Self-Employed? How to Get a Mortgage Without Tax Returns

For many entrepreneurs, freelancers, and small business owners, the tax season is a time to maximize deductions. You work hard to keep your net income low to reduce your tax liability, which is a smart move for your bottom line. However, this strategy often backfires when you walk into a traditional bank to buy a home or refinance a property.

Standard lenders look at the "bottom line" on your tax returns. If you earned $200,000 in gross revenue but wrote off $150,000 in equipment, travel, and home office expenses, the bank sees an income of only $50,000. For a high-balance mortgage in markets like Chicago, Los Angeles, or Miami, that $50,000 figure rarely cuts it.

The good news is that the mortgage industry has evolved. You can secure financing based on your actual cash flow rather than what you tell the IRS. This guide explores the mechanics of bank statement loans and other non-QM (Non-Qualified Mortgage) options that empower self-employed professionals to achieve their real estate goals.

The Disconnect Between Cash Flow and Taxable Income

Traditional mortgage underwriting is designed for W-2 employees. Lenders love the predictability of a paystub and a W-2 form. For the self-employed, income is rarely a straight line. It fluctuates based on seasonality, business reinvestment, and economic shifts.

When you apply for a conventional loan, the lender typically averages your net profit from the last two years of tax returns. If your business is growing rapidly, those two-year-old tax returns don't reflect your current financial strength. This creates a barrier for high-performing business owners who have the liquidity and assets to afford a home but lack the specific documentation traditional banks demand.

To understand the fundamentals of different loan types, you can explore mortgage basics to see how various programs compare.

Bank Statement Loans: The Solution for Entrepreneurs

A bank statement loan is a type of Non-QM mortgage that allows you to prove your income using your business or personal bank deposits rather than tax transcripts. This program focuses on your ability to repay the loan based on the actual money flowing into your accounts.

How Lenders Calculate Your Income

Instead of looking at your tax returns, a lender will typically request 12 to 24 months of complete bank statements. They look for consistent deposits that indicate a stable business.

Lenders apply an "expense factor" to your total deposits to estimate your qualifying income. This factor varies depending on the type of business you run. A service-based consultant with low overhead might have a 10% to 20% expense factor, while a restaurant owner or a contractor with high material costs might see a 50% expense factor.

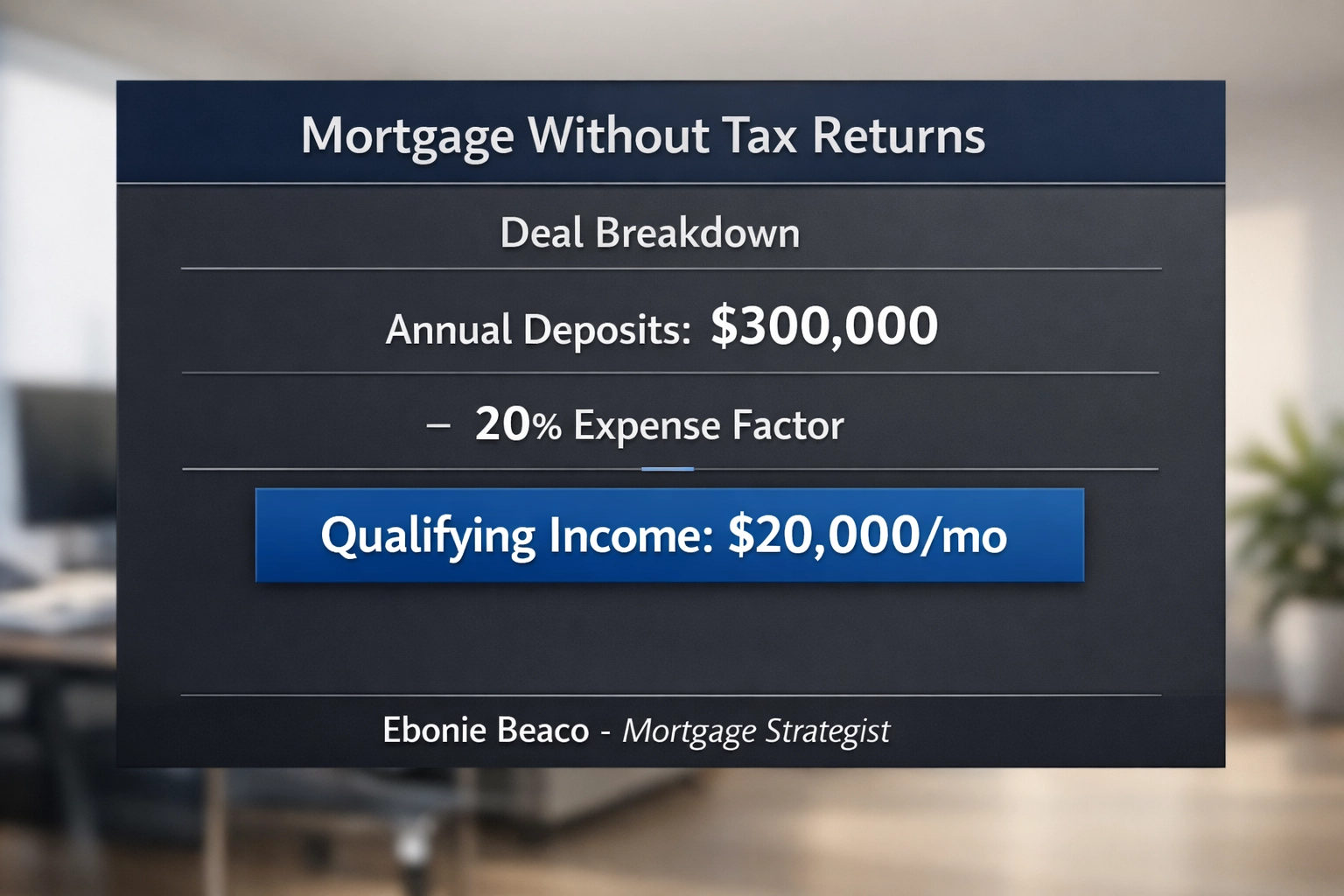

A Practical Example of the Bank Statement Calculation

Imagine a graphic design agency owner in Atlanta with the following financial profile:

- Total Annual Deposits: $300,000

- Business Type: Service-based (low overhead)

- Lender Expense Factor: 20%

- Net Qualifying Income: $240,000 ($20,000 per month)

Under traditional tax return underwriting, if that same owner wrote off $220,000 in expenses, their qualifying income would only be $80,000 ($6,666 per month). The bank statement program effectively triples their buying power.

Title: Bank Statement Income Calculation Example. Business Deposits: $300,000 / 12 months = $25,000/mo. Less 20% Expense Factor ($5,000) = $20,000 Qualifying Monthly Income. Ebonie Beaco - Mortgage Loan Officer.

Title: Bank Statement Income Calculation Example. Business Deposits: $300,000 / 12 months = $25,000/mo. Less 20% Expense Factor ($5,000) = $20,000 Qualifying Monthly Income. Ebonie Beaco - Mortgage Loan Officer.

Key Requirements for Bank Statement Mortgages

While these loans offer flexibility regarding documentation, they are not "no-doc" loans. Lenders still require proof of stability and financial responsibility.

Credit Score Standards

Expect to need a credit score between 660 and 760 to access the most competitive rates. Some programs allow for lower scores, but they often require a larger down payment to offset the risk.

Down Payment Requirements

Since bank statement loans carry more perceived risk than government-backed loans, the down payment is typically higher. You should prepare to put down between 10% and 40%, depending on your credit profile and the property type.

Business Tenure

Most programs require you to have been self-employed in the same industry for at least two years. Lenders verify this through business licenses, a letter from a CPA, or Secretary of State filings.

Debt-to-Income (DTI) Ratio

Lenders generally look for a DTI ratio of 45% or lower. This means your total monthly debt payments, including your new mortgage, should not exceed 45% of the qualifying income calculated from your bank statements. You can use mortgage calculators to estimate your potential payments.

Exploring Alternative Non-QM Options

If bank statement loans aren't the right fit, other strategies exist for self-employed borrowers and real estate investors.

P&L Mortgages

For business owners whose bank statements are complicated by high transaction volumes or co-mingled funds, a Profit and Loss (P&L) mortgage is an alternative. In this scenario, a CPA or a licensed tax preparer provides a P&L statement covering the last 12 to 24 months. The lender uses the net income on this statement to qualify you.

1099 Income Loans

If you are a contract worker or a gig economy professional, such as an IT consultant in Virginia or a traveling nurse in Florida, you might qualify for a 1099 loan. This program uses the gross income reported on your 1099 forms without requiring full tax returns. It is an excellent middle ground for those who have a few primary clients rather than a traditional business structure.

DSCR Loans for Investors

If you are looking to purchase an investment property rather than a primary residence, the Debt Service Coverage Ratio (DSCR) loan is often the path of least resistance. These loans don't look at your personal income or tax returns at all. Instead, they qualify the property based on its ability to generate enough rental income to cover the mortgage payment. This is a favorite strategy for landlords in markets like Chicago and throughout California.

For more information on the steps involved, check out the loan process page.

Real Estate Markets and Financing Trends

Financing strategies often vary by region. In high-cost areas like California or Northern Virginia, self-employed borrowers frequently use bank statement loans to bridge the gap between their tax-reported income and the price of local real estate.

In Florida, we see a high volume of foreign national investors and retirees using non-traditional financing to secure vacation rentals. Meanwhile, in the Midwest: specifically in states like Michigan, Indiana, and Illinois: investors often utilize home refinance options or cash-out strategies to fund their next acquisition.

Whether you are looking for a primary home purchase or building a portfolio, understanding these non-QM tools is essential for modern real estate success.

Preparation Checklist for Your Application

Before you reach out to a mortgage strategist, organize your financial footprint to ensure a smooth process.

- Separate Your Accounts: If you haven't already, separate your business and personal finances. It makes the income calculation much cleaner for underwriters.

- Audit Your Deposits: Ensure all large deposits are documented. Lenders look for "seasoned" funds and regular business activity.

- Clean Up Credit: Pay down revolving credit card balances to improve your DTI and boost your credit score before the initial pull.

- Verify Business Existence: Ensure your business licenses are up to date and your status with the Secretary of State is "Active."

Navigating the Path to Approval

Securing a mortgage without tax returns requires a specialized approach. You need a strategist who understands the nuances of business accounting and how to present your scenario to the right underwriter.

Transparency is a core value at Home Loans Network. We believe every borrower deserves a clear path to homeownership, regardless of how they earn their living. If you have been told "no" by a big-box bank because of your tax returns, it simply means you were talking to the wrong lender for your specific profile.

Explore our about us page to learn more about our commitment to finding creative solutions for unique financial situations.

Jump in and discover how your business success can translate into real estate equity. Compare your options, ask the hard questions, and access the capital you need to move forward.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664