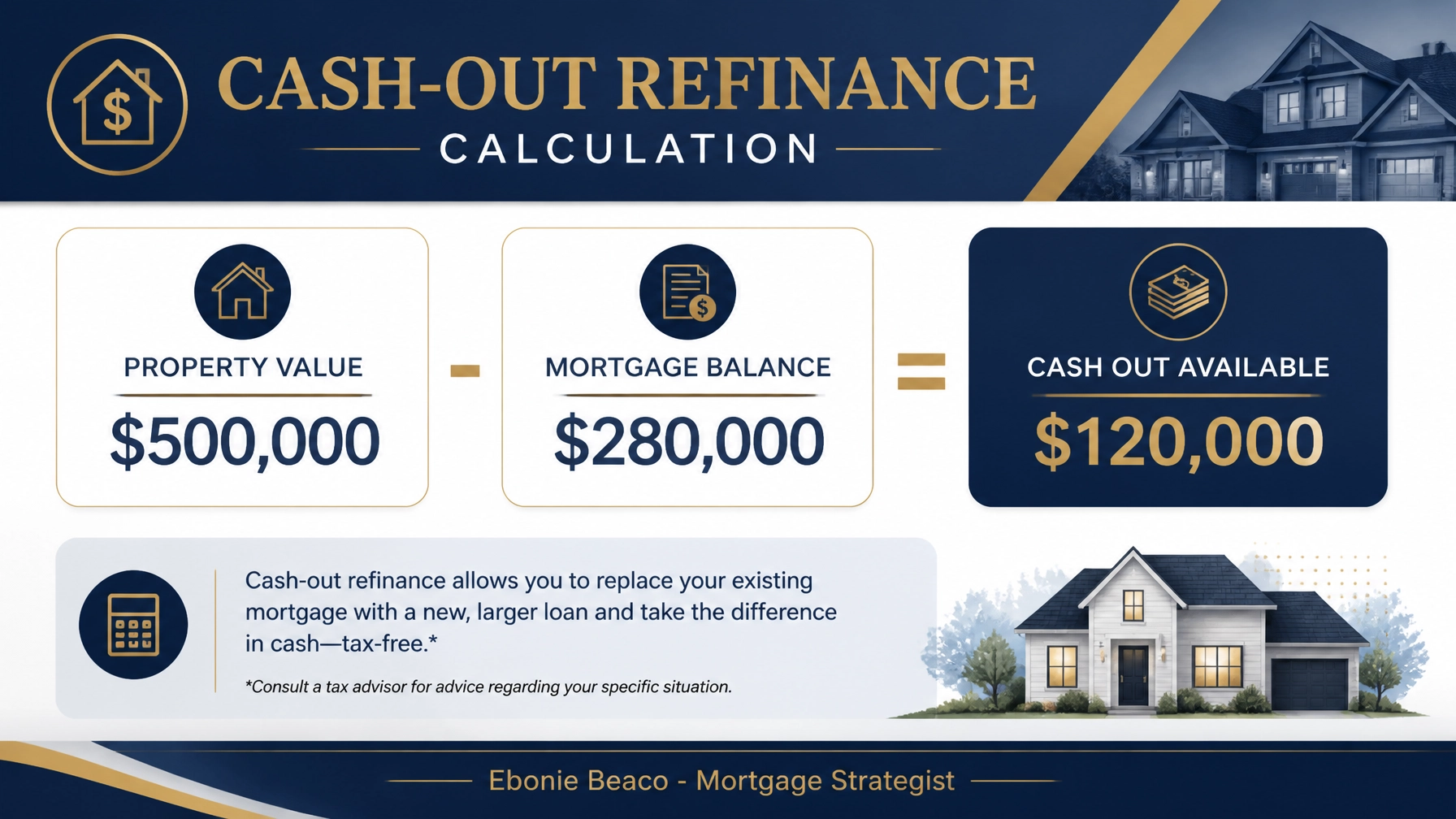

Homeowners who have seen significant appreciation over the last few years are now looking at Cash-Out Refinance and HELOC options to fuel their next move. A cash-out refinance allows you to replace your current mortgage with a new one for more than you owe, taking the difference in cash. This strategy is particularly effective for debt consolidation or for funding the down payment on an investment property. Alternatively, a Home Equity Line of Credit (HELOC) provides a revolving line of credit that you can draw from as needed, similar to a credit card but with lower interest rates. Accessing your equity strategically can help you build wealth without waiting for the next major rate drop.

A Practical Financial Example:

Imagine an investor in Virginia owns a duplex valued at $500,000 with a current mortgage balance of $280,000. Using a cash-out refinance at 75 percent loan-to-value (LTV), the total new loan amount would be $375,000. After paying off the existing $280,000 mortgage and estimated closing costs, the investor could walk away with roughly $85,000 to $90,000 in liquid cash. This capital can then be deployed for renovations to increase the rental yield or as a down payment for a new acquisition. Calculations like these show how the strategic use of equity can be more influential than the interest rate itself.

Looking Ahead to June 2026

As we move into June, all eyes will be on the mid-month Federal Open Market Committee (FOMC) meeting. While the Federal Reserve does not directly set mortgage rates, their policy decisions regarding the federal funds rate strongly influence the 10-year Treasury yield, which is the benchmark for home loans. We expect to see relative stability with daily fluctuations, which professionals often call "market wiggles." This stability provides a window of opportunity for buyers to lock in rates before any potential volatility later in the summer. Jump in and review our FAQ to understand how these upcoming changes might affect your specific scenario.

Navigating the Market with Confidence

The current mortgage environment requires a shift in perspective from waiting for rates to fall to finding the best strategy for the current numbers. Whether you are a first-time homebuyer in Kentucky or a seasoned landlord in Alabama, the right financing structure can make a significant difference in your long-term success. We are committed to providing transparent guidance and educational resources to help you achieve your homeownership goals. If you have questions about how a bridge loan or a bank statement loan might work for your business, we are here to provide the clarity you need. Explore your options today and take control of your financial future in the real estate market.

Access detailed insights and start your journey today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664