Stop Using Your Own Cash: How New Investors are Funding 2026 Flips with Zero Down

The real estate market of 2026 has shifted the way investors approach property acquisitions. Margins can still be strong, but they usually come from better underwriting, tighter renovation budgets, and a disciplined exit strategy. For a new investor, the biggest question is often simple: How do you fund a flip without tying up all your cash?

The answer starts with understanding how fix-and-flip financing is built. These loans are usually based on the property's current value, its projected After Repair Value (ARV), your renovation scope, and the lender's maximum leverage. Instead of relying only on your savings, you use short-term capital designed for acquisition and rehab.

The 2026 Market: Why Deal Selection is Critical

The 2026 market has created a more selective environment for flippers. Elevated borrowing costs, uneven home price growth, and tighter resale timelines mean investors need cleaner numbers on the front end. According to market reporting from HousingWire and housing inventory trends tracked by the National Association of Realtors, local conditions continue to vary widely across metros.

That variation is important if you are investing in places like Chicago, Indianapolis, Detroit, Atlanta, Birmingham, Little Rock, Orlando, Tampa, Miami, Los Angeles, Sacramento, Richmond, or Northern Virginia. Some neighborhoods still reward well-executed cosmetic rehabs. Others require more conservative offers because resale velocity has slowed.

In practical terms, new investors should focus on properties with a clear value-add path. That usually means buying below neighborhood retail pricing, avoiding over-improvement, and staying in price ranges where end-buyer demand remains active. In many markets, that still points to entry-level and mid-range homes rather than luxury inventory.

Speed and certainty also remain useful advantages. A fix-and-flip lender can often close much faster than a traditional owner-occupant mortgage, which can help when you are competing for distressed listings, estate sales, or properties that need immediate repairs.

Understanding ARV: The North Star of Your Deal

After Repair Value (ARV): The projected market value of a property after planned renovations are completed.

In practice, ARV helps you estimate the resale ceiling of the deal. It gives you a benchmark for pricing, renovation scope, and loan sizing.

Your ARV should come from recent sold comparables, not active listings or optimistic guesses. Look for renovated comps within a tight radius, ideally closed within the last 3 to 6 months. Match for square footage, bed and bath count, lot type, garage, condition, and neighborhood appeal.

If a property is in Chicago, for example, the right comp may be only a few blocks away rather than a mile away because block-by-block pricing can shift quickly. In suburban Florida or parts of Georgia, the comp radius may stretch farther, but condition and school district still carry weight. The more precise your comp set, the more reliable your ARV.

A common beginner mistake is using the highest sale in the neighborhood as the target value. A stronger approach is to use a realistic retail number supported by multiple sold comps. Conservative ARV assumptions usually create better decisions.

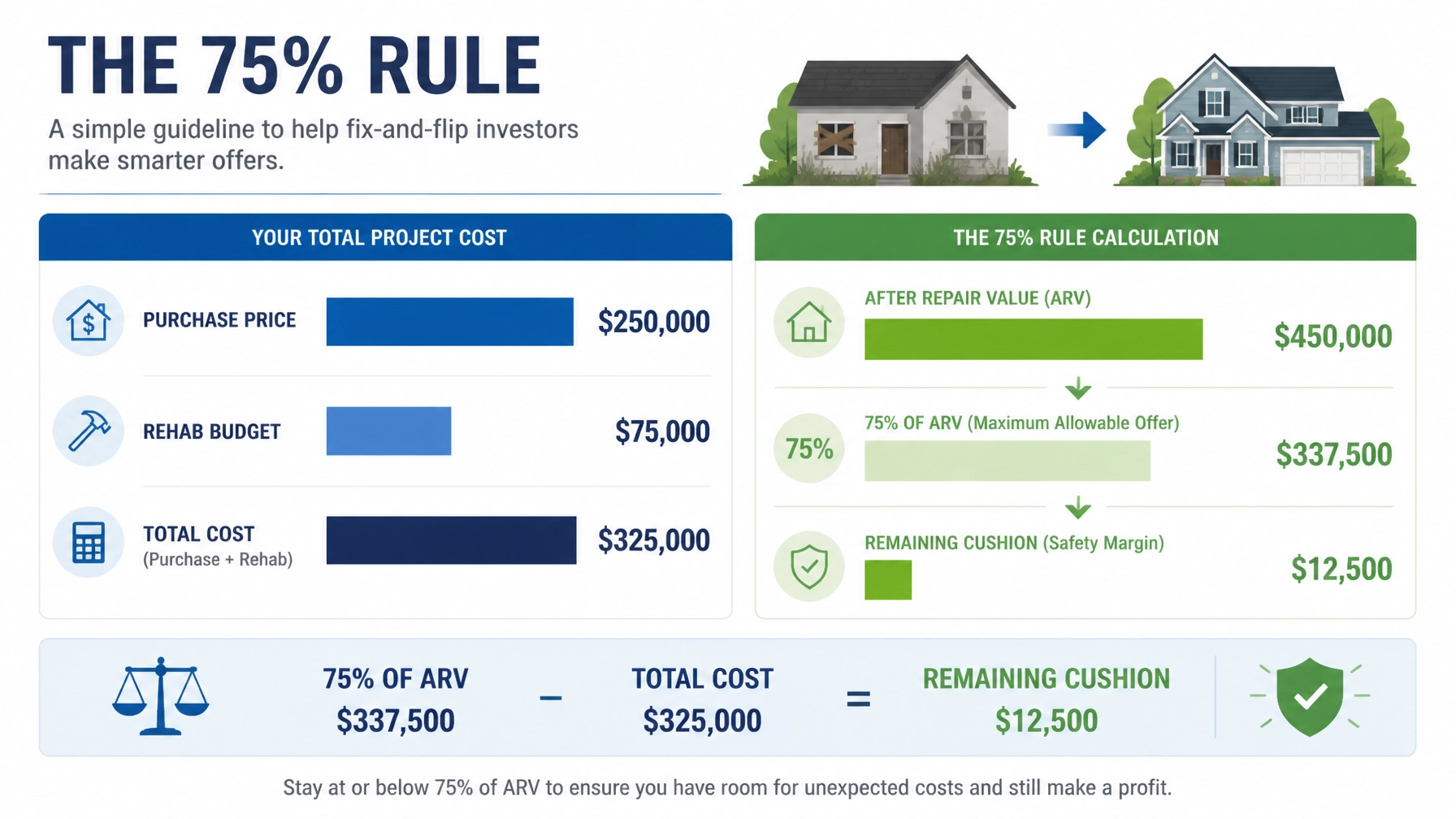

The 75% Rule: Your Safeguard Against Loss

Many lenders and investors use the 75% Rule as a quick screening tool for fix-and-flip deals.

The 75% Rule: A guideline stating that your total project cost, including purchase and rehab, should stay at or below 75% of the property's ARV.

In practice, the rule creates a built-in cushion. That cushion helps absorb financing costs, selling expenses, holding costs, and the risk that the property sells for less than expected.

Here is how it works in plain language:

If a home's ARV is $450,000, then 75% of ARV is $337,500.

If your purchase price is $250,000 and your rehab budget is $75,000, your total project cost is $325,000.

That puts you $12,500 below the 75% threshold.

This does not guarantee a profit. It simply tells you the deal is still within a leverage range many lenders view as more manageable. If your purchase and rehab total rises too close to the ARV, your margin can disappear quickly once interest, taxes, insurance, utilities, agent commissions, and transfer costs are added.

Financial Example: Leveraging a $450,000 Flip

Let's look at how the numbers can work in a realistic scenario for a new investor reviewing a first or second project.

- Purchase Price: $250,000

- Renovation Budget: $75,000

- After Repair Value (ARV): $450,000

- Total Project Cost: $325,000

- 75% of ARV: $337,500

At a high level, the deal fits the 75% rule because the total cost of $325,000 stays below the $337,500 threshold.

Now assume your lender offers:

- Loan for Purchase (90% of $250,000): $225,000

- Loan for Rehab (100% of $75,000): $75,000

- Total Loan Amount: $300,000

- Your Cash Contribution Toward Purchase: $25,000

- Closing Costs, Interest Reserves, and Carrying Costs: Separate and still important to budget for

This is why the phrase "zero down" can be misleading for new investors. In some structures, you may bring very little cash to closing, especially with partner capital or additional gap funding. But most first-time flippers should expect to contribute some funds, and they should always budget beyond the down payment alone.

A better mindset is this: use leverage to preserve liquidity, not to ignore risk. The strongest deals usually work even when you include conservative resale assumptions and a realistic holding period.

The Mechanics of Funding: Holdbacks and Draws

When you close on a fix-and-flip loan, the full renovation budget is usually not wired to you on day one. Instead, lenders often use a Rehab Holdback structure.

Rehab Holdback: A portion of loan proceeds reserved for renovation work and released in stages after verified progress.

In practice, this helps the lender control project risk and helps keep the rehab tied to the approved scope of work.

The Draw Process:

- Work Completion: You or your contractor complete a defined phase of work.

- Inspection or Review: The lender confirms the completed work matches the approved budget and timeline.

- Fund Release: The lender issues a draw to reimburse completed work or fund the next phase, depending on program guidelines.

For new investors, this system creates one important planning issue: timing. Contractors often want deposits, material suppliers want payment, and draw reimbursements are not always instant. That is why you should build in cash reserves for permits, change orders, and short-term project float.

Hard Money vs. Bridge Loans

Most flippers use Hard Money Loans or Bridge Loans because both are built for short-term real estate projects.

Hard Money Loan: A short-term, asset-based loan that relies heavily on the property's value, project scope, and exit strategy.

In practice, hard money is often used when a property needs repairs, a fast closing, or flexible underwriting.

Bridge Loan: A temporary loan used to carry a property until it is sold or refinanced into longer-term financing.

In practice, bridge financing can work well when the investor plans to stabilize the property and then transition into a sale or rental refinance.

These loans are often interest-only during the project term, which can lower monthly payment pressure while the rehab is underway. In 2026, pricing, points, leverage, and reserve requirements can vary widely by lender, borrower experience, and asset type. New investors should compare the full structure, not just the note rate. Origination fees, extension fees, draw fees, appraisal costs, and prepayment terms can all affect the real cost of capital.

Beyond the Flip: The BRRRR Strategy and DSCR Loans

Not every project needs to end with a resale. In 2026, some investors are choosing the BRRRR strategy: Buy, Rehab, Rent, Refinance, Repeat.

That approach can work when resale spreads are thinner but rental demand remains healthy. After renovation, the investor leases the property, then looks at a long-term refinance using a DSCR Investor Loan.

DSCR (Debt Service Coverage Ratio) Loan: An investment property loan that emphasizes the property's cash flow relative to its housing payment.

In practice, DSCR financing can help investors refinance based on rental performance rather than only personal income documents. That can be useful for self-employed borrowers, portfolio investors, and buyers scaling rental properties across markets like Illinois, Indiana, Michigan, Florida, Georgia, and Virginia.

If you want to compare how short-term rehab financing can transition into a longer-term rental strategy, explore our loan programs.

Tips for New Investors in 2026

- Budget for Contingencies: Add a 10% to 15% reserve to your rehab budget for surprises like permit revisions, hidden damage, or contractor change orders.

- Get Pre-Approved: Talk with a lender before you go under contract so you understand leverage limits, liquidity requirements, and expected closing timelines.

- Start with Manageable Scope: For an early flip, cosmetic updates are usually easier to control than full gut rehabs, additions, or heavy structural repairs.

- Underwrite the Exit Clearly: Run the numbers using conservative resale assumptions, realistic days on market, and full holding costs.

- Use Reliable Tools: Access mortgage calculators and deal analysis tools before you commit to a purchase.

Jump In and Scale Your Portfolio

Fix-and-flip financing can be a useful tool for new investors when the numbers are strong and the plan is clear. The key is to understand leverage, respect the ARV, and use the 75% rule as an early filter rather than a shortcut.

Whether you are analyzing your first flip in Chicago, comparing rehab opportunities in Indiana or Michigan, or reviewing rental conversion options in Florida, Georgia, or Virginia, the goal is the same: structure the deal around realistic numbers and a defined exit.

Explore your options and get your deal analyzed clearly and confidently.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664