Strategic Financing for Wholesalers: Moving Deals in a 6% interest rate world

As of March 25, 2026, the real estate landscape has shifted into a phase of calculated stability. The days of sub-3% rates are a distant memory, and the "wait-and-see" approach of 2024 and 2025 has transitioned into a "deal-flow-at-any-cost" mentality. For wholesalers operating in high-velocity markets like Alabama, Florida, Georgia, and Illinois, the challenge isn't just finding the deal anymore, it is ensuring the end-buyer has the capital to cross the finish line.

The current 10-year Treasury yields have kept mortgage rates hovering between 6.3% and 6.5%. According to recent data from HousingWire, this environment requires a higher level of financial sophistication from everyone involved in the transaction. If you are wholesaling properties, you are no longer just a scout; you must act as a preliminary underwriter.

To keep your assignment fees flowing, you must understand how your buyers are funding these acquisitions. If your buyer’s financing falls through, your contract expires, and your reputation in the market takes a hit.

The 2026 Wholesale Bottleneck: Why Deals are Stalling

The primary reason wholesale deals fall apart in today's market is a lack of "financing alignment." Many wholesalers still target "cash buyers" who are, in reality, "leveraged buyers." These investors rely on hard money or private capital to close. When rates sit at 6.5%, the cost of that private capital often jumps to 10% or 12%, squeezing the margins on a fix-and-flip or a rental acquisition.

As a mortgage strategist, I see the friction points daily. Wholesalers in Michigan, Indiana, and Missouri are finding that their old buyer lists are thinning out. The investors who were active in 2021 are not necessarily the ones who can perform in 2026. You need buyers who utilize specialized investment products that bypass traditional banking hurdles.

Modern office scene with real estate professionals analyzing deal structures on a laptop. Ebonie Beaco - Mortgage Strategist

Modern office scene with real estate professionals analyzing deal structures on a laptop. Ebonie Beaco - Mortgage Strategist

Strategic Tool: The DSCR Loan

DSCR (Debt Service Coverage Ratio): A mortgage loan for investment properties that relies on the property's rental income rather than the borrower's personal income or debt-to-income ratio. Practical Application: This allows your end-buyer to qualify for a loan based on the property’s ability to pay for itself, which is essential for scaling a portfolio quickly without hitting personal lending limits.

For wholesalers in Georgia and Virginia, pointing your buyers toward DSCR loans is a game-changer. Since these loans do not require tax returns or employment verification, the closing timeline is significantly faster than a conventional loan. If you have a deal under contract, you should ask your buyer, "Is this property going to hit a 1.2 DSCR?" If the answer is yes, the deal is move-able even at 6.5% interest.

Explore how DSCR investor loans can facilitate faster exits for your wholesale inventory.

The Role of Bridge Financing in High-Rate Environments

Bridge Loan: A short-term, interest-only loan used to "bridge" the gap between the purchase of a property and its eventual renovation, sale, or long-term refinance. Practical Application: Wholesalers can use bridge financing to facilitate "wholetailing" or to give their buyers 12 months of breathing room to stabilize a property before moving into a permanent DSCR or conventional loan.

In states like Arkansas and Kentucky, where property values allow for significant "fix-and-flip" margins, bridge loans are the lifeblood of the industry. As a strategist, I recommend wholesalers vet their buyers for "liquidity depth." Does your buyer have the 15% to 20% down payment required for a bridge loan? If they don't, they aren't a buyer; they are a liability to your contract.

Geographic Nuances: From the Midwest to the Southeast

The strategy for moving a deal in Chicago, Illinois, differs greatly from moving one in Birmingham, Alabama.

The Midwest Strategy (IL, IN, MI, MO)

In markets like Indiana and Missouri, cash flow is the primary driver. Investors here are looking for high yields. To move a wholesale deal in these regions, you must present a "pro-forma" that accounts for a 6.5% interest rate. If the deal still nets a 10% cap rate after financing, your buyers will compete for it.

The Southeast Strategy (AL, FL, GA, VA)

Florida and Georgia remain appreciation-heavy markets. However, with higher carrying costs, your buyers need "interest-only" options to keep their monthly cash flow positive during the initial phases of the investment. Mentioning interest-only mortgage options to your buyer list can make a "tight" deal look much more attractive.

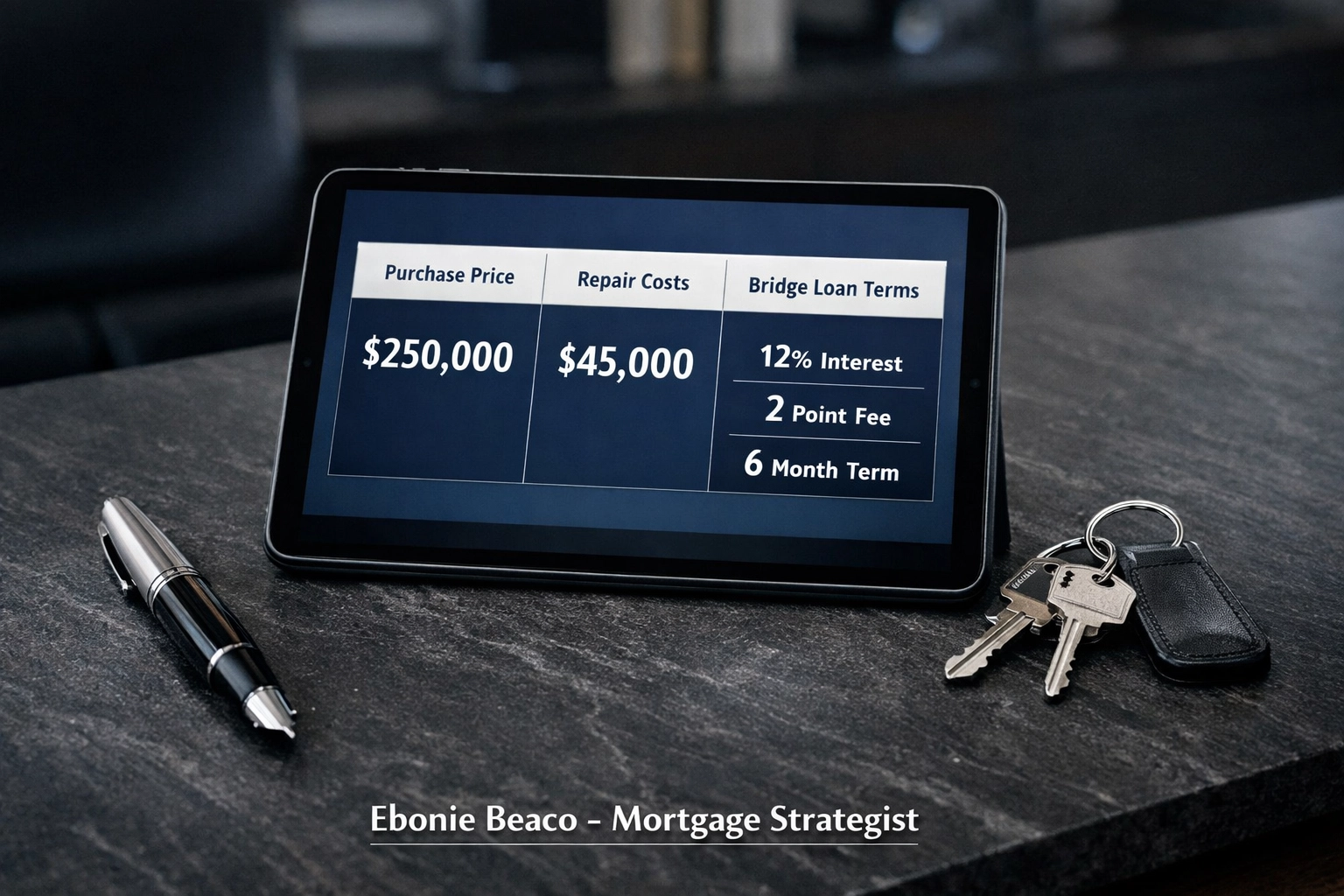

Real-World Deal Breakdown: The Wholesaler’s Math

Let's look at a practical example of how a wholesaler should structure a deal for an investor in 2026. Imagine a single-family home in Virginia with an After Repair Value (ARV) of $400,000.

| Category | Figure |

|---|---|

| Purchase Price (Wholesale) | $260,000 |

| Estimated Repairs | $50,000 |

| Closing/Holding Costs | $15,000 |

| Loan Amount (80% LTV Bridge) | $208,000 |

| Interest Rate (Bridge) | 9.5% (Interest Only) |

| Monthly Carrying Cost | $1,646 |

Financial breakdown chart showing the relationship between purchase price, repair costs, and bridge loan payments. Ebonie Beaco - Mortgage Strategist

Financial breakdown chart showing the relationship between purchase price, repair costs, and bridge loan payments. Ebonie Beaco - Mortgage Strategist

By providing this level of detail to your buyer, you demonstrate that you understand the Debt Service implications of the current rate environment. You aren't just selling a house; you are selling a vetted financial vehicle. Access our mortgage calculators to run these numbers for your buyers before you blast your email list.

Pre-Screening Your Buyer List

As a mortgage strategist, I advise wholesalers to categorize their buyers based on their "funding DNA."

- The Cash Whale: Doesn't care about rates, but wants a deep discount.

- The DSCR Scaler: Needs properties that meet a 1.1 or 1.2 coverage ratio.

- The Rehabber: Lives and dies by the bridge loan and the "ARV" (After Repair Value).

If you are working in Kentucky or Michigan, your "DSCR Scalers" are your most reliable exit strategy. They are looking for long-term holds and are less sensitive to short-term market fluctuations. Ensure they have a relationship with a strategist who can handle non-QM mortgage loans so they don't get stuck in the middle of your transaction.

The "Wholesaling to Yourself" Strategy: BRRRR

Sometimes, the best buyer for your wholesale deal is you. If a deal is too good to pass off for a $10,000 assignment fee, consider the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

In 2026, the "Refinance" step is the most critical. You need to ensure that after you put the work into a property in Alabama or Arkansas, you can execute a cash-out refinance to pull your initial capital back out.

Jump in and explore our loan process to see how we help investors transition from short-term bridge loans to long-term wealth-building debt.

Final Strategy: Velocity Over Margin

In a 6% rate world, the cost of time is high. Every month a property sits vacant or a contract remains unassigned, the "yield" erodes. Wholesalers who succeed in 2026 are those who prioritize "Velocity of Capital."

Partnering with a mortgage strategist allows you to offer your buyers "pre-vetted" financing scenarios. When you send out your next deal alert in Florida or Virginia, include a note that says: "Financing available for this deal: 80% LTV Bridge or 1.2 DSCR Long-term."

This small addition shifts the buyer’s mindset from "Can I afford this?" to "How soon can I close?"

Compare your current exit strategies with the financing options available at Home Loans Network.

Partner for Faster Exits

If you are a Realtor, Investor, or Wholesaler in AL, AR, GA, FL, IL, IN, MI, KY, MO, or VA, stop letting your deals die at the closing table. Let’s structure your buyers' financing before the contract is even signed.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664