Stop Wasting Money on Interest: The Simple HELOC Trick for Homeowners from Virginia to Michigan

If you have been watching your credit card statements lately, you probably noticed something painful. Those interest rates are creeping up, and for many homeowners in states like Michigan, Virginia, and Alabama, the monthly minimum payments feel like they are barely denting the principal balance.

You are essentially paying a "rent" on your own debt, and that rent is at an all-time high.

But there is a strategy that savvy homeowners and real estate investors use to stop the bleeding. It is not a magic trick, but it feels like one when you see your monthly expenses drop by hundreds or even thousands of dollars. It’s called the HELOC debt consolidation strategy.

Whether you are managing a primary residence in Missouri or building a rental portfolio in Florida, understanding how to leverage your home equity is the fastest way to regain control of your cash flow.

The Problem: The High Cost of "Bad" Debt

Before we get into the solution, we need to look at the numbers. Most credit cards today carry interest rates between 18% and 27%. If you are carrying a $30,000 balance at 22%, you are paying over $500 a month just in interest. That money is gone forever. It doesn’t build equity, it doesn’t improve your credit, and it certainly doesn’t help you retire.

In markets like Chicago or Atlanta, where the cost of living continues to rise, that $500 a month could be the difference between struggling and thriving.

What Exactly is a HELOC?

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home.

Think of a HELOC like a credit card with a massive limit and a much lower interest rate. Because the loan is secured by your property, lenders are willing to offer significantly lower rates than what you find on unsecured personal loans or credit cards.

LTV (Loan-to-Value): The ratio of the total loans on a property compared to its appraised value.

Most lenders allow you to tap into your equity up to an 80% or 85% LTV. For example, if your home in Virginia is worth $500,000 and you owe $300,000 on your first mortgage, you have $200,000 in equity. A HELOC might allow you to access a large portion of that cash to use however you see fit.

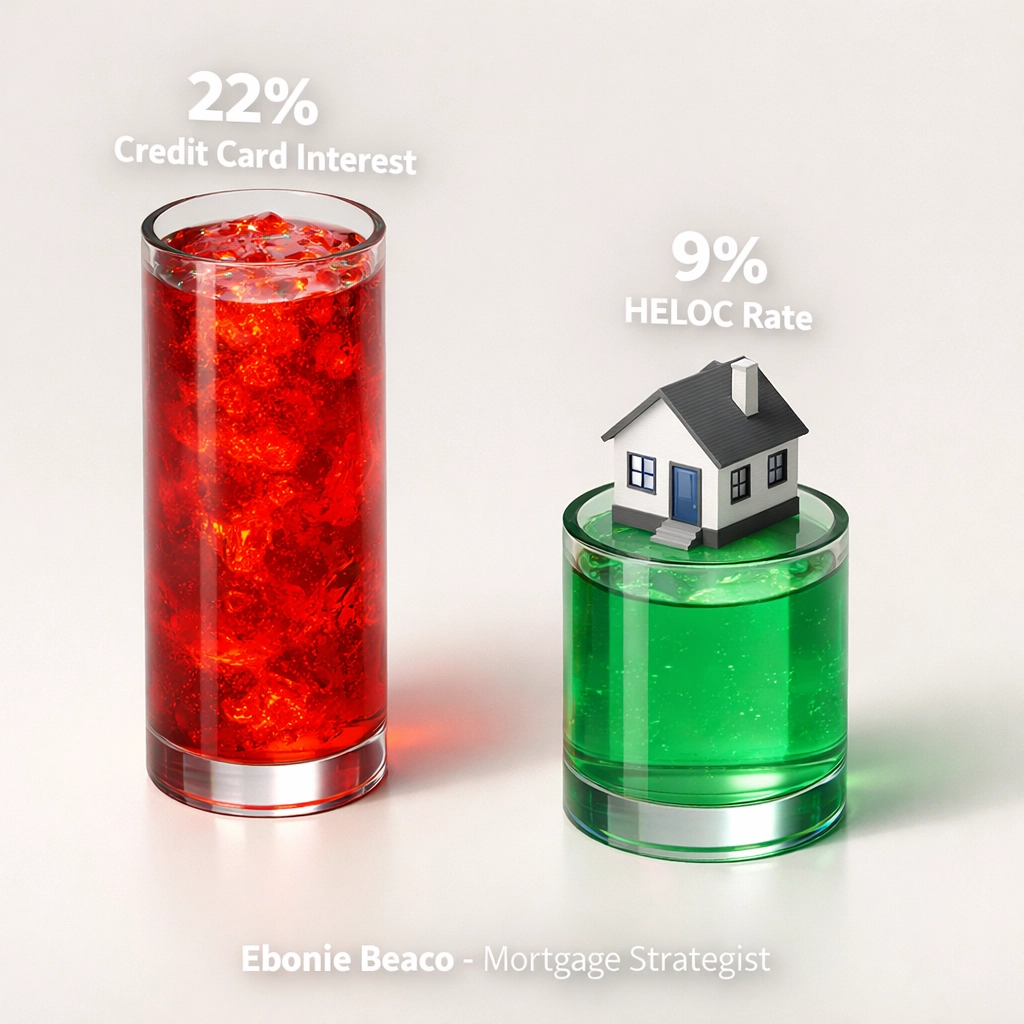

Visual Breakdown: A chart comparing 22% Credit Card Interest vs. 8% HELOC Interest on a $40,000 balance, showing a monthly savings of nearly $460.

The "Simple Trick": Strategic Debt Consolidation

The trick is simple: Use the low-interest HELOC to pay off the high-interest debt.

When you do this, you aren't just moving debt around. You are fundamentally changing the math of your personal economy. By moving $40,000 from a 22% credit card to a 9% HELOC, you immediately reduce your interest expense.

This is why homeowners are searching for a reliable Alabama HELOC lender or a Missouri HELOC lender. They realize that their homes have gained significant value over the last few years, and leaving that equity "trapped" in the walls while paying high interest elsewhere is a massive financial leak.

The Draw Period Advantage

One of the most powerful features of a HELOC is the Draw Period.

Draw Period: The initial phase of a HELOC (usually 10 years) during which you can withdraw funds and often choose to make interest-only payments.

During these first 10 years, your required monthly payment is incredibly low. This gives you the flexibility to take the money you would have spent on high credit card interest and instead put it toward your principal balance or use it for other investments.

Why This Matters from California to Florida

Housing markets vary wildly across the country, but the benefits of a HELOC remain consistent.

- In California and Florida: Home values have skyrocketed. Homeowners in these regions often have six figures of "lazy equity" sitting in their homes. Using a HELOC here can provide the capital needed for home improvements that further increase property value.

- In Michigan and Indiana: Smaller, consistent gains in equity still provide enough "dry powder" to consolidate car loans or student debt, which can be life-changing for families in the Midwest.

- In Virginia and Georgia: Many residents are using HELOCs as a safety net. Since you only pay interest on what you actually draw, having a $50,000 or $100,000 line of credit available costs you nothing until you use it.

For the Investors: The HELOC as an Investment Tool

If you are a landlord or a real estate investor, a HELOC is more than just a way to save on interest: it is a growth engine. Many of our clients use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) and utilize a HELOC for the "Rehab" or "Buy" portion.

Imagine you own a rental property in Kentucky or Arkansas. You can take out a HELOC on your primary residence to fund the down payment on a new investment property. Or, you can use the HELOC to fund a renovation that allows you to increase the rent, subsequently increasing the property's value and allowing for a DSCR (Debt Service Coverage Ratio) loan refinance later.

DSCR Loan: A mortgage for investment properties where qualification is based on the property’s rental income rather than the borrower’s personal income.

Using a HELOC to bridge the gap between acquisition and permanent financing is a classic pro-investor move. It allows you to move quickly on deals without waiting for lengthy traditional loan approvals.

Illustration: A flow chart showing a homeowner using a HELOC to fund a kitchen renovation, which increases the home value by $60,000, creating more equity for future use.

Is a HELOC Better Than a Cash-Out Refinance?

This is a question we get every day at Home Loans Network. The answer depends on your current mortgage rate.

If you bought or refinanced your home in 2020 or 2021, you likely have an interest rate around 3%. If you do a Cash-Out Refinance, you have to refinance your entire loan at today’s higher rates.

Cash-Out Refinance: Replacing your existing mortgage with a new, larger loan and taking the difference in cash.

A HELOC allows you to keep your 3% rate on your first mortgage while only paying today’s rates on the specific amount you borrow from your equity. It is a "surgical" way to get cash without disturbing your low-interest primary mortgage.

For more on the differences, you can check out our Mortgage Basics page.

Potential Tax Benefits

Here is another layer of transparency: If you use your HELOC funds to "buy, build, or substantially improve" the home that secures the loan, the interest may be tax-deductible.

While we always recommend speaking with a tax professional, many homeowners in Illinois and Arkansas find that using a HELOC for a new roof, an ADU, or a kitchen remodel provides a double benefit: increased home value and a potential break at tax time.

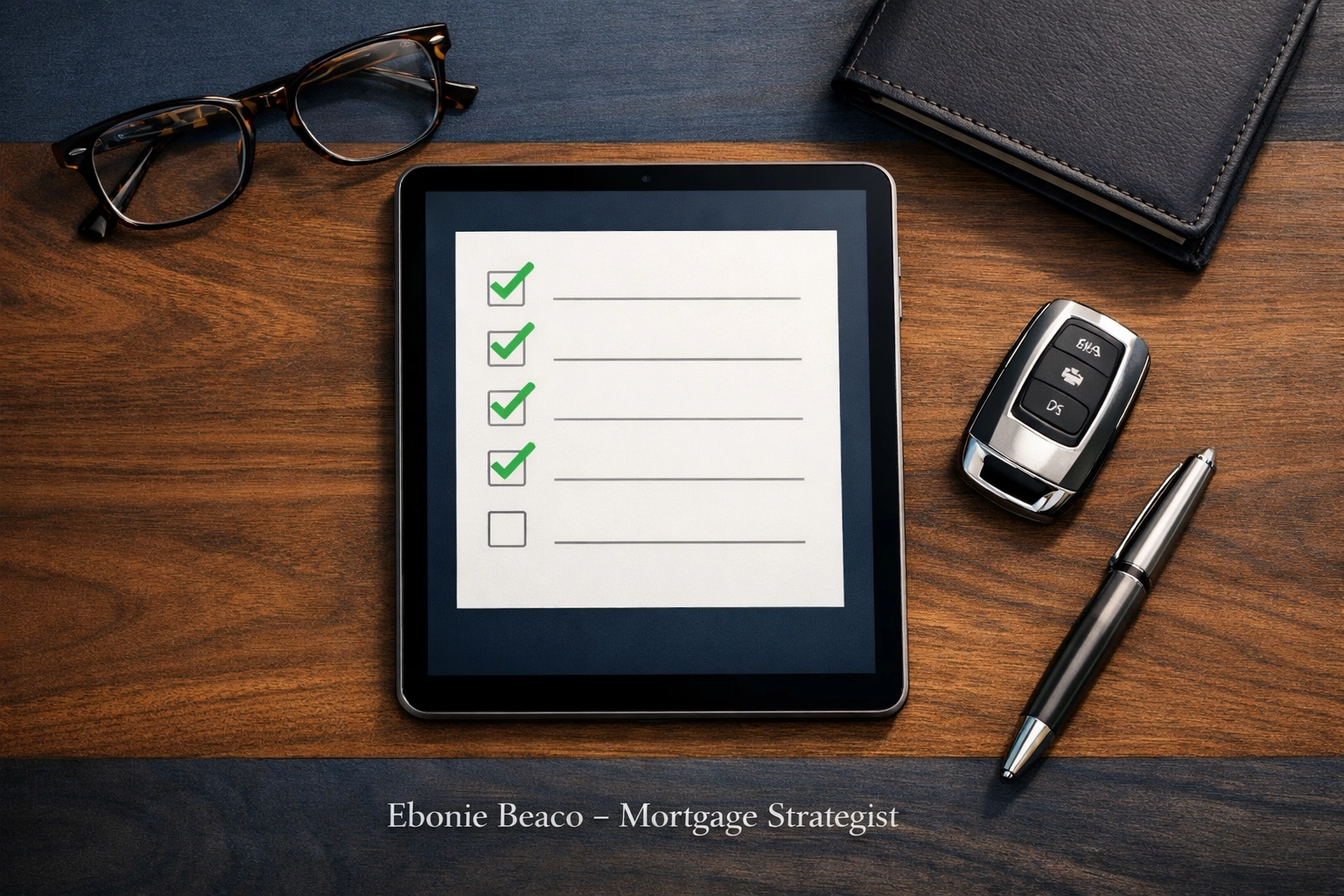

How to Get Started: The Process

Getting a HELOC is generally faster and involves fewer closing costs than a standard mortgage.

- Check Your Equity: You can use our Mortgage Calculators to see how much equity you might be able to tap.

- Gather Your Docs: Think tax returns, pay stubs, and your current mortgage statement.

- Appraisal: The lender will need to verify what your home is worth in today’s market.

- Closing: Once approved, you get access to your line of credit, often via a checkbook or a debit card.

The process is straightforward, but it helps to have a guide who understands the nuances of different states. Whether you need a Missouri HELOC lender or are looking for options in California, we can help you navigate the local requirements.

Graphic: A simple 5-step checklist for the HELOC application process, from initial inquiry to funding.

Real Scenario: The "Interest-Only" Relief

Let’s look at a real-world example from a client in Alabama.

They had $45,000 in credit card debt with a combined monthly payment of $1,400. Most of that was going toward interest. By opening a HELOC at 9%, their interest-only payment during the draw period dropped to approximately $337 per month.

That freed up over $1,000 a month in their budget. They didn't spend that extra $1,000; they used it to pay down the $45,000 principal balance on the HELOC. Because they weren't fighting 22% interest anymore, they were able to pay off the entire $45,000 in less than four years.

That is how you stop wasting money on interest and start building wealth.

Ready to Stop the Bleeding?

You don't have to keep feeling like you are running on a treadmill with your debt. Your home is likely your largest asset: it’s time to make it work for you.

At Home Loans Network, we pride ourselves on being transparent. We will tell you if a HELOC makes sense for your specific situation or if another product, like a Jumbo Loan or an Interest-Only Mortgage, would serve you better.

If you are a homeowner in AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, or VA, let's look at the numbers together.

Stop letting interest eat your future.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664