Should You Buy Investment Properties in an LLC?

Deciding how to hold title to your investment property is one of the first big hurdles you will face as an investor. You might hear seasoned pros in Chicago or investors flipping houses in Florida swear by the Limited Liability Company (LLC) structure. On the other hand, someone just starting with their first rental in Virginia might wonder if the extra paperwork is worth the hassle.

The choice between owning real estate in your personal name or through a business entity impacts your asset protection, your tax strategy, and, most importantly, your financing options.

Explore the reality of using an LLC for real estate and how it affects your ability to scale a portfolio.

Understanding the LLC in Real Estate

Limited Liability Company (LLC): A legal entity that separates your personal identity and assets from your business operations. Practical application: If your rental property is owned by an LLC, the entity acts as a legal "bucket" that holds the property, its income, and its liabilities separate from your personal bank accounts.

When you buy a home for yourself, you generally use your personal name. When you transition into the world of Real Estate Investing, you are essentially starting a business. Treating it like one from day one often means looking into entity formation.

The Primary Benefit: Asset Protection

The most common reason investors choose an LLC is to create a "corporate veil." This legal concept shields your personal assets, like your primary residence, your personal car, and your retirement savings, from lawsuits related to the investment property.

Imagine you own a duplex in Michigan. If a tenant or a guest is injured on that property and decides to sue, they are technically suing the owner of the property. If you own that property personally, your personal assets could be at risk in a judgment. If the LLC owns the property, generally only the assets held within that specific LLC are vulnerable.

Liability Isolation: The strategy of placing each individual property into its own separate LLC to prevent a legal issue with one property from affecting others in your portfolio. Practical application: An investor with five properties in five separate LLCs ensures that a lawsuit on Property A cannot result in a lien against Property B.

Tax Flexibility and Flow-Through Income

One of the best parts about an LLC is its "pass-through" nature. The IRS generally does not tax the LLC itself. Instead, the profits and losses "pass through" to your personal tax return.

This simplicity allows you to take advantage of various deductions without the complexity of double taxation that corporations face. You can typically deduct:

- Mortgage interest

- Property taxes

- Management fees

- Repairs and maintenance

- Depreciation

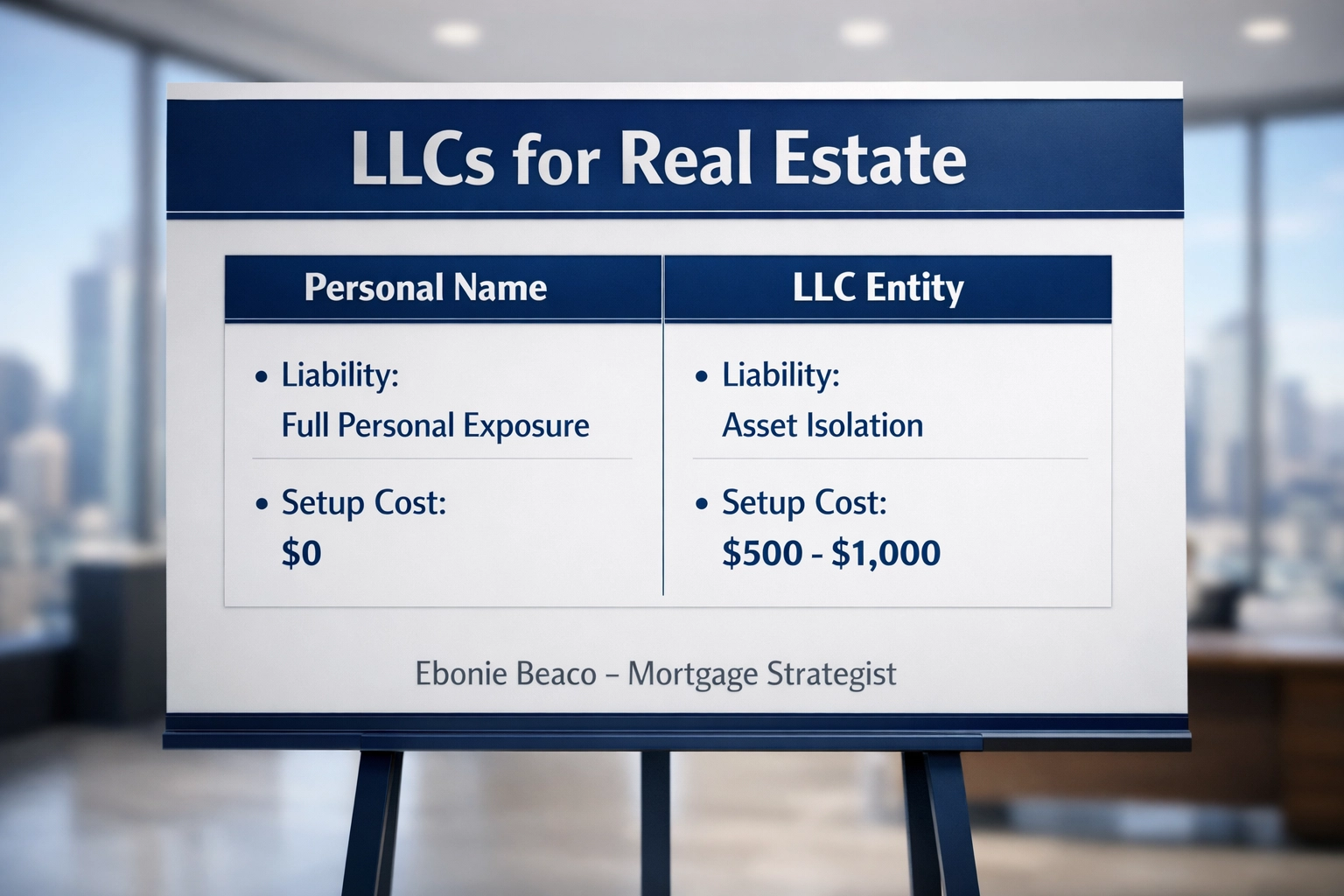

Image Description: A comparison table titled "LLCs for Real Estate". The table compares Personal Ownership vs. LLC Ownership. Personal Ownership: Setup Cost: $0, Liability Risk: High (Personal Assets Exposed), Financing: Easier (Conventional). LLC Ownership: Setup Cost: $500 - $1,000, Liability Risk: Low (Assets Isolated), Financing: Specialized (DSCR/Non-QM). At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Image Description: A comparison table titled "LLCs for Real Estate". The table compares Personal Ownership vs. LLC Ownership. Personal Ownership: Setup Cost: $0, Liability Risk: High (Personal Assets Exposed), Financing: Easier (Conventional). LLC Ownership: Setup Cost: $500 - $1,000, Liability Risk: Low (Assets Isolated), Financing: Specialized (DSCR/Non-QM). At the bottom: Ebonie Beaco - Mortgage Loan Officer.

The Financing Challenge: Why Your Entity Type Affects Your Loan

While an LLC is great for protection, it can complicate your mortgage options. Most "Conventional" loans, the ones backed by Fannie Mae and Freddie Mac, are designed for individuals, not business entities. If you want a standard 30 year fixed rate with the lowest possible interest rate, you usually have to close in your personal name.

However, many investors in states like Georgia, Alabama, or California prefer more flexible options. This is where DSCR Investor Loans and Non-QM Mortgage Loans become vital.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage product that qualifies the borrower based on the property’s rental income rather than personal income tax returns. Practical application: This allows you to close the loan in the name of your LLC, keeping the debt off your personal credit report while focusing on the property's performance.

If you are a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investor, using an LLC combined with a Cash-Out Refinance is a powerful way to scale. You buy a distressed property, fix it up, and then use a DSCR loan to pull your initial capital back out through the LLC. You can learn more about how these specific programs work on our mortgage basics page.

The Costs of Maintaining an LLC

Holding property in an LLC is not free. You need to consider the setup and ongoing compliance costs, which vary significantly by state.

- Filing Fees: Some states like Arkansas or Indiana have very low filing fees. Others, like California, require an annual franchise tax (currently $800) regardless of whether the LLC made money.

- Registered Agent Fees: If you don't want your home address on public record, you will pay a small annual fee for a registered agent.

- Separate Bookkeeping: You must keep your business and personal finances separate. Mixing funds (commingling) can "pierce the corporate veil," making the LLC's protection useless in court.

Access our FAQ for more details on common investor hurdles regarding entity costs and loan requirements.

Transferring Property: The "Due on Sale" Clause

A frequent question from current homeowners is: "Can I just transfer my existing rental property into an LLC?"

Technically, yes, you can use a quitclaim deed to transfer the title. However, most standard mortgages include a Due on Sale Clause.

Due on Sale Clause: A provision in a mortgage contract that requires the full loan balance to be paid if the property is transferred to a new owner. Practical application: If you transfer title from yourself to an LLC without lender permission, the lender could technically call the entire loan due immediately.

Investors often avoid this risk by either getting lender consent in writing or by using specialized Land Lord Loans that are designed to be held in an LLC from the start. If you are looking to move a property into an entity, you might consider a home refinance into a loan program that allows for business entity ownership.

LLCs for Short-Term Rentals (Airbnb)

If you are operating an Airbnb in vacation hubs like Florida or Virginia, an LLC is almost a requirement for many professional hosts. Short-term rentals involve a higher volume of "guests" on the property compared to long-term tenants. This increase in foot traffic naturally increases the risk of a liability claim.

Airbnb and Short-Term Rental Financing often utilizes the same DSCR models mentioned earlier. Lenders look at the projected "Short Term Rental" income to see if the property can cover its own debt. Buying these properties through an LLC provides that extra layer of comfort while you build your hospitality brand.

Making the Decision

So, should you buy in an LLC?

If you are just starting with one small property and want the lowest possible interest rate, buying in your personal name with a high-limit umbrella insurance policy might be enough for now.

However, if you plan to build a portfolio, have significant personal assets to protect, or are working with partners, an LLC is generally the preferred path. It provides a professional structure that is recognized by lenders offering Bridge Loans, Fix and Flip Loans, and Hard Money Loans.

Jump in and research your specific state requirements in places like Kentucky, Missouri, or Illinois. Every state has different rules regarding how LLCs are treated in court and how they are taxed.

How We Help Investors

Navigating the intersection of legal entities and mortgage lending is what we do. Whether you are a wholesaler looking to transition into holding rentals, or a seasoned landlord needing to extract equity from a portfolio of 10 properties, we provide the strategy to make it happen.

We understand the nuances of Non-QM Mortgage Loans and how to structure deals that traditional banks might turn away. Our team helps you compare options between closing personally or through your entity so you can make the choice that fits your long-term goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

For more information about our team and how we serve the investor community, visit our about us page or check out what our clients say on our testimonials page. If you are ready to see what you qualify for, you can start with our online forms to begin the scenario review.