Scaling to 10+ Properties: Financing Strategies for Savvy Investors

Scaling a real estate portfolio from a few units to a double-digit collection of properties requires a fundamental shift in how you view debt. Most investors start with conventional financing, hitting a wall once they reach the magic number of ten financed properties. To push past this limit in markets like Chicago, Atlanta, or Tampa, you need a sophisticated toolkit of financing vehicles that prioritize asset performance over personal income.

The Transition from Individual to Portfolio Investor

When you own one or two rentals, lenders look at you as an individual with some extra income. Once you target 10 or more properties, you transition into a business entity in the eyes of the lending world. This shift allows you to move away from the strict debt-to-income (DTI) requirements that often stall growth for high-earning professionals.

Explore the world of non-QM (Non-Qualified Mortgage) products. These loans do not follow the standard federal guidelines, offering more flexibility for investors who have complex tax returns or multiple active projects. Accessing these tools is essential for staying liquid while expanding your footprint across states like Michigan, Virginia, and Florida.

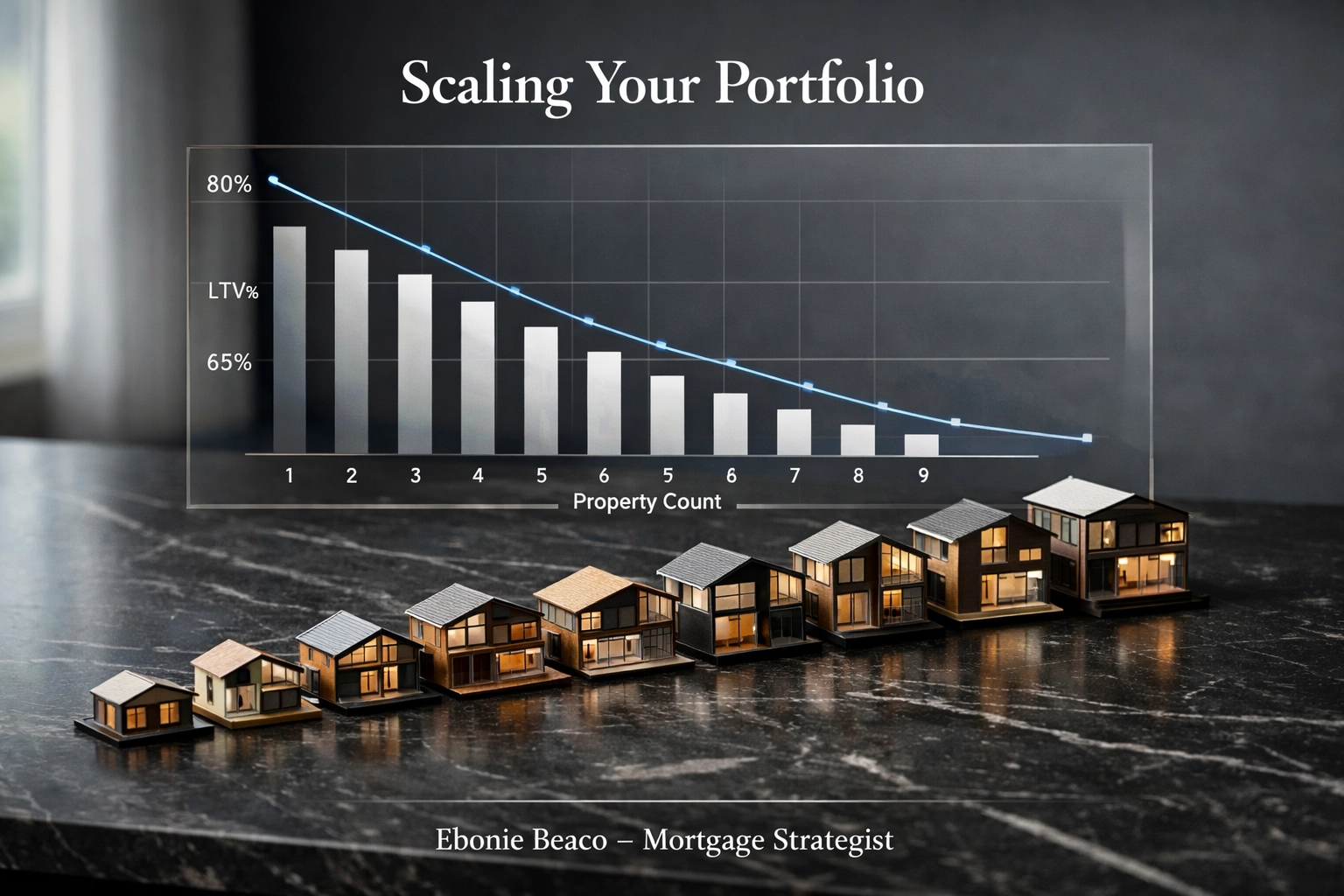

Scaling Your Portfolio - Portfolio Growth and LTV Across 10 Properties

Ebonie Beaco - Mortgage Loan Officer

Scaling Your Portfolio - Portfolio Growth and LTV Across 10 Properties

Ebonie Beaco - Mortgage Loan Officer

Leveraging DSCR Loans for Unlimited Growth

DSCR (Debt Service Coverage Ratio) Loans: A mortgage product where qualification is based on the cash flow of the property rather than the personal income of the borrower. Practical Application: This allows you to acquire property number 11, 12, or 50 without your personal salary being the deciding factor in the approval.

In high-growth regions like Georgia and Arkansas, DSCR loans have become the go-to for savvy investors. Because these loans focus on whether the rent covers the mortgage, taxes, and insurance (PITIA), you can scale as long as the deals make sense. You can compare different DSCR options at the Home Loans Network FAQ page to see how they fit your current acquisitions.

The calculation for DSCR is straightforward: Gross Rental Income / Monthly Debt Service = DSCR Ratio For example, if a duplex in Indianapolis generates $3,000 in rent and the mortgage payment is $2,400, your DSCR is 1.25. Most lenders look for a ratio of 1.20 or higher to offer the most competitive rates.

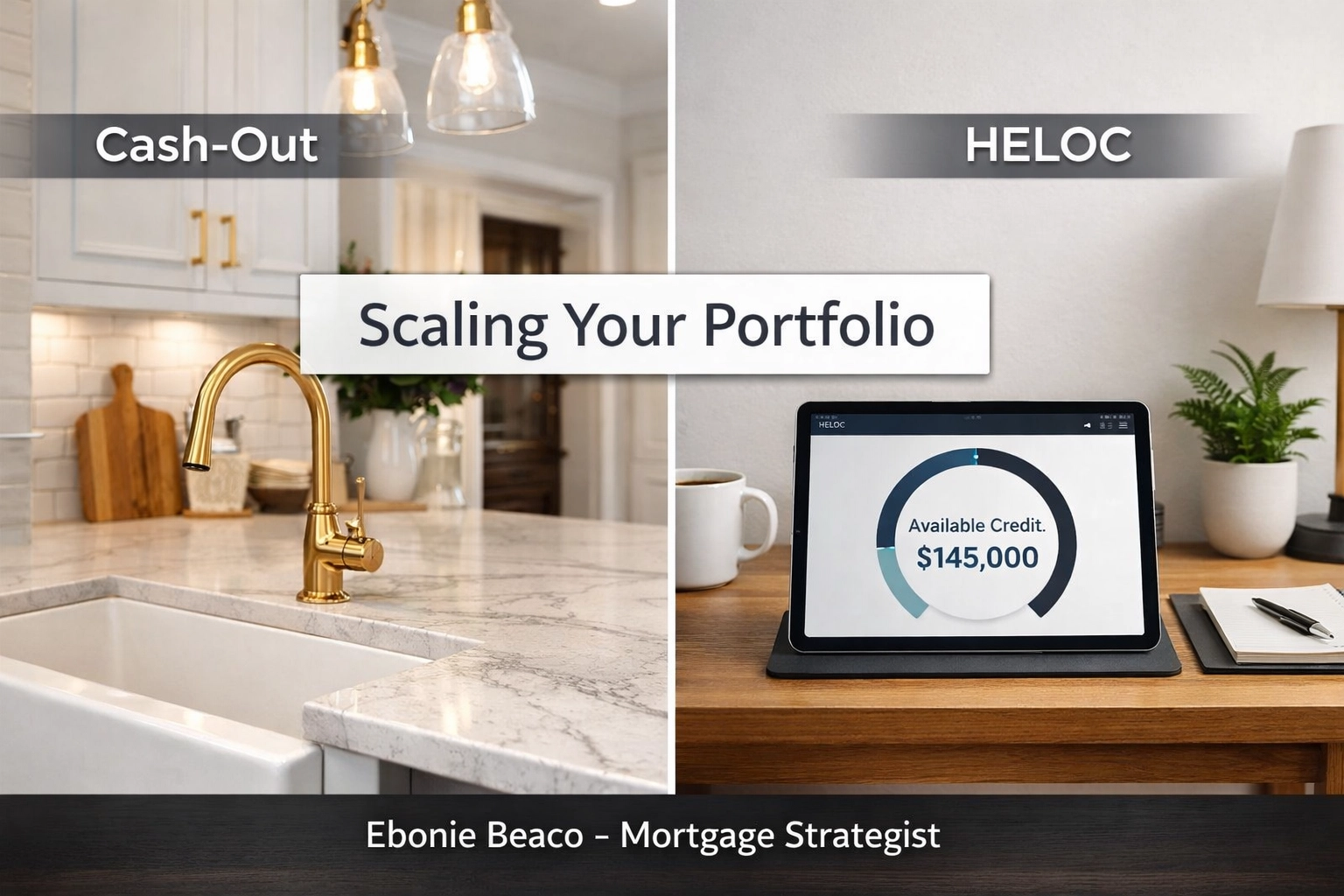

The Power of Cash-Out Refinancing

Cash-Out Refinance: A refinancing option where the new mortgage is for a larger amount than the existing loan, and the borrower receives the difference in cash. Practical Application: Use the "forced equity" from a renovation in California or Virginia to fund the down payment on your next two properties.

For investors following the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method, the cash-out refinance is the engine of the entire operation. By extracting equity from a stabilized asset, you recycle your initial capital into new opportunities. This keeps your "cash on cash" return high and your personal savings accounts intact. Check out the mortgage calculators to model how much equity you can safely pull while maintaining a healthy cash flow.

Utilizing HELOCs on Investment Properties

HELOC (Home Equity Line of Credit): A revolving line of credit secured by the equity in a property, allowing you to borrow, repay, and borrow again. Practical Application: Establish a line of credit on a free-and-clear rental in Missouri to use as a "ready-to-go" fund for earnest money or quick renovations.

Many investors realize that keeping equity "trapped" in a property is a missed opportunity. A HELOC on an investment property provides a safety net and a rapid-response fund for distressed deals in competitive markets like Northern Virginia or Southern California. Unlike a standard loan, you only pay interest on what you use, making it a highly efficient scaling tool.

Scaling Your Portfolio - Comparison of HELOC vs. Cash-Out Refinance for Investors

Ebonie Beaco - Mortgage Loan Officer

Scaling Your Portfolio - Comparison of HELOC vs. Cash-Out Refinance for Investors

Ebonie Beaco - Mortgage Loan Officer

Financing Beyond the 10-Property Limit

Once you surpass ten properties, conventional banks often become less helpful. This is where business entity lending and portfolio loans take center stage.

Portfolio Loan: A mortgage that a lender keeps on their own books instead of selling it on the secondary market. Practical Application: Grouping five separate single-family homes in Alabama into one single commercial loan to simplify management and potentially lower aggregate interest costs.

Scaling to 10+ properties often involves moving your holdings into an LLC or S-Corp. This adds a layer of asset protection and allows for business-purpose loans that don't appear on your personal credit report. This strategy is vital for maintaining a strong credit score while managing millions of dollars in real estate debt. You can learn more about the transition to these products at the Home Loans Network about us page.

Advanced Capital Strategies: Life Insurance and SBLOCs

Experienced investors often look beyond real estate for financing. SBLOC (Securities-Backed Line of Credit): A line of credit that uses your stock or bond portfolio as collateral. Practical Application: Borrow against your brokerage account to buy a fix-and-flip in Chicago for "cash," then refinance into a long-term loan once the work is done.

Similarly, cash-value life insurance (like IUL or Whole Life) can act as your own private bank. By borrowing against the cash value of a policy, you can fund real estate deals without the typical bank approval process. The policy continues to grow as if the money were still there, creating a "double compounding" effect that accelerates wealth building.

Managing Loan-to-Value (LTV) Across a Portfolio

LTV (Loan-to-Value): The ratio of a loan to the value of the asset purchased. Practical Application: Keeping a total portfolio LTV of 70% or lower ensures that a market dip in Florida or Kentucky won't put your entire operation at risk.

As you scale, the total LTV of your portfolio is more important than the LTV of a single property. Professional investors often "cross-collateralize," using the high equity in older properties to secure financing for newer ones with lower down payments. This holistic view of your balance sheet is what separates a landlord from a real estate mogul.

Scaling Your Portfolio - Visual Breakdown of Cross-Collateralization Strategy

Ebonie Beaco - Mortgage Loan Officer

Scaling Your Portfolio - Visual Breakdown of Cross-Collateralization Strategy

Ebonie Beaco - Mortgage Loan Officer

Regional Strategy: Where You Scale

Your financing strategy should reflect the market you are in.

- In Illinois (Chicago): Focus on multi-unit financing (2-4 units) to maximize the "per-loan" property count.

- In Florida and Georgia: DSCR loans are highly effective for short-term rental (Airbnb) properties where rental income often far exceeds standard long-term rates.

- In Indiana and Michigan: Lower entry points allow for rapid acquisition using bridge loans before refinancing into long-term debt.

Navigating the local nuances of each state requires a partner who understands the specific lending environment. Whether you are looking at the loan process for your first out-of-state investment or your twentieth, having a clear roadmap is essential.

Summary of Scaling Tactics

- Pivot to DSCR: Stop relying on your W2 income to qualify for rentals.

- Unlock Equity: Use HELOCs and Cash-Out Refinances to keep your capital moving.

- Think in Portfolios: Group properties together to gain better terms and simplify your life.

- Protect the Entity: Move properties into LLCs to access business-purpose lending.

- Monitor Your Ratios: Keep your DSCR above 1.2 and your portfolio LTV in a safe range.

Scaling to 10+ properties is not just about finding more houses; it is about building a sustainable financing machine. When you stop being the "borrower" and start being the "sponsor" of your deals, the limit on your growth effectively disappears.

If you are ready to stop hitting walls and start building a real estate empire, it is time to look at your financing through a strategic lens. Jump in and see what options are available for your specific scenario by visiting our home purchase page.

Ready to scale to 10+ properties? Contact Ebonie Beaco for advanced financing strategies and mentoring.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664